BIOSKRYB GENOMICS PORTER'S FIVE FORCES TEMPLATE RESEARCH

What is included in the product

Detailed analysis of each competitive force, supported by industry data and strategic commentary.

Instantly spot opportunities or risks with data-driven visualizations.

What You See Is What You Get

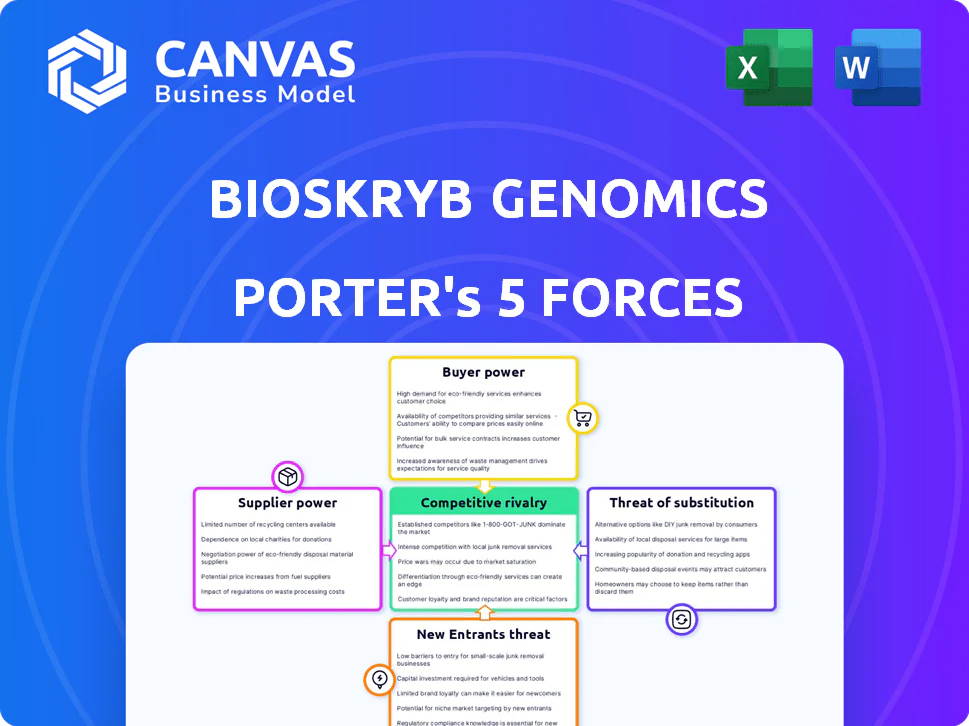

BioSkryb Genomics Porter's Five Forces Analysis

This preview presents the full BioSkryb Genomics Porter's Five Forces Analysis. What you see now is the same comprehensive document you'll receive instantly upon purchase.

Porter's Five Forces Analysis Template

Go Beyond the Preview—Access the Full Strategic Report

BioSkryb Genomics faces moderate rivalry due to competition in genomics. Buyer power is moderate, influenced by customer needs. Supplier power is moderate due to specialized reagents.

The threat of new entrants is moderate, based on high barriers. Substitute threats are low. These forces shape BioSkryb's market position.

Unlock key insights into BioSkryb Genomics’s industry forces—from buyer power to substitute threats—and use this knowledge to inform strategy or investment decisions.

Suppliers Bargaining Power

Limited Number of Specialized Suppliers

The genomics market, especially single-cell analysis, relies on a few key suppliers. These suppliers provide vital reagents and equipment, creating a concentrated supply chain. This concentration gives suppliers significant pricing power. For instance, in 2024, the top 3 reagent suppliers controlled over 60% of the market.

High Switching Costs

BioSkryb's PTA tech ties them to specific suppliers. Changing suppliers means hefty costs for validation, retraining, and workflow adjustments. This dependency boosts supplier power. In 2024, such tech-specific integrations often increase switching costs by 15-25%.

Supplier Differentiation

Suppliers in genomics differentiate through product quality and innovation. Those offering advanced reagents and technologies gain stronger bargaining power. BioSkryb depends on specialized components for its solutions. In 2024, the single-cell analysis market was valued at over $3 billion, highlighting the value of key suppliers.

Potential for Forward Integration

Forward integration by suppliers is less typical but possible in the life sciences sector. Large suppliers might develop their own single-cell analysis tech, directly competing with BioSkryb. This move would significantly increase their leverage over BioSkryb, impacting its market position. The risk is heightened by the increasing consolidation among life science suppliers.

- Recent mergers and acquisitions in the life sciences supply market show a trend toward supplier consolidation, with deals like Thermo Fisher Scientific's acquisition of PPD in 2021.

- The single-cell analysis market is growing, with projections estimating it to reach $7.2 billion by 2028.

- A supplier entering the market could quickly gain traction, given their existing customer base and distribution networks.

- BioSkryb's reliance on specific reagents and consumables makes it vulnerable to such moves.

Strong Relationships with Research Institutions

Suppliers with robust ties to research institutions, like universities, hold a strategic advantage, especially with key customers such as BioSkryb. These connections can significantly affect product adoption, potentially creating a dependency that strengthens the supplier's position. Strong relationships can lead to preference in purchasing and influence the direction of research funding. This influence translates into increased bargaining power for the suppliers.

- Academic research spending in the U.S. reached $97.5 billion in 2023.

- Over 60% of scientific instruments are purchased by universities and research institutions.

- BioSkryb's primary customers include academic and research institutions.

BioSkryb's Supplier Dynamics: Pricing Power & Costs

The genomics market's reliance on key suppliers grants them substantial pricing power. BioSkryb's technology ties it to specific suppliers, raising switching costs, which in 2024 increased by 15-25%. Suppliers leverage product quality and innovation, especially those with strong ties to research institutions, influencing product adoption. Academic research spending in the U.S. reached $97.5 billion in 2023.

| Factor | Impact on BioSkryb | 2024 Data |

|---|---|---|

| Supplier Concentration | High bargaining power | Top 3 reagent suppliers controlled over 60% of the market. |

| Switching Costs | Increased dependency | Tech-specific integrations often increase switching costs by 15-25%. |

| Innovation & Relationships | Strategic advantage for suppliers | Single-cell analysis market valued at over $3 billion. |

Customers Bargaining Power

Diverse Customer Base

BioSkryb's diverse customer base, encompassing academic researchers, healthcare providers, and pharmaceutical companies, is a key strength. This broad reach helps to mitigate the risk of over-reliance on any single customer. In 2024, companies with diversified customer bases often report more stable revenue streams, as seen in the biotech sector. This diversification reduces the impact of any single customer's bargaining power.

Increasing Access to Information

Customers in the genomics market are increasingly informed, thanks to online resources and industry events. This transparency lets them easily compare technologies and prices. For example, in 2024, the global genomics market was valued at $24.8 billion, with customers having diverse choices. This empowers them to negotiate better terms, increasing their bargaining power.

Demand for Personalized Solutions and Data Integration

Customers increasingly demand personalized solutions and seamless data integration, particularly in genomics. BioSkryb must offer comprehensive, integrated workflows to meet these needs. This demand for customization empowers sophisticated customers, giving them leverage. The global genomics market, valued at $23.8 billion in 2023, underscores the importance of customer-centric strategies.

Price Sensitivity

Price sensitivity significantly impacts BioSkryb Genomics' customer bargaining power. The high cost of single-cell analysis tools and consumables, with some instruments costing over $200,000, makes customers price-conscious. This is especially true for academic institutions and smaller biotech firms. The availability of alternative, potentially cheaper, solutions strengthens customer leverage in negotiations.

- Instrument costs can exceed $200,000.

- Academic labs and small biotechs are particularly price-sensitive.

- Alternative solutions increase customer bargaining power.

Availability of In-House Capabilities

Some major players in the biotech and pharmaceutical sectors possess the resources to establish their own single-cell analysis departments. This internal capability diminishes their need for external services, like those offered by BioSkryb. Consequently, these entities gain leverage in price negotiations and service terms when they opt to outsource any part of their research. The trend of in-house lab development is growing; for example, in 2024, the National Institutes of Health invested $1.5 billion in advanced research facilities.

- Investment in internal capabilities reduces reliance on external providers.

- This increases bargaining power during outsourcing negotiations.

- Research institutions and pharma companies drive this trend.

- The NIH's 2024 investment highlights the growth.

Genomics Market Dynamics: Customer Power

BioSkryb's diverse customer base includes academic researchers, healthcare providers, and pharmaceutical companies, which helps spread risk. Informed customers in the genomics market, valued at $24.8B in 2024, can compare prices and negotiate. High costs, like instruments over $200,000, make customers price-sensitive, especially academic institutions.

| Factor | Impact | Data |

|---|---|---|

| Customer Knowledge | Increased Bargaining Power | Market size: $24.8B (2024) |

| Price Sensitivity | Higher Bargaining Power | Instruments >$200K |

| In-house Capabilities | Reduced Reliance | NIH invested $1.5B (2024) |

Rivalry Among Competitors

Presence of Established Players

The single-cell analysis market is fiercely competitive. Established players like 10x Genomics, Illumina, and Thermo Fisher Scientific dominate. These companies possess substantial resources and strong brand recognition. For instance, 10x Genomics reported $562 million in revenue for 2023. Intense rivalry is a key market characteristic.

Technological Advancements

Technological advancements are a major driver of competition in the genomics market. Companies constantly innovate, aiming for higher throughput and better accuracy. For example, in 2024, the NGS market reached $10.6 billion, reflecting intense competition among technology providers. This rapid pace of innovation forces companies to differentiate their offerings.

Focus on Multiomics

Competitive rivalry in multiomics is intensifying. The trend toward integrated multiomic analysis, combining various data types from single cells, is accelerating. Companies, including BioSkryb Genomics, compete by offering comprehensive workflows and analytical tools. The global genomics market, valued at $24.4 billion in 2023, is projected to reach $60.8 billion by 2030. This highlights the need for innovation.

Strategic Partnerships and Collaborations

Strategic partnerships and collaborations are prevalent in the genomics market, with companies teaming up to broaden their market presence. These alliances enable the integration of technologies and the creation of comprehensive solutions, intensifying rivalry. For example, in 2024, Illumina and Roche formed a partnership to improve cancer diagnostics. These collaborations provide customers with more integrated and accessible options, boosting competition.

- Illumina and Roche partnership in 2024 for cancer diagnostics.

- Partnerships can increase market reach and offer integrated solutions.

- These alliances boost competitive intensity.

- Collaboration examples include technology integration.

Market Growth Rate

The single-cell sequencing market's rapid growth fuels intense competition. This expansion draws in new entrants and substantial investments, intensifying the rivalry. The market, valued at $2.9 billion in 2024, is projected to reach $8.5 billion by 2029. The increased investment leads to a more dynamic and competitive setting.

- Market size in 2024: $2.9 billion.

- Projected market size by 2029: $8.5 billion.

- Annual growth rate: Approximately 24% (2024-2029).

- Key drivers: Technological advancements and increasing research demand.

Single-Cell Analysis: Fierce Competition & $2.9B Market

Competitive rivalry in the single-cell analysis market is very high. Established firms like 10x Genomics and Illumina compete fiercely. Technological advancements and strategic alliances further intensify competition. The single-cell sequencing market was $2.9 billion in 2024.

| Aspect | Details | Data |

|---|---|---|

| Key Players | Major Competitors | 10x Genomics, Illumina |

| Market Growth | Single-Cell Market (2024) | $2.9 Billion |

| Growth Rate | Projected (2024-2029) | ~24% Annually |

Original: $10.00

-65%$10.00

$3.50BIOSKRYB GENOMICS PORTER'S FIVE FORCES TEMPLATE RESEARCH

What is included in the product

Detailed analysis of each competitive force, supported by industry data and strategic commentary.

Instantly spot opportunities or risks with data-driven visualizations.

What You See Is What You Get

BioSkryb Genomics Porter's Five Forces Analysis

This preview presents the full BioSkryb Genomics Porter's Five Forces Analysis. What you see now is the same comprehensive document you'll receive instantly upon purchase.

Porter's Five Forces Analysis Template

Go Beyond the Preview—Access the Full Strategic Report

BioSkryb Genomics faces moderate rivalry due to competition in genomics. Buyer power is moderate, influenced by customer needs. Supplier power is moderate due to specialized reagents.

The threat of new entrants is moderate, based on high barriers. Substitute threats are low. These forces shape BioSkryb's market position.

Unlock key insights into BioSkryb Genomics’s industry forces—from buyer power to substitute threats—and use this knowledge to inform strategy or investment decisions.

Suppliers Bargaining Power

Limited Number of Specialized Suppliers

The genomics market, especially single-cell analysis, relies on a few key suppliers. These suppliers provide vital reagents and equipment, creating a concentrated supply chain. This concentration gives suppliers significant pricing power. For instance, in 2024, the top 3 reagent suppliers controlled over 60% of the market.

High Switching Costs

BioSkryb's PTA tech ties them to specific suppliers. Changing suppliers means hefty costs for validation, retraining, and workflow adjustments. This dependency boosts supplier power. In 2024, such tech-specific integrations often increase switching costs by 15-25%.

Supplier Differentiation

Suppliers in genomics differentiate through product quality and innovation. Those offering advanced reagents and technologies gain stronger bargaining power. BioSkryb depends on specialized components for its solutions. In 2024, the single-cell analysis market was valued at over $3 billion, highlighting the value of key suppliers.

Potential for Forward Integration

Forward integration by suppliers is less typical but possible in the life sciences sector. Large suppliers might develop their own single-cell analysis tech, directly competing with BioSkryb. This move would significantly increase their leverage over BioSkryb, impacting its market position. The risk is heightened by the increasing consolidation among life science suppliers.

- Recent mergers and acquisitions in the life sciences supply market show a trend toward supplier consolidation, with deals like Thermo Fisher Scientific's acquisition of PPD in 2021.

- The single-cell analysis market is growing, with projections estimating it to reach $7.2 billion by 2028.

- A supplier entering the market could quickly gain traction, given their existing customer base and distribution networks.

- BioSkryb's reliance on specific reagents and consumables makes it vulnerable to such moves.

Strong Relationships with Research Institutions

Suppliers with robust ties to research institutions, like universities, hold a strategic advantage, especially with key customers such as BioSkryb. These connections can significantly affect product adoption, potentially creating a dependency that strengthens the supplier's position. Strong relationships can lead to preference in purchasing and influence the direction of research funding. This influence translates into increased bargaining power for the suppliers.

- Academic research spending in the U.S. reached $97.5 billion in 2023.

- Over 60% of scientific instruments are purchased by universities and research institutions.

- BioSkryb's primary customers include academic and research institutions.

BioSkryb's Supplier Dynamics: Pricing Power & Costs

The genomics market's reliance on key suppliers grants them substantial pricing power. BioSkryb's technology ties it to specific suppliers, raising switching costs, which in 2024 increased by 15-25%. Suppliers leverage product quality and innovation, especially those with strong ties to research institutions, influencing product adoption. Academic research spending in the U.S. reached $97.5 billion in 2023.

| Factor | Impact on BioSkryb | 2024 Data |

|---|---|---|

| Supplier Concentration | High bargaining power | Top 3 reagent suppliers controlled over 60% of the market. |

| Switching Costs | Increased dependency | Tech-specific integrations often increase switching costs by 15-25%. |

| Innovation & Relationships | Strategic advantage for suppliers | Single-cell analysis market valued at over $3 billion. |

Customers Bargaining Power

Diverse Customer Base

BioSkryb's diverse customer base, encompassing academic researchers, healthcare providers, and pharmaceutical companies, is a key strength. This broad reach helps to mitigate the risk of over-reliance on any single customer. In 2024, companies with diversified customer bases often report more stable revenue streams, as seen in the biotech sector. This diversification reduces the impact of any single customer's bargaining power.

Increasing Access to Information

Customers in the genomics market are increasingly informed, thanks to online resources and industry events. This transparency lets them easily compare technologies and prices. For example, in 2024, the global genomics market was valued at $24.8 billion, with customers having diverse choices. This empowers them to negotiate better terms, increasing their bargaining power.

Demand for Personalized Solutions and Data Integration

Customers increasingly demand personalized solutions and seamless data integration, particularly in genomics. BioSkryb must offer comprehensive, integrated workflows to meet these needs. This demand for customization empowers sophisticated customers, giving them leverage. The global genomics market, valued at $23.8 billion in 2023, underscores the importance of customer-centric strategies.

Price Sensitivity

Price sensitivity significantly impacts BioSkryb Genomics' customer bargaining power. The high cost of single-cell analysis tools and consumables, with some instruments costing over $200,000, makes customers price-conscious. This is especially true for academic institutions and smaller biotech firms. The availability of alternative, potentially cheaper, solutions strengthens customer leverage in negotiations.

- Instrument costs can exceed $200,000.

- Academic labs and small biotechs are particularly price-sensitive.

- Alternative solutions increase customer bargaining power.

Availability of In-House Capabilities

Some major players in the biotech and pharmaceutical sectors possess the resources to establish their own single-cell analysis departments. This internal capability diminishes their need for external services, like those offered by BioSkryb. Consequently, these entities gain leverage in price negotiations and service terms when they opt to outsource any part of their research. The trend of in-house lab development is growing; for example, in 2024, the National Institutes of Health invested $1.5 billion in advanced research facilities.

- Investment in internal capabilities reduces reliance on external providers.

- This increases bargaining power during outsourcing negotiations.

- Research institutions and pharma companies drive this trend.

- The NIH's 2024 investment highlights the growth.

Genomics Market Dynamics: Customer Power

BioSkryb's diverse customer base includes academic researchers, healthcare providers, and pharmaceutical companies, which helps spread risk. Informed customers in the genomics market, valued at $24.8B in 2024, can compare prices and negotiate. High costs, like instruments over $200,000, make customers price-sensitive, especially academic institutions.

| Factor | Impact | Data |

|---|---|---|

| Customer Knowledge | Increased Bargaining Power | Market size: $24.8B (2024) |

| Price Sensitivity | Higher Bargaining Power | Instruments >$200K |

| In-house Capabilities | Reduced Reliance | NIH invested $1.5B (2024) |

Rivalry Among Competitors

Presence of Established Players

The single-cell analysis market is fiercely competitive. Established players like 10x Genomics, Illumina, and Thermo Fisher Scientific dominate. These companies possess substantial resources and strong brand recognition. For instance, 10x Genomics reported $562 million in revenue for 2023. Intense rivalry is a key market characteristic.

Technological Advancements

Technological advancements are a major driver of competition in the genomics market. Companies constantly innovate, aiming for higher throughput and better accuracy. For example, in 2024, the NGS market reached $10.6 billion, reflecting intense competition among technology providers. This rapid pace of innovation forces companies to differentiate their offerings.

Focus on Multiomics

Competitive rivalry in multiomics is intensifying. The trend toward integrated multiomic analysis, combining various data types from single cells, is accelerating. Companies, including BioSkryb Genomics, compete by offering comprehensive workflows and analytical tools. The global genomics market, valued at $24.4 billion in 2023, is projected to reach $60.8 billion by 2030. This highlights the need for innovation.

Strategic Partnerships and Collaborations

Strategic partnerships and collaborations are prevalent in the genomics market, with companies teaming up to broaden their market presence. These alliances enable the integration of technologies and the creation of comprehensive solutions, intensifying rivalry. For example, in 2024, Illumina and Roche formed a partnership to improve cancer diagnostics. These collaborations provide customers with more integrated and accessible options, boosting competition.

- Illumina and Roche partnership in 2024 for cancer diagnostics.

- Partnerships can increase market reach and offer integrated solutions.

- These alliances boost competitive intensity.

- Collaboration examples include technology integration.

Market Growth Rate

The single-cell sequencing market's rapid growth fuels intense competition. This expansion draws in new entrants and substantial investments, intensifying the rivalry. The market, valued at $2.9 billion in 2024, is projected to reach $8.5 billion by 2029. The increased investment leads to a more dynamic and competitive setting.

- Market size in 2024: $2.9 billion.

- Projected market size by 2029: $8.5 billion.

- Annual growth rate: Approximately 24% (2024-2029).

- Key drivers: Technological advancements and increasing research demand.

Single-Cell Analysis: Fierce Competition & $2.9B Market

Competitive rivalry in the single-cell analysis market is very high. Established firms like 10x Genomics and Illumina compete fiercely. Technological advancements and strategic alliances further intensify competition. The single-cell sequencing market was $2.9 billion in 2024.

| Aspect | Details | Data |

|---|---|---|

| Key Players | Major Competitors | 10x Genomics, Illumina |

| Market Growth | Single-Cell Market (2024) | $2.9 Billion |

| Growth Rate | Projected (2024-2029) | ~24% Annually |

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

What is included in the product

Detailed analysis of each competitive force, supported by industry data and strategic commentary.

Instantly spot opportunities or risks with data-driven visualizations.

What You See Is What You Get

BioSkryb Genomics Porter's Five Forces Analysis

This preview presents the full BioSkryb Genomics Porter's Five Forces Analysis. What you see now is the same comprehensive document you'll receive instantly upon purchase.

Porter's Five Forces Analysis Template

Go Beyond the Preview—Access the Full Strategic Report

BioSkryb Genomics faces moderate rivalry due to competition in genomics. Buyer power is moderate, influenced by customer needs. Supplier power is moderate due to specialized reagents.

The threat of new entrants is moderate, based on high barriers. Substitute threats are low. These forces shape BioSkryb's market position.

Unlock key insights into BioSkryb Genomics’s industry forces—from buyer power to substitute threats—and use this knowledge to inform strategy or investment decisions.

Suppliers Bargaining Power

Limited Number of Specialized Suppliers

The genomics market, especially single-cell analysis, relies on a few key suppliers. These suppliers provide vital reagents and equipment, creating a concentrated supply chain. This concentration gives suppliers significant pricing power. For instance, in 2024, the top 3 reagent suppliers controlled over 60% of the market.

High Switching Costs

BioSkryb's PTA tech ties them to specific suppliers. Changing suppliers means hefty costs for validation, retraining, and workflow adjustments. This dependency boosts supplier power. In 2024, such tech-specific integrations often increase switching costs by 15-25%.

Supplier Differentiation

Suppliers in genomics differentiate through product quality and innovation. Those offering advanced reagents and technologies gain stronger bargaining power. BioSkryb depends on specialized components for its solutions. In 2024, the single-cell analysis market was valued at over $3 billion, highlighting the value of key suppliers.

Potential for Forward Integration

Forward integration by suppliers is less typical but possible in the life sciences sector. Large suppliers might develop their own single-cell analysis tech, directly competing with BioSkryb. This move would significantly increase their leverage over BioSkryb, impacting its market position. The risk is heightened by the increasing consolidation among life science suppliers.

- Recent mergers and acquisitions in the life sciences supply market show a trend toward supplier consolidation, with deals like Thermo Fisher Scientific's acquisition of PPD in 2021.

- The single-cell analysis market is growing, with projections estimating it to reach $7.2 billion by 2028.

- A supplier entering the market could quickly gain traction, given their existing customer base and distribution networks.

- BioSkryb's reliance on specific reagents and consumables makes it vulnerable to such moves.

Strong Relationships with Research Institutions

Suppliers with robust ties to research institutions, like universities, hold a strategic advantage, especially with key customers such as BioSkryb. These connections can significantly affect product adoption, potentially creating a dependency that strengthens the supplier's position. Strong relationships can lead to preference in purchasing and influence the direction of research funding. This influence translates into increased bargaining power for the suppliers.

- Academic research spending in the U.S. reached $97.5 billion in 2023.

- Over 60% of scientific instruments are purchased by universities and research institutions.

- BioSkryb's primary customers include academic and research institutions.

BioSkryb's Supplier Dynamics: Pricing Power & Costs

The genomics market's reliance on key suppliers grants them substantial pricing power. BioSkryb's technology ties it to specific suppliers, raising switching costs, which in 2024 increased by 15-25%. Suppliers leverage product quality and innovation, especially those with strong ties to research institutions, influencing product adoption. Academic research spending in the U.S. reached $97.5 billion in 2023.

| Factor | Impact on BioSkryb | 2024 Data |

|---|---|---|

| Supplier Concentration | High bargaining power | Top 3 reagent suppliers controlled over 60% of the market. |

| Switching Costs | Increased dependency | Tech-specific integrations often increase switching costs by 15-25%. |

| Innovation & Relationships | Strategic advantage for suppliers | Single-cell analysis market valued at over $3 billion. |

Customers Bargaining Power

Diverse Customer Base

BioSkryb's diverse customer base, encompassing academic researchers, healthcare providers, and pharmaceutical companies, is a key strength. This broad reach helps to mitigate the risk of over-reliance on any single customer. In 2024, companies with diversified customer bases often report more stable revenue streams, as seen in the biotech sector. This diversification reduces the impact of any single customer's bargaining power.

Increasing Access to Information

Customers in the genomics market are increasingly informed, thanks to online resources and industry events. This transparency lets them easily compare technologies and prices. For example, in 2024, the global genomics market was valued at $24.8 billion, with customers having diverse choices. This empowers them to negotiate better terms, increasing their bargaining power.

Demand for Personalized Solutions and Data Integration

Customers increasingly demand personalized solutions and seamless data integration, particularly in genomics. BioSkryb must offer comprehensive, integrated workflows to meet these needs. This demand for customization empowers sophisticated customers, giving them leverage. The global genomics market, valued at $23.8 billion in 2023, underscores the importance of customer-centric strategies.

Price Sensitivity

Price sensitivity significantly impacts BioSkryb Genomics' customer bargaining power. The high cost of single-cell analysis tools and consumables, with some instruments costing over $200,000, makes customers price-conscious. This is especially true for academic institutions and smaller biotech firms. The availability of alternative, potentially cheaper, solutions strengthens customer leverage in negotiations.

- Instrument costs can exceed $200,000.

- Academic labs and small biotechs are particularly price-sensitive.

- Alternative solutions increase customer bargaining power.

Availability of In-House Capabilities

Some major players in the biotech and pharmaceutical sectors possess the resources to establish their own single-cell analysis departments. This internal capability diminishes their need for external services, like those offered by BioSkryb. Consequently, these entities gain leverage in price negotiations and service terms when they opt to outsource any part of their research. The trend of in-house lab development is growing; for example, in 2024, the National Institutes of Health invested $1.5 billion in advanced research facilities.

- Investment in internal capabilities reduces reliance on external providers.

- This increases bargaining power during outsourcing negotiations.

- Research institutions and pharma companies drive this trend.

- The NIH's 2024 investment highlights the growth.

Genomics Market Dynamics: Customer Power

BioSkryb's diverse customer base includes academic researchers, healthcare providers, and pharmaceutical companies, which helps spread risk. Informed customers in the genomics market, valued at $24.8B in 2024, can compare prices and negotiate. High costs, like instruments over $200,000, make customers price-sensitive, especially academic institutions.

| Factor | Impact | Data |

|---|---|---|

| Customer Knowledge | Increased Bargaining Power | Market size: $24.8B (2024) |

| Price Sensitivity | Higher Bargaining Power | Instruments >$200K |

| In-house Capabilities | Reduced Reliance | NIH invested $1.5B (2024) |

Rivalry Among Competitors

Presence of Established Players

The single-cell analysis market is fiercely competitive. Established players like 10x Genomics, Illumina, and Thermo Fisher Scientific dominate. These companies possess substantial resources and strong brand recognition. For instance, 10x Genomics reported $562 million in revenue for 2023. Intense rivalry is a key market characteristic.

Technological Advancements

Technological advancements are a major driver of competition in the genomics market. Companies constantly innovate, aiming for higher throughput and better accuracy. For example, in 2024, the NGS market reached $10.6 billion, reflecting intense competition among technology providers. This rapid pace of innovation forces companies to differentiate their offerings.

Focus on Multiomics

Competitive rivalry in multiomics is intensifying. The trend toward integrated multiomic analysis, combining various data types from single cells, is accelerating. Companies, including BioSkryb Genomics, compete by offering comprehensive workflows and analytical tools. The global genomics market, valued at $24.4 billion in 2023, is projected to reach $60.8 billion by 2030. This highlights the need for innovation.

Strategic Partnerships and Collaborations

Strategic partnerships and collaborations are prevalent in the genomics market, with companies teaming up to broaden their market presence. These alliances enable the integration of technologies and the creation of comprehensive solutions, intensifying rivalry. For example, in 2024, Illumina and Roche formed a partnership to improve cancer diagnostics. These collaborations provide customers with more integrated and accessible options, boosting competition.

- Illumina and Roche partnership in 2024 for cancer diagnostics.

- Partnerships can increase market reach and offer integrated solutions.

- These alliances boost competitive intensity.

- Collaboration examples include technology integration.

Market Growth Rate

The single-cell sequencing market's rapid growth fuels intense competition. This expansion draws in new entrants and substantial investments, intensifying the rivalry. The market, valued at $2.9 billion in 2024, is projected to reach $8.5 billion by 2029. The increased investment leads to a more dynamic and competitive setting.

- Market size in 2024: $2.9 billion.

- Projected market size by 2029: $8.5 billion.

- Annual growth rate: Approximately 24% (2024-2029).

- Key drivers: Technological advancements and increasing research demand.

Single-Cell Analysis: Fierce Competition & $2.9B Market

Competitive rivalry in the single-cell analysis market is very high. Established firms like 10x Genomics and Illumina compete fiercely. Technological advancements and strategic alliances further intensify competition. The single-cell sequencing market was $2.9 billion in 2024.

| Aspect | Details | Data |

|---|---|---|

| Key Players | Major Competitors | 10x Genomics, Illumina |

| Market Growth | Single-Cell Market (2024) | $2.9 Billion |

| Growth Rate | Projected (2024-2029) | ~24% Annually |