BOTBUILT PORTER'S FIVE FORCES TEMPLATE RESEARCH

What is included in the product

Tailored exclusively for BotBuilt, analyzing its position within its competitive landscape.

Quickly visualize industry competition with a customizable, dynamic dashboard.

Preview the Actual Deliverable

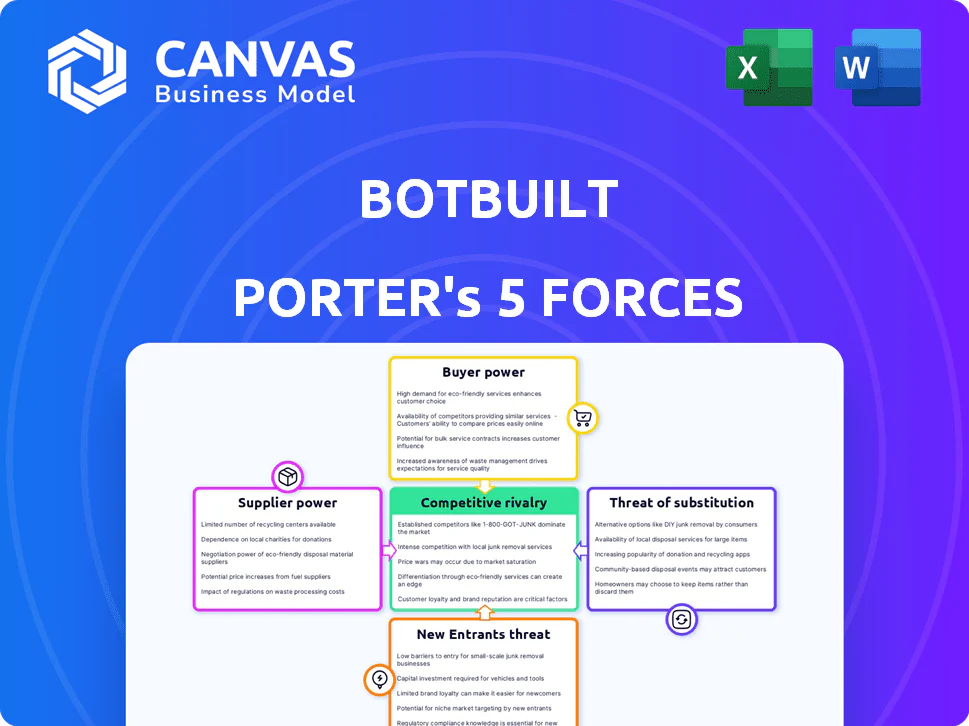

BotBuilt Porter's Five Forces Analysis

This preview showcases the complete BotBuilt Porter's Five Forces analysis report. It's the exact, ready-to-use document you'll download after purchase. No hidden parts, no alterations: what you see is what you get. The full analysis is formatted professionally for immediate application.

Porter's Five Forces Analysis Template

A Must-Have Tool for Decision-Makers

BotBuilt's industry is assessed via Porter's Five Forces. Buyer power is moderate due to diverse customer segments. Threat of new entrants is low, thanks to established market presence.

However, supplier power is high given reliance on critical tech. Competitive rivalry is intense, marked by key players. Substitute threats pose moderate risk, evolving industry dynamics.

Ready to move beyond the basics? Get a full strategic breakdown of BotBuilt’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Limited number of specialized suppliers for robotic components

BotBuilt depends on specialized robotic parts and AI software. The market for such tech might be concentrated, with fewer suppliers available. This scarcity gives suppliers leverage to set prices and dictate terms. In 2024, the robotics market saw a 12% increase in component costs due to supplier concentration.

Dependency on technology providers for AI software

BotBuilt relies on AI software, making it dependent on tech providers. These suppliers hold substantial bargaining power, especially if their tech is unique. For instance, AI software costs rose by 15% in 2024 due to high demand and specialized skills. This can squeeze BotBuilt's profits.

Potential for suppliers to integrate vertically

Some suppliers in robotics and AI could integrate vertically. This means they might enter BotBuilt's market or control more of the supply chain. Such moves could reduce BotBuilt's choices. In 2024, vertical integration trends show a rise in tech, with companies seeking greater control. This could increase supplier power over BotBuilt.

Quality and reliability of components are crucial

BotBuilt’s robotic systems' performance hinges on component quality and reliability. Suppliers of critical, high-quality parts can exert significant influence. This is especially true if these components are unique or essential for system functionality. A 2024 study revealed that 70% of robotics firms cite component reliability as their top concern.

- Component scarcity increases supplier power.

- Long-term contracts can mitigate supplier leverage.

- Supplier concentration affects bargaining power.

- Switching costs for BotBuilt are a factor.

Supply chain challenges impacting costs

Global supply chain disruptions can significantly influence BotBuilt's operational costs, particularly impacting the availability and pricing of vital components for its robots. Suppliers might gain leverage due to their own cost pressures and limited alternatives, potentially raising prices. This scenario underscores the need for BotBuilt to diversify its supplier base and possibly explore vertical integration to mitigate risks. In 2024, shipping costs, a key factor in supply chains, remained elevated, with the Drewry World Container Index showing fluctuations reflecting ongoing volatility.

- Shipping costs: Drewry World Container Index data for 2024 shows continued fluctuations.

- Supplier power: Increased if there are limited alternatives.

- Mitigation: Diversify suppliers and consider vertical integration.

Supplier Power Squeezes BotBuilt's Margins

BotBuilt faces supplier bargaining power due to specialized components and AI software dependency. Supplier concentration and vertical integration trends in 2024 amplified this power, affecting costs. High-quality, reliable components are crucial, increasing supplier influence, especially with limited alternatives.

| Factor | Impact on BotBuilt | 2024 Data |

|---|---|---|

| Component Scarcity | Higher costs, supply risks | Robotics component costs rose 12% |

| AI Software Dependency | Profit margin squeeze | AI software costs up 15% |

| Vertical Integration | Reduced choices | Tech companies seeking control |

Customers Bargaining Power

Customers are primarily homebuilders

BotBuilt's primary customers, homebuilders, significantly impact its bargaining power. These range from custom builders to large developers. In 2024, the U.S. housing market saw varied builder activity, with some regions experiencing stronger demand. The purchasing volume of these builders, influenced by market conditions and construction trends, affects their ability to negotiate prices. This dynamic is key to BotBuilt's profitability.

Customers seek efficiency and cost savings

Homebuilders aggressively seek efficiency and cost savings, driving their decision-making processes. BotBuilt's capacity to improve efficiency and reduce construction costs directly affects customer bargaining power. If BotBuilt's solutions significantly enhance value, customers may have limited negotiation leverage. In 2024, the construction industry faced 10% material cost increases, intensifying the need for cost-saving solutions.

Customers have alternative construction methods

BotBuilt faces customer bargaining power due to construction alternatives. Traditional methods and other prefabrication choices exist. This competition limits BotBuilt's pricing flexibility. In 2024, traditional construction held a significant market share, around 80% in many regions, illustrating customer choice.

Customer adoption of new technology can be slow

The construction industry's slow adoption of new technologies presents a challenge for BotBuilt. Customers might hesitate to switch from established methods, increasing their bargaining power. This hesitancy is reflected in the industry's digital transformation, with only 36% of construction firms highly investing in technology in 2024. This can lead to slower adoption rates and potentially impact BotBuilt's market penetration.

- Construction tech spending is projected to reach $30.1 billion by 2027.

- Only 36% of construction firms are highly investing in technology (2024).

- The construction industry's productivity has only increased by 1% annually over the last 20 years.

- Cost overruns in construction projects average 20%.

Large builders may have significant leverage

BotBuilt's dealings with large builders, including top-tier ones, highlight customer bargaining power. These major clients, such as the top-20 builder, wield considerable influence due to their substantial purchasing volumes. This leverage allows them to negotiate more favorable pricing and contract terms.

- Large builders represent significant revenue streams, increasing their negotiation power.

- Volume discounts are likely a factor, impacting BotBuilt's profitability.

- Customer concentration could be a risk if a major builder switches suppliers.

- Contract terms can influence payment schedules and project timelines.

BotBuilt's Profitability: Homebuilders' Influence

Homebuilders' purchasing power is a key factor for BotBuilt. Their ability to negotiate prices depends on market conditions and construction trends. The construction industry saw 10% material cost increases in 2024. This impacts BotBuilt's ability to maintain profitability.

| Aspect | Impact | Data (2024) |

|---|---|---|

| Customer Base | Negotiation Power | Traditional construction: 80% market share. |

| Cost Pressure | Pricing Flexibility | Material cost increases: 10%. |

| Tech Adoption | Market Penetration | Tech investment: 36% of firms. |

Rivalry Among Competitors

Presence of direct competitors in construction tech

BotBuilt, a construction tech firm, competes with direct rivals in the robotic and AI construction space. RoboConstruct and AI BuildTech are key competitors. The global construction robotics market, valued at $101.9 million in 2024, is projected to reach $207.5 million by 2029, with a CAGR of 15.33% from 2024 to 2029. This intense competition necessitates BotBuilt to continually innovate to maintain market share.

Competition from traditional construction methods

BotBuilt faces intense competition from established traditional construction methods, a sector deeply entrenched in the industry. These traditional methods benefit from decades of experience and established supply chains. The construction industry in 2024 showed that traditional methods still constitute over 95% of the market share. Overcoming the inertia and perceived reliability of these long-standing methods is a key challenge for BotBuilt.

Rivalry from other automated construction companies

BotBuilt confronts competition from firms beyond robotic framing, including those in automated construction like 3D printing. In 2024, the 3D construction market was valued at approximately $65 million, with projections for significant growth. Companies such as ICON and Mighty Buildings are key players. This rivalry intensifies as technology advances and construction methods evolve, potentially impacting BotBuilt's market share.

Different approaches to automation in construction

Competitive rivalry in construction automation is intense due to diverse approaches. Companies like Katerra and Autovol have explored prefabrication and modular construction. These different strategies intensify competition, as firms compete to prove their methods’ efficiency. For instance, the global modular construction market was valued at $62.8 billion in 2022 and is projected to reach $108.4 billion by 2028.

- Prefabrication and modular construction are key competitive areas.

- Companies are vying for market share by demonstrating effectiveness.

- The modular construction market is rapidly growing.

- Differentiation in automation approaches increases rivalry.

Need to differentiate through technology and value proposition

BotBuilt faces intense competition, requiring differentiation. To succeed, it must highlight its unique flexible robotic systems and AI. This includes emphasizing speed, precision, safety, and cost-effectiveness to customers.

- Robotics market is projected to reach $214 billion by 2028.

- AI in robotics is expected to grow significantly.

- Focus on value, like a 20% cost reduction.

- Highlight speed improvements.

BotBuilt's Competitive Landscape: Market Share and Rivals

BotBuilt faces intense competition within the construction tech market, including rivals in robotics and AI. Traditional construction methods, holding over 95% of the 2024 market share, pose a significant challenge. Competition also comes from firms like ICON and Mighty Buildings in 3D construction, valued around $65 million in 2024. This requires BotBuilt to differentiate itself.

| Aspect | Data | Implication for BotBuilt |

|---|---|---|

| Robotics Market (2024) | $101.9M, CAGR 15.33% (2024-2029) | Must innovate to compete |

| 3D Construction Market (2024) | ~$65M | Faces growing competition |

| Modular Construction Market (2022) | $62.8B, projected to $108.4B by 2028 | Competition from modular construction |

BOTBUILT PORTER'S FIVE FORCES TEMPLATE RESEARCH

What is included in the product

Tailored exclusively for BotBuilt, analyzing its position within its competitive landscape.

Quickly visualize industry competition with a customizable, dynamic dashboard.

Preview the Actual Deliverable

BotBuilt Porter's Five Forces Analysis

This preview showcases the complete BotBuilt Porter's Five Forces analysis report. It's the exact, ready-to-use document you'll download after purchase. No hidden parts, no alterations: what you see is what you get. The full analysis is formatted professionally for immediate application.

Porter's Five Forces Analysis Template

A Must-Have Tool for Decision-Makers

BotBuilt's industry is assessed via Porter's Five Forces. Buyer power is moderate due to diverse customer segments. Threat of new entrants is low, thanks to established market presence.

However, supplier power is high given reliance on critical tech. Competitive rivalry is intense, marked by key players. Substitute threats pose moderate risk, evolving industry dynamics.

Ready to move beyond the basics? Get a full strategic breakdown of BotBuilt’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Limited number of specialized suppliers for robotic components

BotBuilt depends on specialized robotic parts and AI software. The market for such tech might be concentrated, with fewer suppliers available. This scarcity gives suppliers leverage to set prices and dictate terms. In 2024, the robotics market saw a 12% increase in component costs due to supplier concentration.

Dependency on technology providers for AI software

BotBuilt relies on AI software, making it dependent on tech providers. These suppliers hold substantial bargaining power, especially if their tech is unique. For instance, AI software costs rose by 15% in 2024 due to high demand and specialized skills. This can squeeze BotBuilt's profits.

Potential for suppliers to integrate vertically

Some suppliers in robotics and AI could integrate vertically. This means they might enter BotBuilt's market or control more of the supply chain. Such moves could reduce BotBuilt's choices. In 2024, vertical integration trends show a rise in tech, with companies seeking greater control. This could increase supplier power over BotBuilt.

Quality and reliability of components are crucial

BotBuilt’s robotic systems' performance hinges on component quality and reliability. Suppliers of critical, high-quality parts can exert significant influence. This is especially true if these components are unique or essential for system functionality. A 2024 study revealed that 70% of robotics firms cite component reliability as their top concern.

- Component scarcity increases supplier power.

- Long-term contracts can mitigate supplier leverage.

- Supplier concentration affects bargaining power.

- Switching costs for BotBuilt are a factor.

Supply chain challenges impacting costs

Global supply chain disruptions can significantly influence BotBuilt's operational costs, particularly impacting the availability and pricing of vital components for its robots. Suppliers might gain leverage due to their own cost pressures and limited alternatives, potentially raising prices. This scenario underscores the need for BotBuilt to diversify its supplier base and possibly explore vertical integration to mitigate risks. In 2024, shipping costs, a key factor in supply chains, remained elevated, with the Drewry World Container Index showing fluctuations reflecting ongoing volatility.

- Shipping costs: Drewry World Container Index data for 2024 shows continued fluctuations.

- Supplier power: Increased if there are limited alternatives.

- Mitigation: Diversify suppliers and consider vertical integration.

Supplier Power Squeezes BotBuilt's Margins

BotBuilt faces supplier bargaining power due to specialized components and AI software dependency. Supplier concentration and vertical integration trends in 2024 amplified this power, affecting costs. High-quality, reliable components are crucial, increasing supplier influence, especially with limited alternatives.

| Factor | Impact on BotBuilt | 2024 Data |

|---|---|---|

| Component Scarcity | Higher costs, supply risks | Robotics component costs rose 12% |

| AI Software Dependency | Profit margin squeeze | AI software costs up 15% |

| Vertical Integration | Reduced choices | Tech companies seeking control |

Customers Bargaining Power

Customers are primarily homebuilders

BotBuilt's primary customers, homebuilders, significantly impact its bargaining power. These range from custom builders to large developers. In 2024, the U.S. housing market saw varied builder activity, with some regions experiencing stronger demand. The purchasing volume of these builders, influenced by market conditions and construction trends, affects their ability to negotiate prices. This dynamic is key to BotBuilt's profitability.

Customers seek efficiency and cost savings

Homebuilders aggressively seek efficiency and cost savings, driving their decision-making processes. BotBuilt's capacity to improve efficiency and reduce construction costs directly affects customer bargaining power. If BotBuilt's solutions significantly enhance value, customers may have limited negotiation leverage. In 2024, the construction industry faced 10% material cost increases, intensifying the need for cost-saving solutions.

Customers have alternative construction methods

BotBuilt faces customer bargaining power due to construction alternatives. Traditional methods and other prefabrication choices exist. This competition limits BotBuilt's pricing flexibility. In 2024, traditional construction held a significant market share, around 80% in many regions, illustrating customer choice.

Customer adoption of new technology can be slow

The construction industry's slow adoption of new technologies presents a challenge for BotBuilt. Customers might hesitate to switch from established methods, increasing their bargaining power. This hesitancy is reflected in the industry's digital transformation, with only 36% of construction firms highly investing in technology in 2024. This can lead to slower adoption rates and potentially impact BotBuilt's market penetration.

- Construction tech spending is projected to reach $30.1 billion by 2027.

- Only 36% of construction firms are highly investing in technology (2024).

- The construction industry's productivity has only increased by 1% annually over the last 20 years.

- Cost overruns in construction projects average 20%.

Large builders may have significant leverage

BotBuilt's dealings with large builders, including top-tier ones, highlight customer bargaining power. These major clients, such as the top-20 builder, wield considerable influence due to their substantial purchasing volumes. This leverage allows them to negotiate more favorable pricing and contract terms.

- Large builders represent significant revenue streams, increasing their negotiation power.

- Volume discounts are likely a factor, impacting BotBuilt's profitability.

- Customer concentration could be a risk if a major builder switches suppliers.

- Contract terms can influence payment schedules and project timelines.

BotBuilt's Profitability: Homebuilders' Influence

Homebuilders' purchasing power is a key factor for BotBuilt. Their ability to negotiate prices depends on market conditions and construction trends. The construction industry saw 10% material cost increases in 2024. This impacts BotBuilt's ability to maintain profitability.

| Aspect | Impact | Data (2024) |

|---|---|---|

| Customer Base | Negotiation Power | Traditional construction: 80% market share. |

| Cost Pressure | Pricing Flexibility | Material cost increases: 10%. |

| Tech Adoption | Market Penetration | Tech investment: 36% of firms. |

Rivalry Among Competitors

Presence of direct competitors in construction tech

BotBuilt, a construction tech firm, competes with direct rivals in the robotic and AI construction space. RoboConstruct and AI BuildTech are key competitors. The global construction robotics market, valued at $101.9 million in 2024, is projected to reach $207.5 million by 2029, with a CAGR of 15.33% from 2024 to 2029. This intense competition necessitates BotBuilt to continually innovate to maintain market share.

Competition from traditional construction methods

BotBuilt faces intense competition from established traditional construction methods, a sector deeply entrenched in the industry. These traditional methods benefit from decades of experience and established supply chains. The construction industry in 2024 showed that traditional methods still constitute over 95% of the market share. Overcoming the inertia and perceived reliability of these long-standing methods is a key challenge for BotBuilt.

Rivalry from other automated construction companies

BotBuilt confronts competition from firms beyond robotic framing, including those in automated construction like 3D printing. In 2024, the 3D construction market was valued at approximately $65 million, with projections for significant growth. Companies such as ICON and Mighty Buildings are key players. This rivalry intensifies as technology advances and construction methods evolve, potentially impacting BotBuilt's market share.

Different approaches to automation in construction

Competitive rivalry in construction automation is intense due to diverse approaches. Companies like Katerra and Autovol have explored prefabrication and modular construction. These different strategies intensify competition, as firms compete to prove their methods’ efficiency. For instance, the global modular construction market was valued at $62.8 billion in 2022 and is projected to reach $108.4 billion by 2028.

- Prefabrication and modular construction are key competitive areas.

- Companies are vying for market share by demonstrating effectiveness.

- The modular construction market is rapidly growing.

- Differentiation in automation approaches increases rivalry.

Need to differentiate through technology and value proposition

BotBuilt faces intense competition, requiring differentiation. To succeed, it must highlight its unique flexible robotic systems and AI. This includes emphasizing speed, precision, safety, and cost-effectiveness to customers.

- Robotics market is projected to reach $214 billion by 2028.

- AI in robotics is expected to grow significantly.

- Focus on value, like a 20% cost reduction.

- Highlight speed improvements.

BotBuilt's Competitive Landscape: Market Share and Rivals

BotBuilt faces intense competition within the construction tech market, including rivals in robotics and AI. Traditional construction methods, holding over 95% of the 2024 market share, pose a significant challenge. Competition also comes from firms like ICON and Mighty Buildings in 3D construction, valued around $65 million in 2024. This requires BotBuilt to differentiate itself.

| Aspect | Data | Implication for BotBuilt |

|---|---|---|

| Robotics Market (2024) | $101.9M, CAGR 15.33% (2024-2029) | Must innovate to compete |

| 3D Construction Market (2024) | ~$65M | Faces growing competition |

| Modular Construction Market (2022) | $62.8B, projected to $108.4B by 2028 | Competition from modular construction |

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

What is included in the product

Tailored exclusively for BotBuilt, analyzing its position within its competitive landscape.

Quickly visualize industry competition with a customizable, dynamic dashboard.

Preview the Actual Deliverable

BotBuilt Porter's Five Forces Analysis

This preview showcases the complete BotBuilt Porter's Five Forces analysis report. It's the exact, ready-to-use document you'll download after purchase. No hidden parts, no alterations: what you see is what you get. The full analysis is formatted professionally for immediate application.

Porter's Five Forces Analysis Template

A Must-Have Tool for Decision-Makers

BotBuilt's industry is assessed via Porter's Five Forces. Buyer power is moderate due to diverse customer segments. Threat of new entrants is low, thanks to established market presence.

However, supplier power is high given reliance on critical tech. Competitive rivalry is intense, marked by key players. Substitute threats pose moderate risk, evolving industry dynamics.

Ready to move beyond the basics? Get a full strategic breakdown of BotBuilt’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Limited number of specialized suppliers for robotic components

BotBuilt depends on specialized robotic parts and AI software. The market for such tech might be concentrated, with fewer suppliers available. This scarcity gives suppliers leverage to set prices and dictate terms. In 2024, the robotics market saw a 12% increase in component costs due to supplier concentration.

Dependency on technology providers for AI software

BotBuilt relies on AI software, making it dependent on tech providers. These suppliers hold substantial bargaining power, especially if their tech is unique. For instance, AI software costs rose by 15% in 2024 due to high demand and specialized skills. This can squeeze BotBuilt's profits.

Potential for suppliers to integrate vertically

Some suppliers in robotics and AI could integrate vertically. This means they might enter BotBuilt's market or control more of the supply chain. Such moves could reduce BotBuilt's choices. In 2024, vertical integration trends show a rise in tech, with companies seeking greater control. This could increase supplier power over BotBuilt.

Quality and reliability of components are crucial

BotBuilt’s robotic systems' performance hinges on component quality and reliability. Suppliers of critical, high-quality parts can exert significant influence. This is especially true if these components are unique or essential for system functionality. A 2024 study revealed that 70% of robotics firms cite component reliability as their top concern.

- Component scarcity increases supplier power.

- Long-term contracts can mitigate supplier leverage.

- Supplier concentration affects bargaining power.

- Switching costs for BotBuilt are a factor.

Supply chain challenges impacting costs

Global supply chain disruptions can significantly influence BotBuilt's operational costs, particularly impacting the availability and pricing of vital components for its robots. Suppliers might gain leverage due to their own cost pressures and limited alternatives, potentially raising prices. This scenario underscores the need for BotBuilt to diversify its supplier base and possibly explore vertical integration to mitigate risks. In 2024, shipping costs, a key factor in supply chains, remained elevated, with the Drewry World Container Index showing fluctuations reflecting ongoing volatility.

- Shipping costs: Drewry World Container Index data for 2024 shows continued fluctuations.

- Supplier power: Increased if there are limited alternatives.

- Mitigation: Diversify suppliers and consider vertical integration.

Supplier Power Squeezes BotBuilt's Margins

BotBuilt faces supplier bargaining power due to specialized components and AI software dependency. Supplier concentration and vertical integration trends in 2024 amplified this power, affecting costs. High-quality, reliable components are crucial, increasing supplier influence, especially with limited alternatives.

| Factor | Impact on BotBuilt | 2024 Data |

|---|---|---|

| Component Scarcity | Higher costs, supply risks | Robotics component costs rose 12% |

| AI Software Dependency | Profit margin squeeze | AI software costs up 15% |

| Vertical Integration | Reduced choices | Tech companies seeking control |

Customers Bargaining Power

Customers are primarily homebuilders

BotBuilt's primary customers, homebuilders, significantly impact its bargaining power. These range from custom builders to large developers. In 2024, the U.S. housing market saw varied builder activity, with some regions experiencing stronger demand. The purchasing volume of these builders, influenced by market conditions and construction trends, affects their ability to negotiate prices. This dynamic is key to BotBuilt's profitability.

Customers seek efficiency and cost savings

Homebuilders aggressively seek efficiency and cost savings, driving their decision-making processes. BotBuilt's capacity to improve efficiency and reduce construction costs directly affects customer bargaining power. If BotBuilt's solutions significantly enhance value, customers may have limited negotiation leverage. In 2024, the construction industry faced 10% material cost increases, intensifying the need for cost-saving solutions.

Customers have alternative construction methods

BotBuilt faces customer bargaining power due to construction alternatives. Traditional methods and other prefabrication choices exist. This competition limits BotBuilt's pricing flexibility. In 2024, traditional construction held a significant market share, around 80% in many regions, illustrating customer choice.

Customer adoption of new technology can be slow

The construction industry's slow adoption of new technologies presents a challenge for BotBuilt. Customers might hesitate to switch from established methods, increasing their bargaining power. This hesitancy is reflected in the industry's digital transformation, with only 36% of construction firms highly investing in technology in 2024. This can lead to slower adoption rates and potentially impact BotBuilt's market penetration.

- Construction tech spending is projected to reach $30.1 billion by 2027.

- Only 36% of construction firms are highly investing in technology (2024).

- The construction industry's productivity has only increased by 1% annually over the last 20 years.

- Cost overruns in construction projects average 20%.

Large builders may have significant leverage

BotBuilt's dealings with large builders, including top-tier ones, highlight customer bargaining power. These major clients, such as the top-20 builder, wield considerable influence due to their substantial purchasing volumes. This leverage allows them to negotiate more favorable pricing and contract terms.

- Large builders represent significant revenue streams, increasing their negotiation power.

- Volume discounts are likely a factor, impacting BotBuilt's profitability.

- Customer concentration could be a risk if a major builder switches suppliers.

- Contract terms can influence payment schedules and project timelines.

BotBuilt's Profitability: Homebuilders' Influence

Homebuilders' purchasing power is a key factor for BotBuilt. Their ability to negotiate prices depends on market conditions and construction trends. The construction industry saw 10% material cost increases in 2024. This impacts BotBuilt's ability to maintain profitability.

| Aspect | Impact | Data (2024) |

|---|---|---|

| Customer Base | Negotiation Power | Traditional construction: 80% market share. |

| Cost Pressure | Pricing Flexibility | Material cost increases: 10%. |

| Tech Adoption | Market Penetration | Tech investment: 36% of firms. |

Rivalry Among Competitors

Presence of direct competitors in construction tech

BotBuilt, a construction tech firm, competes with direct rivals in the robotic and AI construction space. RoboConstruct and AI BuildTech are key competitors. The global construction robotics market, valued at $101.9 million in 2024, is projected to reach $207.5 million by 2029, with a CAGR of 15.33% from 2024 to 2029. This intense competition necessitates BotBuilt to continually innovate to maintain market share.

Competition from traditional construction methods

BotBuilt faces intense competition from established traditional construction methods, a sector deeply entrenched in the industry. These traditional methods benefit from decades of experience and established supply chains. The construction industry in 2024 showed that traditional methods still constitute over 95% of the market share. Overcoming the inertia and perceived reliability of these long-standing methods is a key challenge for BotBuilt.

Rivalry from other automated construction companies

BotBuilt confronts competition from firms beyond robotic framing, including those in automated construction like 3D printing. In 2024, the 3D construction market was valued at approximately $65 million, with projections for significant growth. Companies such as ICON and Mighty Buildings are key players. This rivalry intensifies as technology advances and construction methods evolve, potentially impacting BotBuilt's market share.

Different approaches to automation in construction

Competitive rivalry in construction automation is intense due to diverse approaches. Companies like Katerra and Autovol have explored prefabrication and modular construction. These different strategies intensify competition, as firms compete to prove their methods’ efficiency. For instance, the global modular construction market was valued at $62.8 billion in 2022 and is projected to reach $108.4 billion by 2028.

- Prefabrication and modular construction are key competitive areas.

- Companies are vying for market share by demonstrating effectiveness.

- The modular construction market is rapidly growing.

- Differentiation in automation approaches increases rivalry.

Need to differentiate through technology and value proposition

BotBuilt faces intense competition, requiring differentiation. To succeed, it must highlight its unique flexible robotic systems and AI. This includes emphasizing speed, precision, safety, and cost-effectiveness to customers.

- Robotics market is projected to reach $214 billion by 2028.

- AI in robotics is expected to grow significantly.

- Focus on value, like a 20% cost reduction.

- Highlight speed improvements.

BotBuilt's Competitive Landscape: Market Share and Rivals

BotBuilt faces intense competition within the construction tech market, including rivals in robotics and AI. Traditional construction methods, holding over 95% of the 2024 market share, pose a significant challenge. Competition also comes from firms like ICON and Mighty Buildings in 3D construction, valued around $65 million in 2024. This requires BotBuilt to differentiate itself.

| Aspect | Data | Implication for BotBuilt |

|---|---|---|

| Robotics Market (2024) | $101.9M, CAGR 15.33% (2024-2029) | Must innovate to compete |

| 3D Construction Market (2024) | ~$65M | Faces growing competition |

| Modular Construction Market (2022) | $62.8B, projected to $108.4B by 2028 | Competition from modular construction |