BUILDSTOCK PORTER'S FIVE FORCES TEMPLATE RESEARCH

What is included in the product

Analyzes competitive forces, customer influence, and market entry risks for Buildstock.

Swap in your own data, labels, and notes to reflect current business conditions.

Same Document Delivered

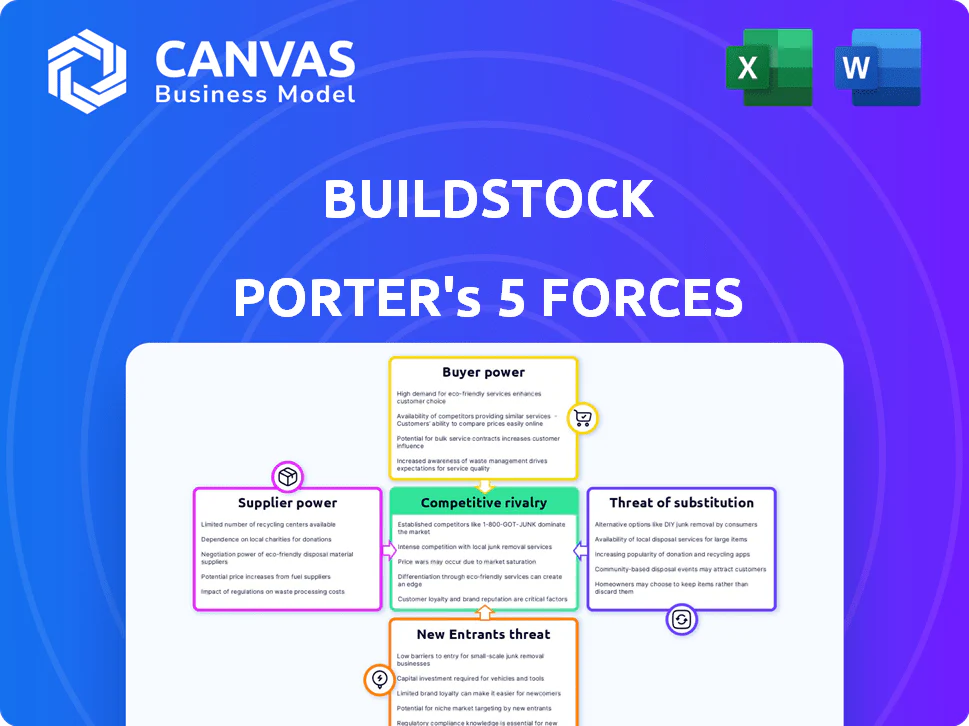

Buildstock Porter's Five Forces Analysis

This preview showcases the complete Buildstock Porter's Five Forces analysis document. You are viewing the exact, fully formatted report you will receive. There are no differences between what you see now and what you'll download instantly. This is the ready-to-use version, prepared professionally. The analysis is immediately available after purchase.

Porter's Five Forces Analysis Template

Don't Miss the Bigger Picture

Buildstock operates within a dynamic construction market, influenced by key forces. Buyer power, particularly from large developers, impacts pricing. Supplier bargaining power, especially for materials, poses another challenge. New entrants face high capital costs and regulatory hurdles. Substitute threats, like prefabricated construction, exist. Finally, competitive rivalry is intense.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Buildstock’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Suppliers

The bargaining power of suppliers is crucial. Fewer suppliers of specialized materials mean more control over pricing. Buildstock's reliance on high-rise and industrial sectors could mean fewer, more powerful suppliers. In 2024, construction material costs, like steel, surged due to supply chain issues. This increased supplier influence.

Switching Costs for Buyers

If switching material suppliers is hard for construction firms, suppliers gain power. This is common due to existing partnerships, specific material needs, or logistical hurdles. For instance, in 2024, material price volatility saw some firms locked into specific suppliers. This reliance increased supplier leverage in negotiations. The construction sector's material costs rose approximately 5% in 2024, indicating supplier power.

Unique or Differentiated Materials

Suppliers of unique materials like specialized insulation or custom-designed windows have strong bargaining power. In 2024, companies offering eco-friendly concrete saw a 15% price increase due to high demand and limited supply. This differentiation allows them to charge premium prices. The construction industry's reliance on these unique components gives suppliers leverage.

Threat of Forward Integration

The threat of forward integration significantly boosts suppliers' leverage. If suppliers can directly supply materials, they gain more control. This bypasses platforms like Buildstock, boosting their bargaining power. In 2024, the building materials market hit $1.5 trillion globally. This trend is driven by suppliers' direct-to-builder strategies.

- Direct supply reduces reliance on intermediaries.

- Suppliers gain pricing control and market access.

- Forward integration increases profitability.

- Construction companies face higher costs.

Importance of Supplier's Input

The bargaining power of suppliers is crucial in construction. If suppliers offer unique, essential materials, their influence grows. This can affect project costs and timelines. For example, steel prices surged in 2024 due to supply chain issues.

- Increased material costs in 2024 impacted construction projects, especially those reliant on specific suppliers.

- Steel prices rose by 15% in Q2 2024, affecting project budgets.

- Supplier concentration, like in specialized concrete, gives more power.

- Diversifying suppliers can reduce dependency and bargaining power.

Supplier Dynamics: Pricing and Market Control

Suppliers hold significant power, especially with unique materials or limited options. Steel prices rose 15% in Q2 2024, impacting project budgets. Forward integration by suppliers further boosts their leverage, as seen in the $1.5T global building materials market.

| Factor | Impact | 2024 Data |

|---|---|---|

| Material Uniqueness | Higher Prices | Eco-concrete up 15% |

| Supplier Concentration | Increased Power | Steel Price Spike: +15% |

| Forward Integration | Direct Market Access | $1.5T Building Materials |

Customers Bargaining Power

Concentration of Customers

In Buildstock's high-rise and industrial construction, customers like developers often wield considerable power. A few large customers can significantly impact pricing and terms, potentially squeezing profit margins. For instance, in 2024, the top 10 construction firms accounted for nearly 40% of the total market revenue, highlighting customer concentration. This concentration allows for greater negotiation leverage.

Volume of Purchases

Customers purchasing construction materials in bulk wield significant bargaining power. Buildstock's platform supports large-volume orders, amplifying this dynamic. For instance, in 2024, bulk buyers of lumber could negotiate up to a 10% discount. This influences pricing strategies and profitability.

Availability of Alternatives

If Buildstock's customers can easily find construction materials elsewhere, their bargaining power strengthens. For instance, in 2024, the market share of online construction material sales grew by 15%, indicating more options. This includes platforms like Amazon Business and specialized online retailers, increasing customer choice. The more choices, the more leverage customers have to negotiate prices and terms.

Customer Price Sensitivity

In the competitive construction industry, customers are frequently very price-sensitive. Buildstock's capacity to provide cost savings significantly affects customer power. For example, in 2024, construction material costs saw fluctuations, with lumber prices changing up to 15% in certain regions, and these changes directly impact project costs. This sensitivity means customers can easily switch to competitors offering lower prices.

- Price Comparison: Customers actively compare bids from different construction companies.

- Cost of Materials: The price of materials greatly influences the final project cost, affecting customer choices.

- Project Budget: Customers usually have defined budgets, making them very price-conscious.

- Switching Costs: Low switching costs allow customers to opt for more affordable options.

Low Customer Switching Costs

In the construction industry, low switching costs give customers significant bargaining power. If construction companies can easily and cheaply switch between platforms or suppliers, they have more leverage. This means they can negotiate better prices and terms. According to a 2024 report, the average cost to switch suppliers is about 2-5% of project costs, depending on the complexity.

- Switching costs affect pricing.

- Negotiating power increases.

- Supplier competition intensifies.

- Profit margins are pressured.

Buildstock's 2024: Customer Power Plays

In 2024, Buildstock's customers, especially developers, held strong bargaining power. Large customers influenced pricing, squeezing margins, as the top 10 firms held nearly 40% market share. Bulk buyers secured discounts; lumber buyers got up to 10% off. Easy access to options, like online sales that grew by 15%, amplified customer leverage.

| Factor | Impact | 2024 Data |

|---|---|---|

| Customer Concentration | Negotiating Leverage | Top 10 firms: 40% market share |

| Bulk Purchases | Price Discounts | Lumber discounts: up to 10% |

| Market Alternatives | Increased Choice | Online sales growth: 15% |

Rivalry Among Competitors

Number and Intensity of Competitors

The construction materials market and FinTech for construction are seeing new entrants. A high number of rivals, from startups to giants, suggests intense competition. For example, in 2024, the construction tech sector saw over $10B in funding globally. This influx fuels rivalry, with companies vying for market share and innovation dominance. Expect this competition to drive down prices and spur rapid advancements.

Industry Growth Rate

The construction industry's growth influences competitive rivalry. If growth slows, firms fight harder for market share. The U.S. construction sector saw a 6.1% YoY increase in spending in December 2024. Slower growth can intensify price wars and marketing battles. This can erode profitability, as seen with a 3.7% decline in construction material prices in Q4 2024.

Product Differentiation

Buildstock's unique marketplace and FinTech features, like AI product discovery, set it apart. This product differentiation can lessen rivalry. For example, in 2024, companies with strong tech saw higher profit margins. Buildstock's faster supplier payments also add to its competitive edge. This strategic focus can make Buildstock less susceptible to intense competition.

Exit Barriers

High exit barriers intensify competition, especially in sectors like construction tech or materials. Companies might persist in the market even with poor profits due to significant investments in specialized equipment or long-term contracts. This can result in price wars and decreased profitability for all involved. For example, in 2024, the construction industry saw a 5% decrease in profit margins because of intense competition and high operational costs.

- High fixed costs: significant investments in machinery or specialized technology.

- Long-term contracts: commitments that are difficult to terminate.

- Specialized assets: assets that are not easily sold or repurposed.

- Emotional attachment: founders or key personnel may be reluctant to exit.

Brand Identity and Loyalty

In B2B markets, brand identity and loyalty significantly shape competitive rivalry. Buildstock's efforts to transform relationship-based models face hurdles from established brands. Strong supplier and buyer brand recognition affects market dynamics. Consider that in 2024, 68% of B2B buyers prioritized brand reputation. This highlights the importance of brand perception in competitive landscapes.

- B2B buyers prioritize brand reputation (68% in 2024).

- Established relationships influence market dynamics.

- Buildstock challenges traditional models.

- Brand strength impacts competitive intensity.

Buildstock's Competitive Landscape: Navigating the Market

Competitive rivalry in Buildstock's sector is high, fueled by new entrants and technological advancements. Increased competition, like the over $10B in 2024 funding for construction tech, drives price wars. Slowing growth, as seen with a 3.7% decline in Q4 2024 construction material prices, intensifies this rivalry, impacting profitability. Buildstock's differentiation, such as AI product discovery, offers some competitive advantage.

| Factor | Impact | Data (2024) |

|---|---|---|

| Market Growth | Influences rivalry intensity | U.S. construction spending: +6.1% YoY |

| Price Wars | Erode profitability | Construction material prices: -3.7% (Q4) |

| Brand Reputation | Affects market dynamics | B2B buyers prioritizing brand: 68% |

Original: $10.00

-65%$10.00

$3.50BUILDSTOCK PORTER'S FIVE FORCES TEMPLATE RESEARCH

What is included in the product

Analyzes competitive forces, customer influence, and market entry risks for Buildstock.

Swap in your own data, labels, and notes to reflect current business conditions.

Same Document Delivered

Buildstock Porter's Five Forces Analysis

This preview showcases the complete Buildstock Porter's Five Forces analysis document. You are viewing the exact, fully formatted report you will receive. There are no differences between what you see now and what you'll download instantly. This is the ready-to-use version, prepared professionally. The analysis is immediately available after purchase.

Porter's Five Forces Analysis Template

Don't Miss the Bigger Picture

Buildstock operates within a dynamic construction market, influenced by key forces. Buyer power, particularly from large developers, impacts pricing. Supplier bargaining power, especially for materials, poses another challenge. New entrants face high capital costs and regulatory hurdles. Substitute threats, like prefabricated construction, exist. Finally, competitive rivalry is intense.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Buildstock’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Suppliers

The bargaining power of suppliers is crucial. Fewer suppliers of specialized materials mean more control over pricing. Buildstock's reliance on high-rise and industrial sectors could mean fewer, more powerful suppliers. In 2024, construction material costs, like steel, surged due to supply chain issues. This increased supplier influence.

Switching Costs for Buyers

If switching material suppliers is hard for construction firms, suppliers gain power. This is common due to existing partnerships, specific material needs, or logistical hurdles. For instance, in 2024, material price volatility saw some firms locked into specific suppliers. This reliance increased supplier leverage in negotiations. The construction sector's material costs rose approximately 5% in 2024, indicating supplier power.

Unique or Differentiated Materials

Suppliers of unique materials like specialized insulation or custom-designed windows have strong bargaining power. In 2024, companies offering eco-friendly concrete saw a 15% price increase due to high demand and limited supply. This differentiation allows them to charge premium prices. The construction industry's reliance on these unique components gives suppliers leverage.

Threat of Forward Integration

The threat of forward integration significantly boosts suppliers' leverage. If suppliers can directly supply materials, they gain more control. This bypasses platforms like Buildstock, boosting their bargaining power. In 2024, the building materials market hit $1.5 trillion globally. This trend is driven by suppliers' direct-to-builder strategies.

- Direct supply reduces reliance on intermediaries.

- Suppliers gain pricing control and market access.

- Forward integration increases profitability.

- Construction companies face higher costs.

Importance of Supplier's Input

The bargaining power of suppliers is crucial in construction. If suppliers offer unique, essential materials, their influence grows. This can affect project costs and timelines. For example, steel prices surged in 2024 due to supply chain issues.

- Increased material costs in 2024 impacted construction projects, especially those reliant on specific suppliers.

- Steel prices rose by 15% in Q2 2024, affecting project budgets.

- Supplier concentration, like in specialized concrete, gives more power.

- Diversifying suppliers can reduce dependency and bargaining power.

Supplier Dynamics: Pricing and Market Control

Suppliers hold significant power, especially with unique materials or limited options. Steel prices rose 15% in Q2 2024, impacting project budgets. Forward integration by suppliers further boosts their leverage, as seen in the $1.5T global building materials market.

| Factor | Impact | 2024 Data |

|---|---|---|

| Material Uniqueness | Higher Prices | Eco-concrete up 15% |

| Supplier Concentration | Increased Power | Steel Price Spike: +15% |

| Forward Integration | Direct Market Access | $1.5T Building Materials |

Customers Bargaining Power

Concentration of Customers

In Buildstock's high-rise and industrial construction, customers like developers often wield considerable power. A few large customers can significantly impact pricing and terms, potentially squeezing profit margins. For instance, in 2024, the top 10 construction firms accounted for nearly 40% of the total market revenue, highlighting customer concentration. This concentration allows for greater negotiation leverage.

Volume of Purchases

Customers purchasing construction materials in bulk wield significant bargaining power. Buildstock's platform supports large-volume orders, amplifying this dynamic. For instance, in 2024, bulk buyers of lumber could negotiate up to a 10% discount. This influences pricing strategies and profitability.

Availability of Alternatives

If Buildstock's customers can easily find construction materials elsewhere, their bargaining power strengthens. For instance, in 2024, the market share of online construction material sales grew by 15%, indicating more options. This includes platforms like Amazon Business and specialized online retailers, increasing customer choice. The more choices, the more leverage customers have to negotiate prices and terms.

Customer Price Sensitivity

In the competitive construction industry, customers are frequently very price-sensitive. Buildstock's capacity to provide cost savings significantly affects customer power. For example, in 2024, construction material costs saw fluctuations, with lumber prices changing up to 15% in certain regions, and these changes directly impact project costs. This sensitivity means customers can easily switch to competitors offering lower prices.

- Price Comparison: Customers actively compare bids from different construction companies.

- Cost of Materials: The price of materials greatly influences the final project cost, affecting customer choices.

- Project Budget: Customers usually have defined budgets, making them very price-conscious.

- Switching Costs: Low switching costs allow customers to opt for more affordable options.

Low Customer Switching Costs

In the construction industry, low switching costs give customers significant bargaining power. If construction companies can easily and cheaply switch between platforms or suppliers, they have more leverage. This means they can negotiate better prices and terms. According to a 2024 report, the average cost to switch suppliers is about 2-5% of project costs, depending on the complexity.

- Switching costs affect pricing.

- Negotiating power increases.

- Supplier competition intensifies.

- Profit margins are pressured.

Buildstock's 2024: Customer Power Plays

In 2024, Buildstock's customers, especially developers, held strong bargaining power. Large customers influenced pricing, squeezing margins, as the top 10 firms held nearly 40% market share. Bulk buyers secured discounts; lumber buyers got up to 10% off. Easy access to options, like online sales that grew by 15%, amplified customer leverage.

| Factor | Impact | 2024 Data |

|---|---|---|

| Customer Concentration | Negotiating Leverage | Top 10 firms: 40% market share |

| Bulk Purchases | Price Discounts | Lumber discounts: up to 10% |

| Market Alternatives | Increased Choice | Online sales growth: 15% |

Rivalry Among Competitors

Number and Intensity of Competitors

The construction materials market and FinTech for construction are seeing new entrants. A high number of rivals, from startups to giants, suggests intense competition. For example, in 2024, the construction tech sector saw over $10B in funding globally. This influx fuels rivalry, with companies vying for market share and innovation dominance. Expect this competition to drive down prices and spur rapid advancements.

Industry Growth Rate

The construction industry's growth influences competitive rivalry. If growth slows, firms fight harder for market share. The U.S. construction sector saw a 6.1% YoY increase in spending in December 2024. Slower growth can intensify price wars and marketing battles. This can erode profitability, as seen with a 3.7% decline in construction material prices in Q4 2024.

Product Differentiation

Buildstock's unique marketplace and FinTech features, like AI product discovery, set it apart. This product differentiation can lessen rivalry. For example, in 2024, companies with strong tech saw higher profit margins. Buildstock's faster supplier payments also add to its competitive edge. This strategic focus can make Buildstock less susceptible to intense competition.

Exit Barriers

High exit barriers intensify competition, especially in sectors like construction tech or materials. Companies might persist in the market even with poor profits due to significant investments in specialized equipment or long-term contracts. This can result in price wars and decreased profitability for all involved. For example, in 2024, the construction industry saw a 5% decrease in profit margins because of intense competition and high operational costs.

- High fixed costs: significant investments in machinery or specialized technology.

- Long-term contracts: commitments that are difficult to terminate.

- Specialized assets: assets that are not easily sold or repurposed.

- Emotional attachment: founders or key personnel may be reluctant to exit.

Brand Identity and Loyalty

In B2B markets, brand identity and loyalty significantly shape competitive rivalry. Buildstock's efforts to transform relationship-based models face hurdles from established brands. Strong supplier and buyer brand recognition affects market dynamics. Consider that in 2024, 68% of B2B buyers prioritized brand reputation. This highlights the importance of brand perception in competitive landscapes.

- B2B buyers prioritize brand reputation (68% in 2024).

- Established relationships influence market dynamics.

- Buildstock challenges traditional models.

- Brand strength impacts competitive intensity.

Buildstock's Competitive Landscape: Navigating the Market

Competitive rivalry in Buildstock's sector is high, fueled by new entrants and technological advancements. Increased competition, like the over $10B in 2024 funding for construction tech, drives price wars. Slowing growth, as seen with a 3.7% decline in Q4 2024 construction material prices, intensifies this rivalry, impacting profitability. Buildstock's differentiation, such as AI product discovery, offers some competitive advantage.

| Factor | Impact | Data (2024) |

|---|---|---|

| Market Growth | Influences rivalry intensity | U.S. construction spending: +6.1% YoY |

| Price Wars | Erode profitability | Construction material prices: -3.7% (Q4) |

| Brand Reputation | Affects market dynamics | B2B buyers prioritizing brand: 68% |

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

What is included in the product

Analyzes competitive forces, customer influence, and market entry risks for Buildstock.

Swap in your own data, labels, and notes to reflect current business conditions.

Same Document Delivered

Buildstock Porter's Five Forces Analysis

This preview showcases the complete Buildstock Porter's Five Forces analysis document. You are viewing the exact, fully formatted report you will receive. There are no differences between what you see now and what you'll download instantly. This is the ready-to-use version, prepared professionally. The analysis is immediately available after purchase.

Porter's Five Forces Analysis Template

Don't Miss the Bigger Picture

Buildstock operates within a dynamic construction market, influenced by key forces. Buyer power, particularly from large developers, impacts pricing. Supplier bargaining power, especially for materials, poses another challenge. New entrants face high capital costs and regulatory hurdles. Substitute threats, like prefabricated construction, exist. Finally, competitive rivalry is intense.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Buildstock’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Suppliers

The bargaining power of suppliers is crucial. Fewer suppliers of specialized materials mean more control over pricing. Buildstock's reliance on high-rise and industrial sectors could mean fewer, more powerful suppliers. In 2024, construction material costs, like steel, surged due to supply chain issues. This increased supplier influence.

Switching Costs for Buyers

If switching material suppliers is hard for construction firms, suppliers gain power. This is common due to existing partnerships, specific material needs, or logistical hurdles. For instance, in 2024, material price volatility saw some firms locked into specific suppliers. This reliance increased supplier leverage in negotiations. The construction sector's material costs rose approximately 5% in 2024, indicating supplier power.

Unique or Differentiated Materials

Suppliers of unique materials like specialized insulation or custom-designed windows have strong bargaining power. In 2024, companies offering eco-friendly concrete saw a 15% price increase due to high demand and limited supply. This differentiation allows them to charge premium prices. The construction industry's reliance on these unique components gives suppliers leverage.

Threat of Forward Integration

The threat of forward integration significantly boosts suppliers' leverage. If suppliers can directly supply materials, they gain more control. This bypasses platforms like Buildstock, boosting their bargaining power. In 2024, the building materials market hit $1.5 trillion globally. This trend is driven by suppliers' direct-to-builder strategies.

- Direct supply reduces reliance on intermediaries.

- Suppliers gain pricing control and market access.

- Forward integration increases profitability.

- Construction companies face higher costs.

Importance of Supplier's Input

The bargaining power of suppliers is crucial in construction. If suppliers offer unique, essential materials, their influence grows. This can affect project costs and timelines. For example, steel prices surged in 2024 due to supply chain issues.

- Increased material costs in 2024 impacted construction projects, especially those reliant on specific suppliers.

- Steel prices rose by 15% in Q2 2024, affecting project budgets.

- Supplier concentration, like in specialized concrete, gives more power.

- Diversifying suppliers can reduce dependency and bargaining power.

Supplier Dynamics: Pricing and Market Control

Suppliers hold significant power, especially with unique materials or limited options. Steel prices rose 15% in Q2 2024, impacting project budgets. Forward integration by suppliers further boosts their leverage, as seen in the $1.5T global building materials market.

| Factor | Impact | 2024 Data |

|---|---|---|

| Material Uniqueness | Higher Prices | Eco-concrete up 15% |

| Supplier Concentration | Increased Power | Steel Price Spike: +15% |

| Forward Integration | Direct Market Access | $1.5T Building Materials |

Customers Bargaining Power

Concentration of Customers

In Buildstock's high-rise and industrial construction, customers like developers often wield considerable power. A few large customers can significantly impact pricing and terms, potentially squeezing profit margins. For instance, in 2024, the top 10 construction firms accounted for nearly 40% of the total market revenue, highlighting customer concentration. This concentration allows for greater negotiation leverage.

Volume of Purchases

Customers purchasing construction materials in bulk wield significant bargaining power. Buildstock's platform supports large-volume orders, amplifying this dynamic. For instance, in 2024, bulk buyers of lumber could negotiate up to a 10% discount. This influences pricing strategies and profitability.

Availability of Alternatives

If Buildstock's customers can easily find construction materials elsewhere, their bargaining power strengthens. For instance, in 2024, the market share of online construction material sales grew by 15%, indicating more options. This includes platforms like Amazon Business and specialized online retailers, increasing customer choice. The more choices, the more leverage customers have to negotiate prices and terms.

Customer Price Sensitivity

In the competitive construction industry, customers are frequently very price-sensitive. Buildstock's capacity to provide cost savings significantly affects customer power. For example, in 2024, construction material costs saw fluctuations, with lumber prices changing up to 15% in certain regions, and these changes directly impact project costs. This sensitivity means customers can easily switch to competitors offering lower prices.

- Price Comparison: Customers actively compare bids from different construction companies.

- Cost of Materials: The price of materials greatly influences the final project cost, affecting customer choices.

- Project Budget: Customers usually have defined budgets, making them very price-conscious.

- Switching Costs: Low switching costs allow customers to opt for more affordable options.

Low Customer Switching Costs

In the construction industry, low switching costs give customers significant bargaining power. If construction companies can easily and cheaply switch between platforms or suppliers, they have more leverage. This means they can negotiate better prices and terms. According to a 2024 report, the average cost to switch suppliers is about 2-5% of project costs, depending on the complexity.

- Switching costs affect pricing.

- Negotiating power increases.

- Supplier competition intensifies.

- Profit margins are pressured.

Buildstock's 2024: Customer Power Plays

In 2024, Buildstock's customers, especially developers, held strong bargaining power. Large customers influenced pricing, squeezing margins, as the top 10 firms held nearly 40% market share. Bulk buyers secured discounts; lumber buyers got up to 10% off. Easy access to options, like online sales that grew by 15%, amplified customer leverage.

| Factor | Impact | 2024 Data |

|---|---|---|

| Customer Concentration | Negotiating Leverage | Top 10 firms: 40% market share |

| Bulk Purchases | Price Discounts | Lumber discounts: up to 10% |

| Market Alternatives | Increased Choice | Online sales growth: 15% |

Rivalry Among Competitors

Number and Intensity of Competitors

The construction materials market and FinTech for construction are seeing new entrants. A high number of rivals, from startups to giants, suggests intense competition. For example, in 2024, the construction tech sector saw over $10B in funding globally. This influx fuels rivalry, with companies vying for market share and innovation dominance. Expect this competition to drive down prices and spur rapid advancements.

Industry Growth Rate

The construction industry's growth influences competitive rivalry. If growth slows, firms fight harder for market share. The U.S. construction sector saw a 6.1% YoY increase in spending in December 2024. Slower growth can intensify price wars and marketing battles. This can erode profitability, as seen with a 3.7% decline in construction material prices in Q4 2024.

Product Differentiation

Buildstock's unique marketplace and FinTech features, like AI product discovery, set it apart. This product differentiation can lessen rivalry. For example, in 2024, companies with strong tech saw higher profit margins. Buildstock's faster supplier payments also add to its competitive edge. This strategic focus can make Buildstock less susceptible to intense competition.

Exit Barriers

High exit barriers intensify competition, especially in sectors like construction tech or materials. Companies might persist in the market even with poor profits due to significant investments in specialized equipment or long-term contracts. This can result in price wars and decreased profitability for all involved. For example, in 2024, the construction industry saw a 5% decrease in profit margins because of intense competition and high operational costs.

- High fixed costs: significant investments in machinery or specialized technology.

- Long-term contracts: commitments that are difficult to terminate.

- Specialized assets: assets that are not easily sold or repurposed.

- Emotional attachment: founders or key personnel may be reluctant to exit.

Brand Identity and Loyalty

In B2B markets, brand identity and loyalty significantly shape competitive rivalry. Buildstock's efforts to transform relationship-based models face hurdles from established brands. Strong supplier and buyer brand recognition affects market dynamics. Consider that in 2024, 68% of B2B buyers prioritized brand reputation. This highlights the importance of brand perception in competitive landscapes.

- B2B buyers prioritize brand reputation (68% in 2024).

- Established relationships influence market dynamics.

- Buildstock challenges traditional models.

- Brand strength impacts competitive intensity.

Buildstock's Competitive Landscape: Navigating the Market

Competitive rivalry in Buildstock's sector is high, fueled by new entrants and technological advancements. Increased competition, like the over $10B in 2024 funding for construction tech, drives price wars. Slowing growth, as seen with a 3.7% decline in Q4 2024 construction material prices, intensifies this rivalry, impacting profitability. Buildstock's differentiation, such as AI product discovery, offers some competitive advantage.

| Factor | Impact | Data (2024) |

|---|---|---|

| Market Growth | Influences rivalry intensity | U.S. construction spending: +6.1% YoY |

| Price Wars | Erode profitability | Construction material prices: -3.7% (Q4) |

| Brand Reputation | Affects market dynamics | B2B buyers prioritizing brand: 68% |