CARBONCAPTURE PORTER'S FIVE FORCES TEMPLATE RESEARCH

What is included in the product

Evaluates control held by suppliers and buyers, and their influence on pricing and profitability.

Easily identify pressure points to unlock competitive advantages.

Full Version Awaits

CarbonCapture Porter's Five Forces Analysis

This preview showcases the complete Carbon Capture Porter's Five Forces analysis. You will receive this identical, professionally formatted document immediately after your purchase.

Porter's Five Forces Analysis Template

From Overview to Strategy Blueprint

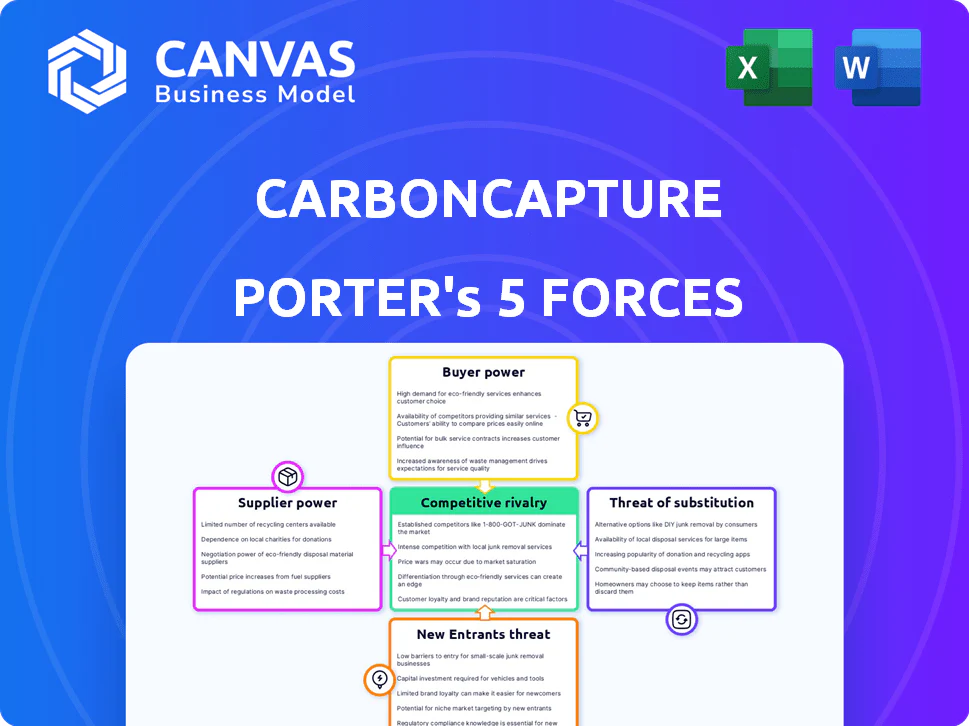

CarbonCapture's competitive landscape is evolving rapidly. Supplier power is moderate, given specialized equipment needs. Buyer power is currently low, but could increase with government incentives. The threat of new entrants is significant, fueled by growing interest in carbon capture. Substitute products pose a moderate threat, particularly in sectors with established decarbonization technologies. Finally, the intensity of rivalry is increasing as more companies enter the space.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore CarbonCapture’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Limited Number of Specialized Material Suppliers

The direct air capture sector depends on specific materials such as high-tech filters and absorbents. Currently, there is a shortage of suppliers for these essential parts, potentially increasing their bargaining power. For instance, the cost of specialized absorbents can fluctuate considerably. In 2024, the price of certain advanced filter materials rose by about 15% due to limited supply. This situation allows suppliers to influence pricing and terms with companies like CarbonCapture.

High Switching Costs for CarbonCapture

Carbon capture projects often face high switching costs for key components, making them dependent on current suppliers. Changing suppliers can be expensive, involving investments in new materials and integration efforts. For example, the cost to retrofit a carbon capture system can range from $50 million to $200 million. This dependence gives suppliers significant bargaining power, especially for specialized equipment. This is important to consider in 2024 as the market grows.

Suppliers Holding Unique Patents or Technologies

Some suppliers, owning exclusive patents or tech, can significantly boost their bargaining power in the carbon capture market. This is especially true for firms supplying specialized equipment or crucial materials. For instance, in 2024, companies with proprietary amine-based solvents, essential for many carbon capture processes, could command higher prices and terms. This dependency limits CarbonCapture's choices, impacting project costs.

Dependency on Energy Sources

CarbonCapture's dependency on energy sources significantly impacts its operations. The energy-intensive nature of Direct Air Capture (DAC) machines places the company at the mercy of energy suppliers. Securing low-cost, renewable energy is crucial to both maximize carbon removal efficiency and minimize operational expenses, impacting profitability.

- Energy costs can represent up to 60% of operational expenses for DAC facilities.

- In 2024, the average cost of renewable energy varied significantly: Solar at $0.03/kWh, Wind at $0.04/kWh, and Geothermal at $0.05/kWh.

- CarbonCapture needs to negotiate favorable energy contracts to stay competitive.

- The bargaining power of energy suppliers directly affects CarbonCapture's cost structure and overall financial viability.

Availability of CO2 Transportation and Storage Infrastructure

The bargaining power of suppliers is affected by the availability of CO2 transportation and storage infrastructure, which is critical for CarbonCapture operations. Limited access to suitable storage sites or transportation networks increases the power of companies providing these services. This can lead to higher costs and operational challenges. In 2024, the global CO2 storage capacity is estimated at around 8.5 billion tonnes.

- High concentration of CO2 transport and storage providers can create supplier power.

- Lack of infrastructure increases operational costs for CarbonCapture.

- Strategic partnerships are essential to mitigate supplier power.

- Government incentives can influence infrastructure development.

Carbon Capture: Costs & Supplier Dynamics

Suppliers of specialized materials and components for carbon capture, like advanced filters, hold significant bargaining power due to limited supply and high switching costs. In 2024, prices for crucial filter materials rose by approximately 15%. Exclusive patents and technology further enhance supplier influence, especially for essential components like amine-based solvents. CarbonCapture's profitability depends on negotiating favorable energy contracts, as energy costs can constitute up to 60% of operational expenses.

| Factor | Impact on CarbonCapture | 2024 Data |

|---|---|---|

| Material Scarcity | Higher costs, supply chain risks | Filter material price increase: ~15% |

| Switching Costs | Dependency on existing suppliers | Retrofit cost range: $50M-$200M |

| Energy Costs | Operational expense, profitability | Renewable energy cost: $0.03-$0.05/kWh |

Customers Bargaining Power

Government and Corporate Net-Zero Commitments Driving Demand

Government and corporate net-zero pledges significantly boost customer bargaining power in carbon capture. For example, in 2024, over 70% of Fortune 500 companies had net-zero targets. This creates strong demand for carbon removal. Consequently, customers can negotiate better terms.

Availability of Government Funding and Incentives

Government funding and incentives, like tax credits and grants, heavily impact customer decisions in carbon capture. These incentives, particularly for DAC projects, boost customer bargaining power by improving project financial viability. For instance, the U.S. Inflation Reduction Act offers substantial tax credits, potentially covering up to $180 per metric ton of captured CO2. This reduces costs and enhances customer leverage. In 2024, these incentives continue to drive project adoption.

Customers' Need for Verifiable Carbon Removal Credits

Customers, especially those in voluntary carbon markets, demand verifiable, high-quality carbon removal credits. CarbonCapture, offering these, gains stronger bargaining power, as demand for verifiable credits surged. In 2024, the voluntary carbon market saw transactions valued at approximately $2 billion. Customers' need for specific attributes also boosts their influence, shaping market dynamics.

Potential for Customers to Develop In-House Solutions

Some large corporations, particularly those with substantial financial resources, might consider developing their own carbon capture solutions. This strategic move could diminish their dependence on external providers like CarbonCapture. Such an option grants these potential customers a degree of leverage in negotiations. For example, in 2024, companies like ExxonMobil allocated billions to carbon capture projects, reflecting this trend.

- ExxonMobil's investment in carbon capture in 2024 reached several billion dollars.

- This investment strategy directly impacts the bargaining power of CarbonCapture.

- Companies with internal R&D capabilities can negotiate better terms.

- The threat of self-supply reduces the pricing power of external providers.

Price Sensitivity and Cost of DAC

The substantial expenses linked to Direct Air Capture (DAC) make clients particularly sensitive to pricing. As DAC innovations advance, possibly reducing costs, clients' leverage in pricing negotiations might rise. According to the IEA, the cost of DAC ranges from $600-$1,000+ per ton of CO2 removed in 2024, highlighting the financial burden.

- Cost Sensitivity: Customers are highly sensitive to the high costs of current DAC technologies.

- Price Negotiation: Potential for increased bargaining power as technology costs decrease.

- Financial Burden: High capital and operational expenditures influence purchasing decisions.

- Cost Range: The IEA estimates DAC costs between $600-$1,000+ per ton of CO2 in 2024.

Carbon Capture: Customer Power Surge

Customer bargaining power in carbon capture is amplified by net-zero commitments; over 70% of Fortune 500 had such targets in 2024. Government incentives, like the U.S. Inflation Reduction Act offering up to $180/ton tax credits, further enhance customer leverage. The voluntary carbon market's $2 billion transactions in 2024 highlight demand for verifiable credits, shaping customer influence.

| Factor | Impact | Data (2024) |

|---|---|---|

| Net-Zero Pledges | Increases bargaining power | 70%+ Fortune 500 with targets |

| Govt. Incentives | Enhances customer leverage | Up to $180/ton tax credit (US IRA) |

| Voluntary Market | Shapes customer influence | $2B in transactions |

Rivalry Among Competitors

Presence of Multiple DAC Technology Developers

The Direct Air Capture (DAC) market is becoming more competitive due to the rise of multiple technology developers. Companies like Climeworks and Carbon Engineering are competing, increasing rivalry. This leads to innovation but also potential price wars as firms seek market share. For example, in 2024, over $1 billion was invested in DAC projects globally.

Varying Stages of Technology Development and Deployment

Competitive rivalry in carbon capture is complex due to varying tech stages. Some firms operate pilot plants, while others manage commercial facilities. This leads to competition based on scalability and efficiency. For example, in 2024, the global carbon capture market was valued at $3.5 billion, showing the stakes. Cost-effectiveness is another key factor, shaping strategic decisions.

Entry of Large Industrial Players and Startups

The carbon capture market sees heightened competition from established industrial giants and new startups. This blend of players with diverse strengths intensifies the rivalry. For example, in 2024, several major companies like ExxonMobil and Chevron significantly increased their investments in carbon capture projects, adding to the competitive pressure. Startups, such as Climeworks, also raise substantial funding rounds, further reshaping the market dynamics.

Competition from Other Carbon Capture and Storage (CCS) Methods

Direct Air Capture (DAC) faces competition from established Carbon Capture and Storage (CCS) methods, particularly point-source capture. The CCS market is diverse, encompassing various technologies and significant existing players. This competition influences the adoption and economic viability of DAC projects. The global CCS market was valued at $2.98 billion in 2023 and is projected to reach $10.43 billion by 2030.

- Point-source capture is a more mature technology.

- The CCS market includes companies like ExxonMobil and Shell.

- CCS projects often involve lower initial capital costs.

- DAC faces challenges related to energy consumption and scalability.

Focus on Strategic Partnerships and Funding

Competitive rivalry in carbon capture is intensifying, with companies aggressively pursuing strategic partnerships and substantial funding. Securing investments and forming alliances is crucial for accelerating development and deployment in this emerging industry. For example, in 2024, several carbon capture projects secured over $100 million in funding through government grants and private investments. This financial backing is vital for scaling operations and gaining a competitive edge. The competition drives innovation and efficiency improvements, shaping the future of carbon capture technologies.

- Strategic partnerships are essential for sharing expertise and resources.

- Funding rounds frequently exceed $50 million, indicating strong investor interest.

- Competition is pushing companies to develop more cost-effective solutions.

- Government incentives play a significant role in attracting investments.

Carbon Capture: A Billion-Dollar Battleground

Competitive rivalry in the carbon capture sector is fierce, fueled by escalating investments and strategic partnerships. Companies are vying for market share, leading to innovation and cost-cutting. In 2024, over $1.5 billion was invested in carbon capture projects, reflecting the high stakes.

| Key Factor | Description | Impact |

|---|---|---|

| Investment | Significant capital influx from public and private sources. | Accelerates technology development and deployment. |

| Partnerships | Strategic alliances for technology and market access. | Enhances competitiveness and market reach. |

| Innovation | Focus on improving efficiency and reducing costs. | Drives down costs and increases adoption rates. |

Original: $10.00

-65%$10.00

$3.50CARBONCAPTURE PORTER'S FIVE FORCES TEMPLATE RESEARCH

What is included in the product

Evaluates control held by suppliers and buyers, and their influence on pricing and profitability.

Easily identify pressure points to unlock competitive advantages.

Full Version Awaits

CarbonCapture Porter's Five Forces Analysis

This preview showcases the complete Carbon Capture Porter's Five Forces analysis. You will receive this identical, professionally formatted document immediately after your purchase.

Porter's Five Forces Analysis Template

From Overview to Strategy Blueprint

CarbonCapture's competitive landscape is evolving rapidly. Supplier power is moderate, given specialized equipment needs. Buyer power is currently low, but could increase with government incentives. The threat of new entrants is significant, fueled by growing interest in carbon capture. Substitute products pose a moderate threat, particularly in sectors with established decarbonization technologies. Finally, the intensity of rivalry is increasing as more companies enter the space.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore CarbonCapture’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Limited Number of Specialized Material Suppliers

The direct air capture sector depends on specific materials such as high-tech filters and absorbents. Currently, there is a shortage of suppliers for these essential parts, potentially increasing their bargaining power. For instance, the cost of specialized absorbents can fluctuate considerably. In 2024, the price of certain advanced filter materials rose by about 15% due to limited supply. This situation allows suppliers to influence pricing and terms with companies like CarbonCapture.

High Switching Costs for CarbonCapture

Carbon capture projects often face high switching costs for key components, making them dependent on current suppliers. Changing suppliers can be expensive, involving investments in new materials and integration efforts. For example, the cost to retrofit a carbon capture system can range from $50 million to $200 million. This dependence gives suppliers significant bargaining power, especially for specialized equipment. This is important to consider in 2024 as the market grows.

Suppliers Holding Unique Patents or Technologies

Some suppliers, owning exclusive patents or tech, can significantly boost their bargaining power in the carbon capture market. This is especially true for firms supplying specialized equipment or crucial materials. For instance, in 2024, companies with proprietary amine-based solvents, essential for many carbon capture processes, could command higher prices and terms. This dependency limits CarbonCapture's choices, impacting project costs.

Dependency on Energy Sources

CarbonCapture's dependency on energy sources significantly impacts its operations. The energy-intensive nature of Direct Air Capture (DAC) machines places the company at the mercy of energy suppliers. Securing low-cost, renewable energy is crucial to both maximize carbon removal efficiency and minimize operational expenses, impacting profitability.

- Energy costs can represent up to 60% of operational expenses for DAC facilities.

- In 2024, the average cost of renewable energy varied significantly: Solar at $0.03/kWh, Wind at $0.04/kWh, and Geothermal at $0.05/kWh.

- CarbonCapture needs to negotiate favorable energy contracts to stay competitive.

- The bargaining power of energy suppliers directly affects CarbonCapture's cost structure and overall financial viability.

Availability of CO2 Transportation and Storage Infrastructure

The bargaining power of suppliers is affected by the availability of CO2 transportation and storage infrastructure, which is critical for CarbonCapture operations. Limited access to suitable storage sites or transportation networks increases the power of companies providing these services. This can lead to higher costs and operational challenges. In 2024, the global CO2 storage capacity is estimated at around 8.5 billion tonnes.

- High concentration of CO2 transport and storage providers can create supplier power.

- Lack of infrastructure increases operational costs for CarbonCapture.

- Strategic partnerships are essential to mitigate supplier power.

- Government incentives can influence infrastructure development.

Carbon Capture: Costs & Supplier Dynamics

Suppliers of specialized materials and components for carbon capture, like advanced filters, hold significant bargaining power due to limited supply and high switching costs. In 2024, prices for crucial filter materials rose by approximately 15%. Exclusive patents and technology further enhance supplier influence, especially for essential components like amine-based solvents. CarbonCapture's profitability depends on negotiating favorable energy contracts, as energy costs can constitute up to 60% of operational expenses.

| Factor | Impact on CarbonCapture | 2024 Data |

|---|---|---|

| Material Scarcity | Higher costs, supply chain risks | Filter material price increase: ~15% |

| Switching Costs | Dependency on existing suppliers | Retrofit cost range: $50M-$200M |

| Energy Costs | Operational expense, profitability | Renewable energy cost: $0.03-$0.05/kWh |

Customers Bargaining Power

Government and Corporate Net-Zero Commitments Driving Demand

Government and corporate net-zero pledges significantly boost customer bargaining power in carbon capture. For example, in 2024, over 70% of Fortune 500 companies had net-zero targets. This creates strong demand for carbon removal. Consequently, customers can negotiate better terms.

Availability of Government Funding and Incentives

Government funding and incentives, like tax credits and grants, heavily impact customer decisions in carbon capture. These incentives, particularly for DAC projects, boost customer bargaining power by improving project financial viability. For instance, the U.S. Inflation Reduction Act offers substantial tax credits, potentially covering up to $180 per metric ton of captured CO2. This reduces costs and enhances customer leverage. In 2024, these incentives continue to drive project adoption.

Customers' Need for Verifiable Carbon Removal Credits

Customers, especially those in voluntary carbon markets, demand verifiable, high-quality carbon removal credits. CarbonCapture, offering these, gains stronger bargaining power, as demand for verifiable credits surged. In 2024, the voluntary carbon market saw transactions valued at approximately $2 billion. Customers' need for specific attributes also boosts their influence, shaping market dynamics.

Potential for Customers to Develop In-House Solutions

Some large corporations, particularly those with substantial financial resources, might consider developing their own carbon capture solutions. This strategic move could diminish their dependence on external providers like CarbonCapture. Such an option grants these potential customers a degree of leverage in negotiations. For example, in 2024, companies like ExxonMobil allocated billions to carbon capture projects, reflecting this trend.

- ExxonMobil's investment in carbon capture in 2024 reached several billion dollars.

- This investment strategy directly impacts the bargaining power of CarbonCapture.

- Companies with internal R&D capabilities can negotiate better terms.

- The threat of self-supply reduces the pricing power of external providers.

Price Sensitivity and Cost of DAC

The substantial expenses linked to Direct Air Capture (DAC) make clients particularly sensitive to pricing. As DAC innovations advance, possibly reducing costs, clients' leverage in pricing negotiations might rise. According to the IEA, the cost of DAC ranges from $600-$1,000+ per ton of CO2 removed in 2024, highlighting the financial burden.

- Cost Sensitivity: Customers are highly sensitive to the high costs of current DAC technologies.

- Price Negotiation: Potential for increased bargaining power as technology costs decrease.

- Financial Burden: High capital and operational expenditures influence purchasing decisions.

- Cost Range: The IEA estimates DAC costs between $600-$1,000+ per ton of CO2 in 2024.

Carbon Capture: Customer Power Surge

Customer bargaining power in carbon capture is amplified by net-zero commitments; over 70% of Fortune 500 had such targets in 2024. Government incentives, like the U.S. Inflation Reduction Act offering up to $180/ton tax credits, further enhance customer leverage. The voluntary carbon market's $2 billion transactions in 2024 highlight demand for verifiable credits, shaping customer influence.

| Factor | Impact | Data (2024) |

|---|---|---|

| Net-Zero Pledges | Increases bargaining power | 70%+ Fortune 500 with targets |

| Govt. Incentives | Enhances customer leverage | Up to $180/ton tax credit (US IRA) |

| Voluntary Market | Shapes customer influence | $2B in transactions |

Rivalry Among Competitors

Presence of Multiple DAC Technology Developers

The Direct Air Capture (DAC) market is becoming more competitive due to the rise of multiple technology developers. Companies like Climeworks and Carbon Engineering are competing, increasing rivalry. This leads to innovation but also potential price wars as firms seek market share. For example, in 2024, over $1 billion was invested in DAC projects globally.

Varying Stages of Technology Development and Deployment

Competitive rivalry in carbon capture is complex due to varying tech stages. Some firms operate pilot plants, while others manage commercial facilities. This leads to competition based on scalability and efficiency. For example, in 2024, the global carbon capture market was valued at $3.5 billion, showing the stakes. Cost-effectiveness is another key factor, shaping strategic decisions.

Entry of Large Industrial Players and Startups

The carbon capture market sees heightened competition from established industrial giants and new startups. This blend of players with diverse strengths intensifies the rivalry. For example, in 2024, several major companies like ExxonMobil and Chevron significantly increased their investments in carbon capture projects, adding to the competitive pressure. Startups, such as Climeworks, also raise substantial funding rounds, further reshaping the market dynamics.

Competition from Other Carbon Capture and Storage (CCS) Methods

Direct Air Capture (DAC) faces competition from established Carbon Capture and Storage (CCS) methods, particularly point-source capture. The CCS market is diverse, encompassing various technologies and significant existing players. This competition influences the adoption and economic viability of DAC projects. The global CCS market was valued at $2.98 billion in 2023 and is projected to reach $10.43 billion by 2030.

- Point-source capture is a more mature technology.

- The CCS market includes companies like ExxonMobil and Shell.

- CCS projects often involve lower initial capital costs.

- DAC faces challenges related to energy consumption and scalability.

Focus on Strategic Partnerships and Funding

Competitive rivalry in carbon capture is intensifying, with companies aggressively pursuing strategic partnerships and substantial funding. Securing investments and forming alliances is crucial for accelerating development and deployment in this emerging industry. For example, in 2024, several carbon capture projects secured over $100 million in funding through government grants and private investments. This financial backing is vital for scaling operations and gaining a competitive edge. The competition drives innovation and efficiency improvements, shaping the future of carbon capture technologies.

- Strategic partnerships are essential for sharing expertise and resources.

- Funding rounds frequently exceed $50 million, indicating strong investor interest.

- Competition is pushing companies to develop more cost-effective solutions.

- Government incentives play a significant role in attracting investments.

Carbon Capture: A Billion-Dollar Battleground

Competitive rivalry in the carbon capture sector is fierce, fueled by escalating investments and strategic partnerships. Companies are vying for market share, leading to innovation and cost-cutting. In 2024, over $1.5 billion was invested in carbon capture projects, reflecting the high stakes.

| Key Factor | Description | Impact |

|---|---|---|

| Investment | Significant capital influx from public and private sources. | Accelerates technology development and deployment. |

| Partnerships | Strategic alliances for technology and market access. | Enhances competitiveness and market reach. |

| Innovation | Focus on improving efficiency and reducing costs. | Drives down costs and increases adoption rates. |

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

What is included in the product

Evaluates control held by suppliers and buyers, and their influence on pricing and profitability.

Easily identify pressure points to unlock competitive advantages.

Full Version Awaits

CarbonCapture Porter's Five Forces Analysis

This preview showcases the complete Carbon Capture Porter's Five Forces analysis. You will receive this identical, professionally formatted document immediately after your purchase.

Porter's Five Forces Analysis Template

From Overview to Strategy Blueprint

CarbonCapture's competitive landscape is evolving rapidly. Supplier power is moderate, given specialized equipment needs. Buyer power is currently low, but could increase with government incentives. The threat of new entrants is significant, fueled by growing interest in carbon capture. Substitute products pose a moderate threat, particularly in sectors with established decarbonization technologies. Finally, the intensity of rivalry is increasing as more companies enter the space.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore CarbonCapture’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Limited Number of Specialized Material Suppliers

The direct air capture sector depends on specific materials such as high-tech filters and absorbents. Currently, there is a shortage of suppliers for these essential parts, potentially increasing their bargaining power. For instance, the cost of specialized absorbents can fluctuate considerably. In 2024, the price of certain advanced filter materials rose by about 15% due to limited supply. This situation allows suppliers to influence pricing and terms with companies like CarbonCapture.

High Switching Costs for CarbonCapture

Carbon capture projects often face high switching costs for key components, making them dependent on current suppliers. Changing suppliers can be expensive, involving investments in new materials and integration efforts. For example, the cost to retrofit a carbon capture system can range from $50 million to $200 million. This dependence gives suppliers significant bargaining power, especially for specialized equipment. This is important to consider in 2024 as the market grows.

Suppliers Holding Unique Patents or Technologies

Some suppliers, owning exclusive patents or tech, can significantly boost their bargaining power in the carbon capture market. This is especially true for firms supplying specialized equipment or crucial materials. For instance, in 2024, companies with proprietary amine-based solvents, essential for many carbon capture processes, could command higher prices and terms. This dependency limits CarbonCapture's choices, impacting project costs.

Dependency on Energy Sources

CarbonCapture's dependency on energy sources significantly impacts its operations. The energy-intensive nature of Direct Air Capture (DAC) machines places the company at the mercy of energy suppliers. Securing low-cost, renewable energy is crucial to both maximize carbon removal efficiency and minimize operational expenses, impacting profitability.

- Energy costs can represent up to 60% of operational expenses for DAC facilities.

- In 2024, the average cost of renewable energy varied significantly: Solar at $0.03/kWh, Wind at $0.04/kWh, and Geothermal at $0.05/kWh.

- CarbonCapture needs to negotiate favorable energy contracts to stay competitive.

- The bargaining power of energy suppliers directly affects CarbonCapture's cost structure and overall financial viability.

Availability of CO2 Transportation and Storage Infrastructure

The bargaining power of suppliers is affected by the availability of CO2 transportation and storage infrastructure, which is critical for CarbonCapture operations. Limited access to suitable storage sites or transportation networks increases the power of companies providing these services. This can lead to higher costs and operational challenges. In 2024, the global CO2 storage capacity is estimated at around 8.5 billion tonnes.

- High concentration of CO2 transport and storage providers can create supplier power.

- Lack of infrastructure increases operational costs for CarbonCapture.

- Strategic partnerships are essential to mitigate supplier power.

- Government incentives can influence infrastructure development.

Carbon Capture: Costs & Supplier Dynamics

Suppliers of specialized materials and components for carbon capture, like advanced filters, hold significant bargaining power due to limited supply and high switching costs. In 2024, prices for crucial filter materials rose by approximately 15%. Exclusive patents and technology further enhance supplier influence, especially for essential components like amine-based solvents. CarbonCapture's profitability depends on negotiating favorable energy contracts, as energy costs can constitute up to 60% of operational expenses.

| Factor | Impact on CarbonCapture | 2024 Data |

|---|---|---|

| Material Scarcity | Higher costs, supply chain risks | Filter material price increase: ~15% |

| Switching Costs | Dependency on existing suppliers | Retrofit cost range: $50M-$200M |

| Energy Costs | Operational expense, profitability | Renewable energy cost: $0.03-$0.05/kWh |

Customers Bargaining Power

Government and Corporate Net-Zero Commitments Driving Demand

Government and corporate net-zero pledges significantly boost customer bargaining power in carbon capture. For example, in 2024, over 70% of Fortune 500 companies had net-zero targets. This creates strong demand for carbon removal. Consequently, customers can negotiate better terms.

Availability of Government Funding and Incentives

Government funding and incentives, like tax credits and grants, heavily impact customer decisions in carbon capture. These incentives, particularly for DAC projects, boost customer bargaining power by improving project financial viability. For instance, the U.S. Inflation Reduction Act offers substantial tax credits, potentially covering up to $180 per metric ton of captured CO2. This reduces costs and enhances customer leverage. In 2024, these incentives continue to drive project adoption.

Customers' Need for Verifiable Carbon Removal Credits

Customers, especially those in voluntary carbon markets, demand verifiable, high-quality carbon removal credits. CarbonCapture, offering these, gains stronger bargaining power, as demand for verifiable credits surged. In 2024, the voluntary carbon market saw transactions valued at approximately $2 billion. Customers' need for specific attributes also boosts their influence, shaping market dynamics.

Potential for Customers to Develop In-House Solutions

Some large corporations, particularly those with substantial financial resources, might consider developing their own carbon capture solutions. This strategic move could diminish their dependence on external providers like CarbonCapture. Such an option grants these potential customers a degree of leverage in negotiations. For example, in 2024, companies like ExxonMobil allocated billions to carbon capture projects, reflecting this trend.

- ExxonMobil's investment in carbon capture in 2024 reached several billion dollars.

- This investment strategy directly impacts the bargaining power of CarbonCapture.

- Companies with internal R&D capabilities can negotiate better terms.

- The threat of self-supply reduces the pricing power of external providers.

Price Sensitivity and Cost of DAC

The substantial expenses linked to Direct Air Capture (DAC) make clients particularly sensitive to pricing. As DAC innovations advance, possibly reducing costs, clients' leverage in pricing negotiations might rise. According to the IEA, the cost of DAC ranges from $600-$1,000+ per ton of CO2 removed in 2024, highlighting the financial burden.

- Cost Sensitivity: Customers are highly sensitive to the high costs of current DAC technologies.

- Price Negotiation: Potential for increased bargaining power as technology costs decrease.

- Financial Burden: High capital and operational expenditures influence purchasing decisions.

- Cost Range: The IEA estimates DAC costs between $600-$1,000+ per ton of CO2 in 2024.

Carbon Capture: Customer Power Surge

Customer bargaining power in carbon capture is amplified by net-zero commitments; over 70% of Fortune 500 had such targets in 2024. Government incentives, like the U.S. Inflation Reduction Act offering up to $180/ton tax credits, further enhance customer leverage. The voluntary carbon market's $2 billion transactions in 2024 highlight demand for verifiable credits, shaping customer influence.

| Factor | Impact | Data (2024) |

|---|---|---|

| Net-Zero Pledges | Increases bargaining power | 70%+ Fortune 500 with targets |

| Govt. Incentives | Enhances customer leverage | Up to $180/ton tax credit (US IRA) |

| Voluntary Market | Shapes customer influence | $2B in transactions |

Rivalry Among Competitors

Presence of Multiple DAC Technology Developers

The Direct Air Capture (DAC) market is becoming more competitive due to the rise of multiple technology developers. Companies like Climeworks and Carbon Engineering are competing, increasing rivalry. This leads to innovation but also potential price wars as firms seek market share. For example, in 2024, over $1 billion was invested in DAC projects globally.

Varying Stages of Technology Development and Deployment

Competitive rivalry in carbon capture is complex due to varying tech stages. Some firms operate pilot plants, while others manage commercial facilities. This leads to competition based on scalability and efficiency. For example, in 2024, the global carbon capture market was valued at $3.5 billion, showing the stakes. Cost-effectiveness is another key factor, shaping strategic decisions.

Entry of Large Industrial Players and Startups

The carbon capture market sees heightened competition from established industrial giants and new startups. This blend of players with diverse strengths intensifies the rivalry. For example, in 2024, several major companies like ExxonMobil and Chevron significantly increased their investments in carbon capture projects, adding to the competitive pressure. Startups, such as Climeworks, also raise substantial funding rounds, further reshaping the market dynamics.

Competition from Other Carbon Capture and Storage (CCS) Methods

Direct Air Capture (DAC) faces competition from established Carbon Capture and Storage (CCS) methods, particularly point-source capture. The CCS market is diverse, encompassing various technologies and significant existing players. This competition influences the adoption and economic viability of DAC projects. The global CCS market was valued at $2.98 billion in 2023 and is projected to reach $10.43 billion by 2030.

- Point-source capture is a more mature technology.

- The CCS market includes companies like ExxonMobil and Shell.

- CCS projects often involve lower initial capital costs.

- DAC faces challenges related to energy consumption and scalability.

Focus on Strategic Partnerships and Funding

Competitive rivalry in carbon capture is intensifying, with companies aggressively pursuing strategic partnerships and substantial funding. Securing investments and forming alliances is crucial for accelerating development and deployment in this emerging industry. For example, in 2024, several carbon capture projects secured over $100 million in funding through government grants and private investments. This financial backing is vital for scaling operations and gaining a competitive edge. The competition drives innovation and efficiency improvements, shaping the future of carbon capture technologies.

- Strategic partnerships are essential for sharing expertise and resources.

- Funding rounds frequently exceed $50 million, indicating strong investor interest.

- Competition is pushing companies to develop more cost-effective solutions.

- Government incentives play a significant role in attracting investments.

Carbon Capture: A Billion-Dollar Battleground

Competitive rivalry in the carbon capture sector is fierce, fueled by escalating investments and strategic partnerships. Companies are vying for market share, leading to innovation and cost-cutting. In 2024, over $1.5 billion was invested in carbon capture projects, reflecting the high stakes.

| Key Factor | Description | Impact |

|---|---|---|

| Investment | Significant capital influx from public and private sources. | Accelerates technology development and deployment. |

| Partnerships | Strategic alliances for technology and market access. | Enhances competitiveness and market reach. |

| Innovation | Focus on improving efficiency and reducing costs. | Drives down costs and increases adoption rates. |