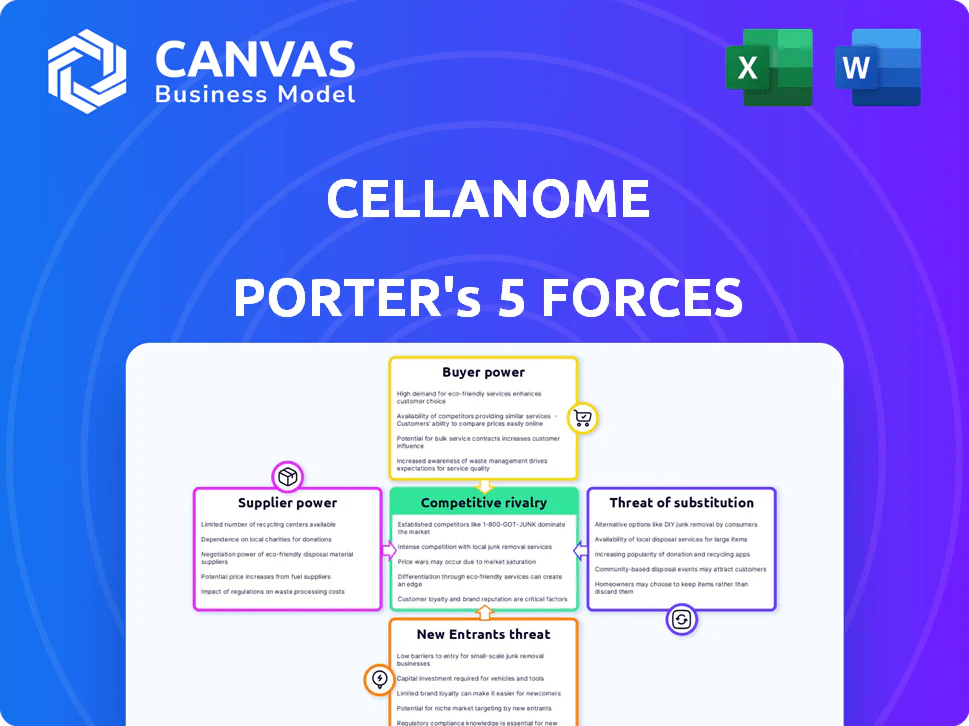

CELLANOME PORTER'S FIVE FORCES TEMPLATE RESEARCH

A Must-Have Tool for Decision-Makers

Cellanome faces moderate supplier leverage and high buyer scrutiny as it scales niche cell-based therapies; regulatory hurdles and capital intensity raise entry barriers while scientific substitutes and larger incumbents pose ongoing threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cellanome's competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependency on Specialized Sequencing Hardware

Cellanome depends on three dominant suppliers for high-throughput sequencers and proprietary flow cells, giving them pricing power; in 2025 these vendors control ~85% of market share for instruments used in single-cell workflows.

Their hardware sets data formats and throughput caps, so a 10-20% price hike or a 6-12 week supply delay in 2025 would raise Cellanome's per-sample costs by an estimated 8-14%.

Scarcity of Specialized Multi-Omics Talent

The market for PhD-level multi-omics scientists remained tight in 2026; across biotech hiring surveys, demand outpaced supply by ~2.5x and median offers rose 18% year-over-year versus 2025, with top packages hitting $250-350k total comp in 2025-giving these specialists strong supplier bargaining power.

Cloud Infrastructure and Compute Costs

Processing Cellanome's multi-omics datasets needs vast cloud compute; AWS and Google Cloud together held ~64% of global market in 2025 and charge $0.10-$3.50 per vCPU-hour for high‑performance instances, making supplier pricing power strong.

Access to Proprietary Biological Databases

Cellanome's model accuracy hinges on access to curated biological datasets-many held by academic consortiums or private biobanks charging licensing fees; in 2025 top biobank access fees range from $50k-$500k+ annually, and restricted access or fee hikes would erode Cellanome's disease-mechanism differentiation and raise model training costs.

- High dependency: >60% of training value from third-party datasets

- Cost risk: typical 2025 licensing $50k-$500k+ per dataset

- Supply risk: access restrictions reduce model novelty and speed-to-insight

Concentration of Reagent Manufacturers

Cellanome depends on a few specialized reagent makers-top three suppliers control ~65% of the niche synthetic-biology reagent market (2025), so supplier price moves directly hit COGS and EBITDA.

Vertical integration remains costly and slow in 2026, keeping Cellanome exposed to supplier-driven price hikes and supply shocks, risking sudden margin compression of 200-400 bps.

- Top-3 suppliers: ~65% market share (2025)

- Supplier-driven margin risk: 200-400 bps (2026)

- Diversification limited by technical spec and lead times

Cellanome at Risk: Supplier Concentration Could Squeeze Margins 200-400 bps in 2025

Cellanome faces strong supplier power in 2025: top sequencer vendors hold ~85% instrument share, cloud (AWS+GCP) ~64% share, reagent top‑3 ~65%, PhD talent demand ~2.5x supply, dataset licensing $50k-$500k+, and supplier shocks could compress margins 200-400 bps.

| Supplier | 2025 Metric | Impact |

|---|---|---|

| Sequencers | ~85% market share | Pricing power |

| Cloud | ~64% market share | Compute cost $0.10-$3.50/vCPU‑hr |

| Reagents | Top‑3 ~65% | COGS sensitivity |

| Datasets | $50k-$500k+/yr | Training cost, access risk |

| Talent | Demand 2.5x supply | Comp $250-$350k |

What is included in the product

Tailored Porter's Five Forces for Cellanome: evaluates competitive rivalry, supplier and buyer power, threats from substitutes and new entrants, and highlights disruptive technologies and regulatory risks shaping pricing, margins, and strategic positioning.

Compact Porter's Five Forces snapshot to pinpoint competitive pain points quickly-ready to drop into decks and guide immediate strategic moves.

Customers Bargaining Power

Consolidation of Big Pharma Partners

The primary buyers for Cellanome's platform are Big Pharma; following 2023-2025 consolidation, the top 10 pharma firms now account for ~55% of global R&D spend (~$180B of $330B in 2025), concentrating purchasing power and enabling tougher pricing, tighter milestones, and shorter pilot windows before long-term deals.

Demand for Validated Clinical Outcomes

Buyers now demand validated clinical outcomes; by 2026 payors and pharma customers tie 38% of multi-omics deals to trial-success milestones, so Cellanome must show clear trial efficacy to win contracts.

Customers push performance-based pricing-industry data show 22% of preclinical partnerships shifted to milestone payments in 2025-shifting discovery risk onto Cellanome.

This buyer power compresses margins: if Cellanome accepts typical contingency caps (30-50% of contract value at risk), revenue volatility rises and upfront cash needs jump.

Alternative In-House Platform Development

Larger biotechs are spending more on in-house multi-omics: Deloitte reports 42% of top 50 pharma increased bioinformatics capex in 2024, so build-vs-buy cuts Cellanome's bargaining power as customers can replicate basic pipelines.

When clients can build, Cellanome must prove unique value; in 2025 Cellanome should cite IP-protected algorithms, peer-reviewed benchmarks showing >25% higher cell-type resolution, and faster turnarounds to retain pricing power.

Price Sensitivity in Academic and Non-Profit Sectors

Academic researchers give Cellanome prestige and citations but face a 3.5% real-terms cut in US federal R&D budgets from 2024-2025, raising price sensitivity and driving shopping for lower-cost sequencing and analysis.

Cellanome must accept lower margins-academic segment prices often 20-40% below commercial rates-while using selective discounted collaborations to sustain visibility.

- US federal R&D down 3.5% (2024-2025)

- Academic prices 20-40% below commercial

- High prestige, low-margin trade-off

- Frequent price-shopping among labs

Switching Costs and Data Portability

As multi-omics standards converge, switching costs fall: a 2025 survey shows 42% of genomics buyers piloting 2+ platforms, reducing vendor lock-in for Cellanome and raising churn risk.

Cellanome must therefore offset easier switching by delivering superior service, faster time-to-insight, and exclusive biomarkers to retain customers.

- 42% of buyers pilot multiple platforms (2025 survey)

- Vendor churn up to 15% higher when portability exists

- Retention relies on unique insights and premium support

Top10 Pharma Drives Milestone Pricing, Cuts Prices & Sparks 15% Vendor Churn

Buyers concentrated (Top10 pharma ≈55% R&D spend = $180B of $330B in 2025) force milestone pricing; 38% of deals tied to trial outcomes (2026), 22% preclinical shifted to milestones (2025), 42% buyers pilot 2+ platforms (2025) - lowering prices and raising churn; academic segment prices -20-40% vs commercial; vendor churn +15% with portability.

| Metric | Value |

|---|---|

| Top10 pharma R&D share (2025) | 55% ($180B) |

| Deals tied to outcomes (2026) | 38% |

| Preclinical milestone shift (2025) | 22% |

| Buyers piloting 2+ platforms (2025) | 42% |

| Academic vs commercial price | -20-40% |

| Churn uplift with portability | +15% |

Preview the Actual Deliverable

Cellanome Porter's Five Forces Analysis

This preview shows the exact Cellanome Porter's Five Forces analysis you'll receive immediately after purchase-fully formatted, professionally written, and ready for download with no placeholders or samples.

Original: $10.00

-65%$10.00

$3.50CELLANOME PORTER'S FIVE FORCES TEMPLATE RESEARCH

A Must-Have Tool for Decision-Makers

Cellanome faces moderate supplier leverage and high buyer scrutiny as it scales niche cell-based therapies; regulatory hurdles and capital intensity raise entry barriers while scientific substitutes and larger incumbents pose ongoing threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cellanome's competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependency on Specialized Sequencing Hardware

Cellanome depends on three dominant suppliers for high-throughput sequencers and proprietary flow cells, giving them pricing power; in 2025 these vendors control ~85% of market share for instruments used in single-cell workflows.

Their hardware sets data formats and throughput caps, so a 10-20% price hike or a 6-12 week supply delay in 2025 would raise Cellanome's per-sample costs by an estimated 8-14%.

Scarcity of Specialized Multi-Omics Talent

The market for PhD-level multi-omics scientists remained tight in 2026; across biotech hiring surveys, demand outpaced supply by ~2.5x and median offers rose 18% year-over-year versus 2025, with top packages hitting $250-350k total comp in 2025-giving these specialists strong supplier bargaining power.

Cloud Infrastructure and Compute Costs

Processing Cellanome's multi-omics datasets needs vast cloud compute; AWS and Google Cloud together held ~64% of global market in 2025 and charge $0.10-$3.50 per vCPU-hour for high‑performance instances, making supplier pricing power strong.

Access to Proprietary Biological Databases

Cellanome's model accuracy hinges on access to curated biological datasets-many held by academic consortiums or private biobanks charging licensing fees; in 2025 top biobank access fees range from $50k-$500k+ annually, and restricted access or fee hikes would erode Cellanome's disease-mechanism differentiation and raise model training costs.

- High dependency: >60% of training value from third-party datasets

- Cost risk: typical 2025 licensing $50k-$500k+ per dataset

- Supply risk: access restrictions reduce model novelty and speed-to-insight

Concentration of Reagent Manufacturers

Cellanome depends on a few specialized reagent makers-top three suppliers control ~65% of the niche synthetic-biology reagent market (2025), so supplier price moves directly hit COGS and EBITDA.

Vertical integration remains costly and slow in 2026, keeping Cellanome exposed to supplier-driven price hikes and supply shocks, risking sudden margin compression of 200-400 bps.

- Top-3 suppliers: ~65% market share (2025)

- Supplier-driven margin risk: 200-400 bps (2026)

- Diversification limited by technical spec and lead times

Cellanome at Risk: Supplier Concentration Could Squeeze Margins 200-400 bps in 2025

Cellanome faces strong supplier power in 2025: top sequencer vendors hold ~85% instrument share, cloud (AWS+GCP) ~64% share, reagent top‑3 ~65%, PhD talent demand ~2.5x supply, dataset licensing $50k-$500k+, and supplier shocks could compress margins 200-400 bps.

| Supplier | 2025 Metric | Impact |

|---|---|---|

| Sequencers | ~85% market share | Pricing power |

| Cloud | ~64% market share | Compute cost $0.10-$3.50/vCPU‑hr |

| Reagents | Top‑3 ~65% | COGS sensitivity |

| Datasets | $50k-$500k+/yr | Training cost, access risk |

| Talent | Demand 2.5x supply | Comp $250-$350k |

What is included in the product

Tailored Porter's Five Forces for Cellanome: evaluates competitive rivalry, supplier and buyer power, threats from substitutes and new entrants, and highlights disruptive technologies and regulatory risks shaping pricing, margins, and strategic positioning.

Compact Porter's Five Forces snapshot to pinpoint competitive pain points quickly-ready to drop into decks and guide immediate strategic moves.

Customers Bargaining Power

Consolidation of Big Pharma Partners

The primary buyers for Cellanome's platform are Big Pharma; following 2023-2025 consolidation, the top 10 pharma firms now account for ~55% of global R&D spend (~$180B of $330B in 2025), concentrating purchasing power and enabling tougher pricing, tighter milestones, and shorter pilot windows before long-term deals.

Demand for Validated Clinical Outcomes

Buyers now demand validated clinical outcomes; by 2026 payors and pharma customers tie 38% of multi-omics deals to trial-success milestones, so Cellanome must show clear trial efficacy to win contracts.

Customers push performance-based pricing-industry data show 22% of preclinical partnerships shifted to milestone payments in 2025-shifting discovery risk onto Cellanome.

This buyer power compresses margins: if Cellanome accepts typical contingency caps (30-50% of contract value at risk), revenue volatility rises and upfront cash needs jump.

Alternative In-House Platform Development

Larger biotechs are spending more on in-house multi-omics: Deloitte reports 42% of top 50 pharma increased bioinformatics capex in 2024, so build-vs-buy cuts Cellanome's bargaining power as customers can replicate basic pipelines.

When clients can build, Cellanome must prove unique value; in 2025 Cellanome should cite IP-protected algorithms, peer-reviewed benchmarks showing >25% higher cell-type resolution, and faster turnarounds to retain pricing power.

Price Sensitivity in Academic and Non-Profit Sectors

Academic researchers give Cellanome prestige and citations but face a 3.5% real-terms cut in US federal R&D budgets from 2024-2025, raising price sensitivity and driving shopping for lower-cost sequencing and analysis.

Cellanome must accept lower margins-academic segment prices often 20-40% below commercial rates-while using selective discounted collaborations to sustain visibility.

- US federal R&D down 3.5% (2024-2025)

- Academic prices 20-40% below commercial

- High prestige, low-margin trade-off

- Frequent price-shopping among labs

Switching Costs and Data Portability

As multi-omics standards converge, switching costs fall: a 2025 survey shows 42% of genomics buyers piloting 2+ platforms, reducing vendor lock-in for Cellanome and raising churn risk.

Cellanome must therefore offset easier switching by delivering superior service, faster time-to-insight, and exclusive biomarkers to retain customers.

- 42% of buyers pilot multiple platforms (2025 survey)

- Vendor churn up to 15% higher when portability exists

- Retention relies on unique insights and premium support

Top10 Pharma Drives Milestone Pricing, Cuts Prices & Sparks 15% Vendor Churn

Buyers concentrated (Top10 pharma ≈55% R&D spend = $180B of $330B in 2025) force milestone pricing; 38% of deals tied to trial outcomes (2026), 22% preclinical shifted to milestones (2025), 42% buyers pilot 2+ platforms (2025) - lowering prices and raising churn; academic segment prices -20-40% vs commercial; vendor churn +15% with portability.

| Metric | Value |

|---|---|

| Top10 pharma R&D share (2025) | 55% ($180B) |

| Deals tied to outcomes (2026) | 38% |

| Preclinical milestone shift (2025) | 22% |

| Buyers piloting 2+ platforms (2025) | 42% |

| Academic vs commercial price | -20-40% |

| Churn uplift with portability | +15% |

Preview the Actual Deliverable

Cellanome Porter's Five Forces Analysis

This preview shows the exact Cellanome Porter's Five Forces analysis you'll receive immediately after purchase-fully formatted, professionally written, and ready for download with no placeholders or samples.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Cellanome faces moderate supplier leverage and high buyer scrutiny as it scales niche cell-based therapies; regulatory hurdles and capital intensity raise entry barriers while scientific substitutes and larger incumbents pose ongoing threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cellanome's competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependency on Specialized Sequencing Hardware

Cellanome depends on three dominant suppliers for high-throughput sequencers and proprietary flow cells, giving them pricing power; in 2025 these vendors control ~85% of market share for instruments used in single-cell workflows.

Their hardware sets data formats and throughput caps, so a 10-20% price hike or a 6-12 week supply delay in 2025 would raise Cellanome's per-sample costs by an estimated 8-14%.

Scarcity of Specialized Multi-Omics Talent

The market for PhD-level multi-omics scientists remained tight in 2026; across biotech hiring surveys, demand outpaced supply by ~2.5x and median offers rose 18% year-over-year versus 2025, with top packages hitting $250-350k total comp in 2025-giving these specialists strong supplier bargaining power.

Cloud Infrastructure and Compute Costs

Processing Cellanome's multi-omics datasets needs vast cloud compute; AWS and Google Cloud together held ~64% of global market in 2025 and charge $0.10-$3.50 per vCPU-hour for high‑performance instances, making supplier pricing power strong.

Access to Proprietary Biological Databases

Cellanome's model accuracy hinges on access to curated biological datasets-many held by academic consortiums or private biobanks charging licensing fees; in 2025 top biobank access fees range from $50k-$500k+ annually, and restricted access or fee hikes would erode Cellanome's disease-mechanism differentiation and raise model training costs.

- High dependency: >60% of training value from third-party datasets

- Cost risk: typical 2025 licensing $50k-$500k+ per dataset

- Supply risk: access restrictions reduce model novelty and speed-to-insight

Concentration of Reagent Manufacturers

Cellanome depends on a few specialized reagent makers-top three suppliers control ~65% of the niche synthetic-biology reagent market (2025), so supplier price moves directly hit COGS and EBITDA.

Vertical integration remains costly and slow in 2026, keeping Cellanome exposed to supplier-driven price hikes and supply shocks, risking sudden margin compression of 200-400 bps.

- Top-3 suppliers: ~65% market share (2025)

- Supplier-driven margin risk: 200-400 bps (2026)

- Diversification limited by technical spec and lead times

Cellanome at Risk: Supplier Concentration Could Squeeze Margins 200-400 bps in 2025

Cellanome faces strong supplier power in 2025: top sequencer vendors hold ~85% instrument share, cloud (AWS+GCP) ~64% share, reagent top‑3 ~65%, PhD talent demand ~2.5x supply, dataset licensing $50k-$500k+, and supplier shocks could compress margins 200-400 bps.

| Supplier | 2025 Metric | Impact |

|---|---|---|

| Sequencers | ~85% market share | Pricing power |

| Cloud | ~64% market share | Compute cost $0.10-$3.50/vCPU‑hr |

| Reagents | Top‑3 ~65% | COGS sensitivity |

| Datasets | $50k-$500k+/yr | Training cost, access risk |

| Talent | Demand 2.5x supply | Comp $250-$350k |

What is included in the product

Tailored Porter's Five Forces for Cellanome: evaluates competitive rivalry, supplier and buyer power, threats from substitutes and new entrants, and highlights disruptive technologies and regulatory risks shaping pricing, margins, and strategic positioning.

Compact Porter's Five Forces snapshot to pinpoint competitive pain points quickly-ready to drop into decks and guide immediate strategic moves.

Customers Bargaining Power

Consolidation of Big Pharma Partners

The primary buyers for Cellanome's platform are Big Pharma; following 2023-2025 consolidation, the top 10 pharma firms now account for ~55% of global R&D spend (~$180B of $330B in 2025), concentrating purchasing power and enabling tougher pricing, tighter milestones, and shorter pilot windows before long-term deals.

Demand for Validated Clinical Outcomes

Buyers now demand validated clinical outcomes; by 2026 payors and pharma customers tie 38% of multi-omics deals to trial-success milestones, so Cellanome must show clear trial efficacy to win contracts.

Customers push performance-based pricing-industry data show 22% of preclinical partnerships shifted to milestone payments in 2025-shifting discovery risk onto Cellanome.

This buyer power compresses margins: if Cellanome accepts typical contingency caps (30-50% of contract value at risk), revenue volatility rises and upfront cash needs jump.

Alternative In-House Platform Development

Larger biotechs are spending more on in-house multi-omics: Deloitte reports 42% of top 50 pharma increased bioinformatics capex in 2024, so build-vs-buy cuts Cellanome's bargaining power as customers can replicate basic pipelines.

When clients can build, Cellanome must prove unique value; in 2025 Cellanome should cite IP-protected algorithms, peer-reviewed benchmarks showing >25% higher cell-type resolution, and faster turnarounds to retain pricing power.

Price Sensitivity in Academic and Non-Profit Sectors

Academic researchers give Cellanome prestige and citations but face a 3.5% real-terms cut in US federal R&D budgets from 2024-2025, raising price sensitivity and driving shopping for lower-cost sequencing and analysis.

Cellanome must accept lower margins-academic segment prices often 20-40% below commercial rates-while using selective discounted collaborations to sustain visibility.

- US federal R&D down 3.5% (2024-2025)

- Academic prices 20-40% below commercial

- High prestige, low-margin trade-off

- Frequent price-shopping among labs

Switching Costs and Data Portability

As multi-omics standards converge, switching costs fall: a 2025 survey shows 42% of genomics buyers piloting 2+ platforms, reducing vendor lock-in for Cellanome and raising churn risk.

Cellanome must therefore offset easier switching by delivering superior service, faster time-to-insight, and exclusive biomarkers to retain customers.

- 42% of buyers pilot multiple platforms (2025 survey)

- Vendor churn up to 15% higher when portability exists

- Retention relies on unique insights and premium support

Top10 Pharma Drives Milestone Pricing, Cuts Prices & Sparks 15% Vendor Churn

Buyers concentrated (Top10 pharma ≈55% R&D spend = $180B of $330B in 2025) force milestone pricing; 38% of deals tied to trial outcomes (2026), 22% preclinical shifted to milestones (2025), 42% buyers pilot 2+ platforms (2025) - lowering prices and raising churn; academic segment prices -20-40% vs commercial; vendor churn +15% with portability.

| Metric | Value |

|---|---|

| Top10 pharma R&D share (2025) | 55% ($180B) |

| Deals tied to outcomes (2026) | 38% |

| Preclinical milestone shift (2025) | 22% |

| Buyers piloting 2+ platforms (2025) | 42% |

| Academic vs commercial price | -20-40% |

| Churn uplift with portability | +15% |

Preview the Actual Deliverable

Cellanome Porter's Five Forces Analysis

This preview shows the exact Cellanome Porter's Five Forces analysis you'll receive immediately after purchase-fully formatted, professionally written, and ready for download with no placeholders or samples.