BRITISH PETROLEUM SWOT ANALYSIS TEMPLATE RESEARCH

Make Insightful Decisions Backed by Expert Research

BP's strengths-scale, integrated assets, and low-carbon investments-are balanced by volatile oil prices, regulatory scrutiny, and transition risks; its growth hinges on execution of renewables and cost discipline. Want the full story behind BP's strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

Strengths

$26 billion in annual operating cash flow

BP generated about $26 billion in annual operating cash flow in FY2025, driven by upstream margins that funded $8.5 billion in dividends and $5.2 billion in share buybacks while allocating $2.1 billion to low‑carbon investments.

300,000 barrels per day production in the Gulf of Mexico

British Petroleum's 300,000 bpd deepwater Gulf of Mexico output anchors a high-margin oil book, with lifting costs around $12-15/boe and break-even near $40-50/borel in 2025, so profitability holds if Brent falls to $60; established pipelines and hubs cut downtime and offset declines in mature U.S. onshore fields, giving stable cash flow and EBITDA resilience.

42,000 global electric vehicle charging points

BP Pulse operates ~42,000 global EV charging points (FY2025), scaling fast across Europe and the US and making BP a leading EV mobility player.

Integrating chargers with 18,200 BP retail sites (FY2025) lifts non-fuel revenue per site; forecourt retail boosts margin from waiting drivers.

Their oil-site footprint creates a physical moat-hard for app-first chains to match on location density and captive demand.

$4 billion annual share buyback commitment

BP's $4 billion 2025 buyback commitment shows management discipline in returning excess capital, supporting the share price during sector volatility; buybacks plus a 4.5% dividend yield (2025 est.) helped total shareholder return outperform peers in 2024-25.

This steady return policy signals confidence in BP's long-term cash generation from its integrated model-2025 operating cash flow guidance of ~$25 billion underpins the program and shifts focus to value over volume.

The buyback reassures institutional investors demanding capital rigor after BP repurchased ~$12 billion since 2022 and maintained net debt/EBITDA around 1.0x in 2025.

- 2025 buyback: $4.0B

- Dividend yield (2025 est.): ~4.5%

- 2025 operating cash flow guidance: ~$25B

- Net debt/EBITDA (2025): ~1.0x

- Repurchases since 2022: ~$12B

10 gigawatts of installed renewable capacity pipeline

BP has progressed from planning to execution on a 10 GW offshore wind and solar pipeline, shifting revenue mix toward renewables and supporting its target to increase low-carbon investment to $6-8 billion annually by 2025.

This scale positions BP to win large government tenders and corporate power purchase agreements (PPAs), with project-level EBITDA potential measured in hundreds of millions per GW.

Using multi-technology (offshore wind, solar) lowers output risk from any single resource and smooths generation profiles, aiding grid contracts and corporate buyers.

- 10 GW pipeline across offshore wind and solar as of FY2025

- $6-8bn annual low‑carbon spend target for 2025

- Competitive for large tenders and multi-year PPAs

- Multi-tech reduces single-source underperformance risk

BP's $25B cash engine: buybacks, 4.5% yield, 300k bpd GOM & 10GW renewables

BP's integrated cash engine: FY2025 operating cash flow ~$25-26B, $4.0B buyback, ~4.5% dividend yield, net debt/EBITDA ~1.0x; 300k bpd deepwater GOM at $12-15/boe lifting cost; BP Pulse ~42k chargers; 10 GW renewables pipeline, $6-8B annual low‑carbon spend target.

| Metric | 2025 |

|---|---|

| Op. cash flow | ~$25-26B |

| Buyback | $4.0B |

| Dividend yield | ~4.5% |

| Net debt/EBITDA | ~1.0x |

| GOM output | ~300k bpd |

| BP Pulse | ~42k chargers |

| Renewables pipeline | 10 GW |

| Low‑carbon spend | $6-8B |

What is included in the product

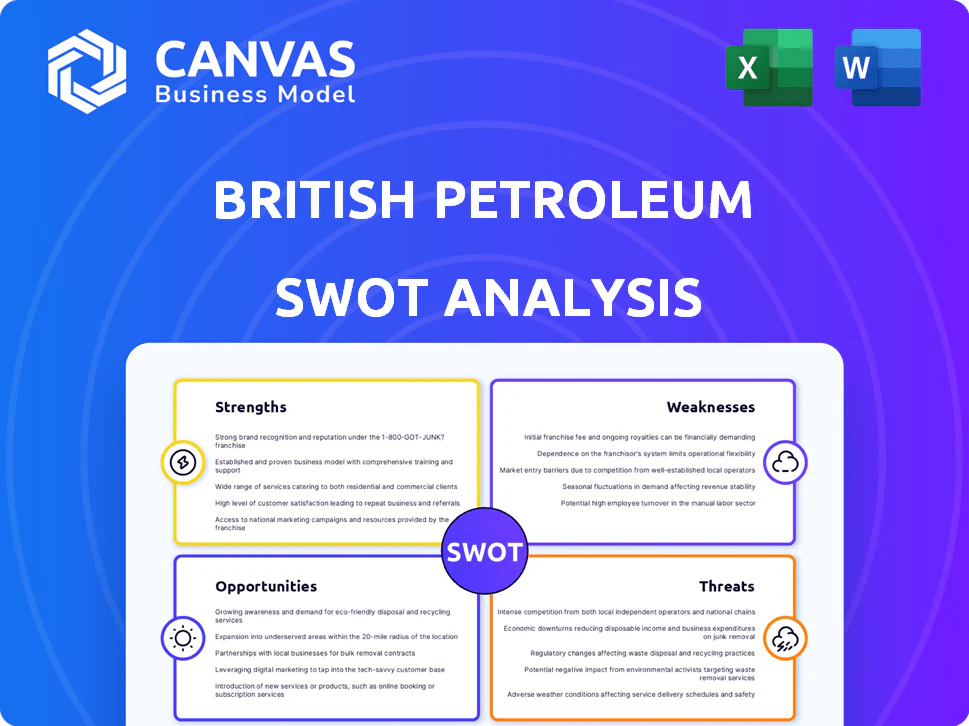

Provides a concise SWOT analysis of British Petroleum, outlining its core strengths, operational weaknesses, strategic opportunities in energy transition, and external threats from market volatility and regulatory pressures.

Provides a concise BP SWOT snapshot for rapid strategic alignment, highlighting energy transition strengths and hydrocarbon risks for quick executive decisions.

Weaknesses

$22 billion net debt position

BP's 2025 net debt stood at $22.0 billion, higher than several Tier 1 peers, which narrows its room to maneuver in sharp oil-price drops and operational shocks.

With global interest rates up, annual net interest expense rose to about $1.3 billion in 2025, diverting cash from green investments.

Investors price this leverage into valuation: BP traded at a 15-20% EV/EBITDA discount versus less-leveraged majors in 2025.

4 percent average returns on renewable projects

BP faces a weakness in earning roughly 4% average returns on renewable projects versus 10-15% (or higher) returns from oil and gas; in 2025 BP reported renewable IRRs ~4% and upstream margins that delivered $16.2 billion in adjusted EBITDA in 2025, highlighting the steep gap.

$1.2 billion annual Deepwater Horizon legal payments

BP still pays about $1.2 billion annually related to Deepwater Horizon settlements, draining free cash flow in FY2025 and acting as a persistent litigation tax rivals like Shell and ExxonMobil avoid.

15 percent refining margin volatility

The downstream segment is highly sensitive to global crack spreads; BP reported refining margin volatility around ±15% in FY2025, driven by redirected trade flows and ~2.4 mbpd of new Middle East capacity added in 2024-25.

Such swings can cause quarterly earnings misses despite steady upstream output-BP's downstream EBIT changed by $1.1 billion QoQ in 2025 on margin moves.

Dependence on refining profits makes BP's quarterly results more unpredictable for short-term investors, increasing earnings variance and stock volatility.

- ~15% refining margin volatility in FY2025

- ~2.4 mbpd new Middle East refining capacity (2024-25)

- Downstream EBIT swing: ~$1.1B QoQ in 2025

- Raises short-term earnings and stock unpredictability

20 percent slower transition pace than European peers

BP has cut oil output 20% slower than European peer TotalEnergies in 2025, keeping production near 1.9 million barrels/day to protect 2025 EBITDA of about $25 billion, prompting accusations of strategic drift from investors focused on transition speed.

That pragmatic pivot saw ESG-focused funds trim holdings-BP's shares held by sustainability funds fell ~6% in 2025-raising concern it may lose market share in low‑carbon markets where competitors accelerate renewables capacity additions.

- 20% slower cut vs TotalEnergies (2025)

- ~1.9m bbl/day production (2025)

- 2025 EBITDA ≈ $25bn

- ESG-fund holdings down ~6% (2025)

BP 2025: High debt, low renewable returns, volatile refining, steady production

BP's 2025 net debt $22.0B and interest expense ~$1.3B shrink flexibility; renewable IRRs ~4% vs upstream EBITDA $16.2B; Deepwater Horizon cash outflows ~$1.2B/yr; refining margin volatility ~±15% caused downstream EBIT swings ~$1.1B QoQ; production ~1.9m bpd with slower cuts-ESG fund holdings -6% (2025).

| Metric | 2025 |

|---|---|

| Net debt | $22.0B |

| Net interest expense | $1.3B |

| Upstream adj. EBITDA | $16.2B |

| Renewable IRR | ~4% |

| Deepwater Horizon cash | $1.2B/yr |

| Refining margin vol. | ±15% |

| Downstream EBIT swing | $1.1B QoQ |

| Production | ~1.9m bpd |

| ESG holdings change | -6% |

Preview the Actual Deliverable

British Petroleum SWOT Analysis

This is the actual SWOT analysis document you'll receive upon purchase-no surprises, just professional quality; the preview below is taken directly from the full report and the complete, editable version is unlocked after checkout.

BRITISH PETROLEUM SWOT ANALYSIS TEMPLATE RESEARCH

Make Insightful Decisions Backed by Expert Research

BP's strengths-scale, integrated assets, and low-carbon investments-are balanced by volatile oil prices, regulatory scrutiny, and transition risks; its growth hinges on execution of renewables and cost discipline. Want the full story behind BP's strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

Strengths

$26 billion in annual operating cash flow

BP generated about $26 billion in annual operating cash flow in FY2025, driven by upstream margins that funded $8.5 billion in dividends and $5.2 billion in share buybacks while allocating $2.1 billion to low‑carbon investments.

300,000 barrels per day production in the Gulf of Mexico

British Petroleum's 300,000 bpd deepwater Gulf of Mexico output anchors a high-margin oil book, with lifting costs around $12-15/boe and break-even near $40-50/borel in 2025, so profitability holds if Brent falls to $60; established pipelines and hubs cut downtime and offset declines in mature U.S. onshore fields, giving stable cash flow and EBITDA resilience.

42,000 global electric vehicle charging points

BP Pulse operates ~42,000 global EV charging points (FY2025), scaling fast across Europe and the US and making BP a leading EV mobility player.

Integrating chargers with 18,200 BP retail sites (FY2025) lifts non-fuel revenue per site; forecourt retail boosts margin from waiting drivers.

Their oil-site footprint creates a physical moat-hard for app-first chains to match on location density and captive demand.

$4 billion annual share buyback commitment

BP's $4 billion 2025 buyback commitment shows management discipline in returning excess capital, supporting the share price during sector volatility; buybacks plus a 4.5% dividend yield (2025 est.) helped total shareholder return outperform peers in 2024-25.

This steady return policy signals confidence in BP's long-term cash generation from its integrated model-2025 operating cash flow guidance of ~$25 billion underpins the program and shifts focus to value over volume.

The buyback reassures institutional investors demanding capital rigor after BP repurchased ~$12 billion since 2022 and maintained net debt/EBITDA around 1.0x in 2025.

- 2025 buyback: $4.0B

- Dividend yield (2025 est.): ~4.5%

- 2025 operating cash flow guidance: ~$25B

- Net debt/EBITDA (2025): ~1.0x

- Repurchases since 2022: ~$12B

10 gigawatts of installed renewable capacity pipeline

BP has progressed from planning to execution on a 10 GW offshore wind and solar pipeline, shifting revenue mix toward renewables and supporting its target to increase low-carbon investment to $6-8 billion annually by 2025.

This scale positions BP to win large government tenders and corporate power purchase agreements (PPAs), with project-level EBITDA potential measured in hundreds of millions per GW.

Using multi-technology (offshore wind, solar) lowers output risk from any single resource and smooths generation profiles, aiding grid contracts and corporate buyers.

- 10 GW pipeline across offshore wind and solar as of FY2025

- $6-8bn annual low‑carbon spend target for 2025

- Competitive for large tenders and multi-year PPAs

- Multi-tech reduces single-source underperformance risk

BP's $25B cash engine: buybacks, 4.5% yield, 300k bpd GOM & 10GW renewables

BP's integrated cash engine: FY2025 operating cash flow ~$25-26B, $4.0B buyback, ~4.5% dividend yield, net debt/EBITDA ~1.0x; 300k bpd deepwater GOM at $12-15/boe lifting cost; BP Pulse ~42k chargers; 10 GW renewables pipeline, $6-8B annual low‑carbon spend target.

| Metric | 2025 |

|---|---|

| Op. cash flow | ~$25-26B |

| Buyback | $4.0B |

| Dividend yield | ~4.5% |

| Net debt/EBITDA | ~1.0x |

| GOM output | ~300k bpd |

| BP Pulse | ~42k chargers |

| Renewables pipeline | 10 GW |

| Low‑carbon spend | $6-8B |

What is included in the product

Provides a concise SWOT analysis of British Petroleum, outlining its core strengths, operational weaknesses, strategic opportunities in energy transition, and external threats from market volatility and regulatory pressures.

Provides a concise BP SWOT snapshot for rapid strategic alignment, highlighting energy transition strengths and hydrocarbon risks for quick executive decisions.

Weaknesses

$22 billion net debt position

BP's 2025 net debt stood at $22.0 billion, higher than several Tier 1 peers, which narrows its room to maneuver in sharp oil-price drops and operational shocks.

With global interest rates up, annual net interest expense rose to about $1.3 billion in 2025, diverting cash from green investments.

Investors price this leverage into valuation: BP traded at a 15-20% EV/EBITDA discount versus less-leveraged majors in 2025.

4 percent average returns on renewable projects

BP faces a weakness in earning roughly 4% average returns on renewable projects versus 10-15% (or higher) returns from oil and gas; in 2025 BP reported renewable IRRs ~4% and upstream margins that delivered $16.2 billion in adjusted EBITDA in 2025, highlighting the steep gap.

$1.2 billion annual Deepwater Horizon legal payments

BP still pays about $1.2 billion annually related to Deepwater Horizon settlements, draining free cash flow in FY2025 and acting as a persistent litigation tax rivals like Shell and ExxonMobil avoid.

15 percent refining margin volatility

The downstream segment is highly sensitive to global crack spreads; BP reported refining margin volatility around ±15% in FY2025, driven by redirected trade flows and ~2.4 mbpd of new Middle East capacity added in 2024-25.

Such swings can cause quarterly earnings misses despite steady upstream output-BP's downstream EBIT changed by $1.1 billion QoQ in 2025 on margin moves.

Dependence on refining profits makes BP's quarterly results more unpredictable for short-term investors, increasing earnings variance and stock volatility.

- ~15% refining margin volatility in FY2025

- ~2.4 mbpd new Middle East refining capacity (2024-25)

- Downstream EBIT swing: ~$1.1B QoQ in 2025

- Raises short-term earnings and stock unpredictability

20 percent slower transition pace than European peers

BP has cut oil output 20% slower than European peer TotalEnergies in 2025, keeping production near 1.9 million barrels/day to protect 2025 EBITDA of about $25 billion, prompting accusations of strategic drift from investors focused on transition speed.

That pragmatic pivot saw ESG-focused funds trim holdings-BP's shares held by sustainability funds fell ~6% in 2025-raising concern it may lose market share in low‑carbon markets where competitors accelerate renewables capacity additions.

- 20% slower cut vs TotalEnergies (2025)

- ~1.9m bbl/day production (2025)

- 2025 EBITDA ≈ $25bn

- ESG-fund holdings down ~6% (2025)

BP 2025: High debt, low renewable returns, volatile refining, steady production

BP's 2025 net debt $22.0B and interest expense ~$1.3B shrink flexibility; renewable IRRs ~4% vs upstream EBITDA $16.2B; Deepwater Horizon cash outflows ~$1.2B/yr; refining margin volatility ~±15% caused downstream EBIT swings ~$1.1B QoQ; production ~1.9m bpd with slower cuts-ESG fund holdings -6% (2025).

| Metric | 2025 |

|---|---|

| Net debt | $22.0B |

| Net interest expense | $1.3B |

| Upstream adj. EBITDA | $16.2B |

| Renewable IRR | ~4% |

| Deepwater Horizon cash | $1.2B/yr |

| Refining margin vol. | ±15% |

| Downstream EBIT swing | $1.1B QoQ |

| Production | ~1.9m bpd |

| ESG holdings change | -6% |

Preview the Actual Deliverable

British Petroleum SWOT Analysis

This is the actual SWOT analysis document you'll receive upon purchase-no surprises, just professional quality; the preview below is taken directly from the full report and the complete, editable version is unlocked after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Insightful Decisions Backed by Expert Research

BP's strengths-scale, integrated assets, and low-carbon investments-are balanced by volatile oil prices, regulatory scrutiny, and transition risks; its growth hinges on execution of renewables and cost discipline. Want the full story behind BP's strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

Strengths

$26 billion in annual operating cash flow

BP generated about $26 billion in annual operating cash flow in FY2025, driven by upstream margins that funded $8.5 billion in dividends and $5.2 billion in share buybacks while allocating $2.1 billion to low‑carbon investments.

300,000 barrels per day production in the Gulf of Mexico

British Petroleum's 300,000 bpd deepwater Gulf of Mexico output anchors a high-margin oil book, with lifting costs around $12-15/boe and break-even near $40-50/borel in 2025, so profitability holds if Brent falls to $60; established pipelines and hubs cut downtime and offset declines in mature U.S. onshore fields, giving stable cash flow and EBITDA resilience.

42,000 global electric vehicle charging points

BP Pulse operates ~42,000 global EV charging points (FY2025), scaling fast across Europe and the US and making BP a leading EV mobility player.

Integrating chargers with 18,200 BP retail sites (FY2025) lifts non-fuel revenue per site; forecourt retail boosts margin from waiting drivers.

Their oil-site footprint creates a physical moat-hard for app-first chains to match on location density and captive demand.

$4 billion annual share buyback commitment

BP's $4 billion 2025 buyback commitment shows management discipline in returning excess capital, supporting the share price during sector volatility; buybacks plus a 4.5% dividend yield (2025 est.) helped total shareholder return outperform peers in 2024-25.

This steady return policy signals confidence in BP's long-term cash generation from its integrated model-2025 operating cash flow guidance of ~$25 billion underpins the program and shifts focus to value over volume.

The buyback reassures institutional investors demanding capital rigor after BP repurchased ~$12 billion since 2022 and maintained net debt/EBITDA around 1.0x in 2025.

- 2025 buyback: $4.0B

- Dividend yield (2025 est.): ~4.5%

- 2025 operating cash flow guidance: ~$25B

- Net debt/EBITDA (2025): ~1.0x

- Repurchases since 2022: ~$12B

10 gigawatts of installed renewable capacity pipeline

BP has progressed from planning to execution on a 10 GW offshore wind and solar pipeline, shifting revenue mix toward renewables and supporting its target to increase low-carbon investment to $6-8 billion annually by 2025.

This scale positions BP to win large government tenders and corporate power purchase agreements (PPAs), with project-level EBITDA potential measured in hundreds of millions per GW.

Using multi-technology (offshore wind, solar) lowers output risk from any single resource and smooths generation profiles, aiding grid contracts and corporate buyers.

- 10 GW pipeline across offshore wind and solar as of FY2025

- $6-8bn annual low‑carbon spend target for 2025

- Competitive for large tenders and multi-year PPAs

- Multi-tech reduces single-source underperformance risk

BP's $25B cash engine: buybacks, 4.5% yield, 300k bpd GOM & 10GW renewables

BP's integrated cash engine: FY2025 operating cash flow ~$25-26B, $4.0B buyback, ~4.5% dividend yield, net debt/EBITDA ~1.0x; 300k bpd deepwater GOM at $12-15/boe lifting cost; BP Pulse ~42k chargers; 10 GW renewables pipeline, $6-8B annual low‑carbon spend target.

| Metric | 2025 |

|---|---|

| Op. cash flow | ~$25-26B |

| Buyback | $4.0B |

| Dividend yield | ~4.5% |

| Net debt/EBITDA | ~1.0x |

| GOM output | ~300k bpd |

| BP Pulse | ~42k chargers |

| Renewables pipeline | 10 GW |

| Low‑carbon spend | $6-8B |

What is included in the product

Provides a concise SWOT analysis of British Petroleum, outlining its core strengths, operational weaknesses, strategic opportunities in energy transition, and external threats from market volatility and regulatory pressures.

Provides a concise BP SWOT snapshot for rapid strategic alignment, highlighting energy transition strengths and hydrocarbon risks for quick executive decisions.

Weaknesses

$22 billion net debt position

BP's 2025 net debt stood at $22.0 billion, higher than several Tier 1 peers, which narrows its room to maneuver in sharp oil-price drops and operational shocks.

With global interest rates up, annual net interest expense rose to about $1.3 billion in 2025, diverting cash from green investments.

Investors price this leverage into valuation: BP traded at a 15-20% EV/EBITDA discount versus less-leveraged majors in 2025.

4 percent average returns on renewable projects

BP faces a weakness in earning roughly 4% average returns on renewable projects versus 10-15% (or higher) returns from oil and gas; in 2025 BP reported renewable IRRs ~4% and upstream margins that delivered $16.2 billion in adjusted EBITDA in 2025, highlighting the steep gap.

$1.2 billion annual Deepwater Horizon legal payments

BP still pays about $1.2 billion annually related to Deepwater Horizon settlements, draining free cash flow in FY2025 and acting as a persistent litigation tax rivals like Shell and ExxonMobil avoid.

15 percent refining margin volatility

The downstream segment is highly sensitive to global crack spreads; BP reported refining margin volatility around ±15% in FY2025, driven by redirected trade flows and ~2.4 mbpd of new Middle East capacity added in 2024-25.

Such swings can cause quarterly earnings misses despite steady upstream output-BP's downstream EBIT changed by $1.1 billion QoQ in 2025 on margin moves.

Dependence on refining profits makes BP's quarterly results more unpredictable for short-term investors, increasing earnings variance and stock volatility.

- ~15% refining margin volatility in FY2025

- ~2.4 mbpd new Middle East refining capacity (2024-25)

- Downstream EBIT swing: ~$1.1B QoQ in 2025

- Raises short-term earnings and stock unpredictability

20 percent slower transition pace than European peers

BP has cut oil output 20% slower than European peer TotalEnergies in 2025, keeping production near 1.9 million barrels/day to protect 2025 EBITDA of about $25 billion, prompting accusations of strategic drift from investors focused on transition speed.

That pragmatic pivot saw ESG-focused funds trim holdings-BP's shares held by sustainability funds fell ~6% in 2025-raising concern it may lose market share in low‑carbon markets where competitors accelerate renewables capacity additions.

- 20% slower cut vs TotalEnergies (2025)

- ~1.9m bbl/day production (2025)

- 2025 EBITDA ≈ $25bn

- ESG-fund holdings down ~6% (2025)

BP 2025: High debt, low renewable returns, volatile refining, steady production

BP's 2025 net debt $22.0B and interest expense ~$1.3B shrink flexibility; renewable IRRs ~4% vs upstream EBITDA $16.2B; Deepwater Horizon cash outflows ~$1.2B/yr; refining margin volatility ~±15% caused downstream EBIT swings ~$1.1B QoQ; production ~1.9m bpd with slower cuts-ESG fund holdings -6% (2025).

| Metric | 2025 |

|---|---|

| Net debt | $22.0B |

| Net interest expense | $1.3B |

| Upstream adj. EBITDA | $16.2B |

| Renewable IRR | ~4% |

| Deepwater Horizon cash | $1.2B/yr |

| Refining margin vol. | ±15% |

| Downstream EBIT swing | $1.1B QoQ |

| Production | ~1.9m bpd |

| ESG holdings change | -6% |

Preview the Actual Deliverable

British Petroleum SWOT Analysis

This is the actual SWOT analysis document you'll receive upon purchase-no surprises, just professional quality; the preview below is taken directly from the full report and the complete, editable version is unlocked after checkout.