CMR SURGICAL PORTER'S FIVE FORCES TEMPLATE RESEARCH

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

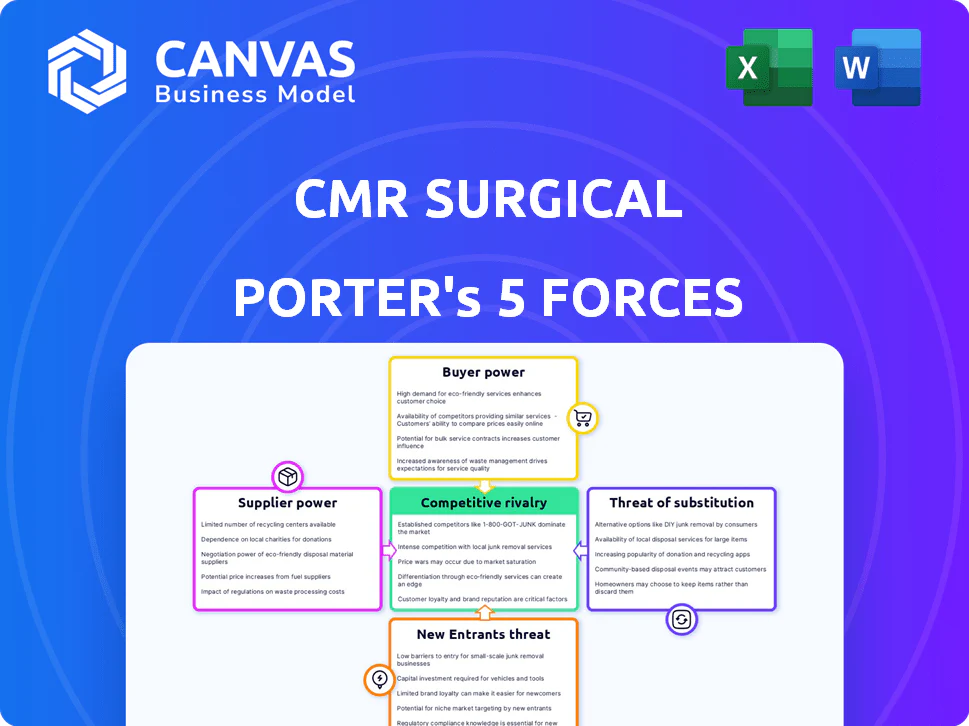

CMR Surgical faces intense competitive rivalry from established robotic-surgery players, moderate supplier power tied to specialized components, and significant buyer scrutiny as hospitals demand clear ROI-while regulatory hurdles and emerging substitutes shape its growth runway. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore CMR Surgical's competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Component Dependency

CMR Surgical depends on scarce medical-grade parts-precision sensors, HD imaging chips, and micro-motors-sourced from a few suppliers, giving suppliers moderate bargaining power as global surgical-robotics demand rose ~18% YoY into 2026. Suppliers' leverage tightened after 2025 when multi-vendor orders increased and lead times extended to 16-24 weeks, raising parts cost pressure on Versius production. Any supply disruption could cut CMR's 2026 unit growth target (management guided ~+40% system deployments) and delay revenue recognition tied to installations.

Proprietary Technology Integration

The Versius system's patented V-Wrist and modular arms use custom-fabricated parts, creating supplier lock-in: replacing a supplier would demand months of re-engineering and fresh regulatory clearance (e.g., 510(k) or CE-IVDR), raising switching costs above $20-50m in development and validation; thus partners wield substantial bargaining power given technical complexity and high exit costs.

Geopolitical and Tariff Risks

With manufacturing concentrated in the UK and global sourcing, CMR Surgical faced a 12-18% rise in input costs in 2025 after UK-EU customs frictions and US tariffs reshaped medtech trade, forcing suppliers to pass on price hikes and strengthening supplier bargaining power.

Regulatory and Quality Standards

Suppliers in surgical robotics must meet ISO 13485 and pass audits, shrinking the vendor pool; globally, roughly 1,200 medical device firms hold ISO 13485 and fewer than 150 supply precision robotic components suitable for CMR Surgical as of 2025.

CMR Surgical's FDA and CE Mark approvals tie to specific qualified suppliers, so replacing a vendor risks revalidation costs-often $5-15M and 12-18 months-raising supplier leverage.

This regulatory moat boosts bargaining power of the few compliant vendors, concentrating pricing and delivery risk amid CMR's high-stakes clinical safety requirements.

- ISO 13485: ~1,200 certified firms (2025)

- Qualified component suppliers: <150 (2025)

- Revalidation cost to swap supplier: $5-15M, 12-18 months

Scaling and Volume Pressure

As CMR Surgical ramps US launch for 2026, demand for high-tier manufacturing pits it against Intuitive Surgical (2025 revenue $7.0bn) and Medtronic ($35.5bn), letting suppliers favor larger, higher-volume buyers.

Suppliers of semiconductors and advanced alloys can push longer lead times or tougher pricing; volume-based leverage raises CMR's procurement risk.

- CMR must secure contracts before 2026 launch to avoid 6-12 month lead-time squeezes

Supplier squeeze: long lead times, cost spikes & costly revalidation threaten 2026 growth

Suppliers hold moderate-to-high power: ~<150 qualified precision vendors (2025), ISO13485 pool ~1,200; lead times 16-24 weeks; input costs +12-18% in 2025; switching/revalidation $5-15M and 12-18 months; CMR's 2026 deployment guide ~+40%-supplier disruption could cut growth.

| Metric | 2025 |

|---|---|

| Qualified suppliers | <150 |

| ISO13485 holders | ~1,200 |

| Lead times | 16-24 wks |

| Input cost rise | 12-18% |

| Revalidation cost/time | $5-15M /12-18 mths |

What is included in the product

Tailored Porter's Five Forces for CMR Surgical, revealing competitive intensity, buyer and supplier leverage, substitution risks from alternative surgical technologies, and entry barriers shaping its surgical robotics profitability and strategic positioning.

A concise Porter's Five Forces snapshot for CMR Surgical-shows competitive intensity, supplier and buyer leverage, threat of substitutes and entrants, and industry rivalry in one slide to speed strategic decisions.

Customers Bargaining Power

High Switching Costs and Training

Hospitals invest millions and hundreds of training hours in CMR Surgical's Versius modular system-CMR reported 2025 installed base growth of 48% and per-hospital capex averaging $1.2-1.8M-making switching to Intuitive's da Vinci 5 operationally disruptive and costly.

Alternative Platform Availability

In 2026 hospitals pick among CMR Surgical, Medtronic's Hugo RAS, and Intuitive's da Vinci 5, giving buyers strong leverage; global RAS installations rose ~18% in 2025 to ~9,600 systems, concentrating purchasing power in large networks.

CMR's modularity helps, but well-funded rivals (Intuitive FY2025 revenue $8.0B, Medtronic FY2025 revenue $34.3B) let networks extract discounts, lower per-procedure consumable fees, and better service or financing.

Consolidated Hospital Purchasing Power

Large US IDNs (e.g., Kaiser, HCA) and centralized systems in UK/NHS and India (AIIMS networks) push bulk discounts; in 2025 IDNs accounted for ~45% of hospital procurement spend and can demand 10-25% price cuts.

These super-buyers represent most of CMR Surgical's addressable revenue-losing one major network contract can cut regional share by 10-30%, given CMR's limited installed base in 2025 (estimated ~120 units globally).

Demand for Measurable ROI

Hospital CFOs in 2025-26, facing higher borrowing costs (US rates ~5%+), require proof that CMR Surgical systems improve throughput and cut total cost per procedure before approving $2-10m capital buys.

Buyers insist on clinical evidence and risk-sharing contracts tying manufacturer payments to procedure volume or outcomes, shifting pricing leverage to hospitals.

- Hospitals demand ROI within 3-5 years

- Risk-sharing deals commonly tie 10-30% of payments to outcomes

- Procurement teams control service-level and utilization clauses

Modular Flexibility as a Buyer Advantage

CMR Surgical's Versius modular design lets hospitals buy a single arm and add units later, making robotics affordable for mid-tier hospitals and ASCs; by FY2025 CMR reported 400+ worldwide installations, with ASCs representing ~28% of new customers, boosting bargaining power for smaller buyers who can scale spend over multiple CAPEX cycles.

- Modular entry lowers initial CAPEX (single-arm cost ~£150-200k vs legacy £1-2M)

- 400+ installations by FY2025; ASCs ~28% of new clients

- Buyers can customize upgrades, reducing lock-in and increasing negotiating leverage

IDNs and ASCs Drive Tough Price Cuts: 10-25% Discounts, 3-5yr ROI, 10-30% Risk Share

Buyers hold strong leverage: large IDNs (≈45% procurement share in 2025) and 9,600 global RAS systems let networks extract 10-25% discounts; CMR Surgical had ~400 installations (≈120 hospital units) in FY2025, with ASCs 28% of new customers and per-hospital capex £1.0-1.5M; buyers demand 3-5yr ROI and 10-30% risk‑share.

| Metric | 2025 |

|---|---|

| Global RAS systems | ~9,600 |

| CMR Surgical installations | ~400 |

| CMR hospital units | ~120 |

| ASC share of new clients | 28% |

| IDN procurement share | 45% |

| Typical buyer price cuts | 10-25% |

| Risk‑share portion | 10-30% |

| Required ROI window | 3-5 years |

What You See Is What You Get

CMR Surgical Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of CMR Surgical you'll receive immediately after purchase-no placeholders, no mockups.

The document displayed here is the professionally formatted, ready-to-use file you'll be able to download and employ the moment you buy; it contains the full competitive intensity, supplier/customer power, threat of substitutes and entrants, and rivalry assessment.

Original: $10.00

-65%$10.00

$3.50CMR SURGICAL PORTER'S FIVE FORCES TEMPLATE RESEARCH

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

CMR Surgical faces intense competitive rivalry from established robotic-surgery players, moderate supplier power tied to specialized components, and significant buyer scrutiny as hospitals demand clear ROI-while regulatory hurdles and emerging substitutes shape its growth runway. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore CMR Surgical's competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Component Dependency

CMR Surgical depends on scarce medical-grade parts-precision sensors, HD imaging chips, and micro-motors-sourced from a few suppliers, giving suppliers moderate bargaining power as global surgical-robotics demand rose ~18% YoY into 2026. Suppliers' leverage tightened after 2025 when multi-vendor orders increased and lead times extended to 16-24 weeks, raising parts cost pressure on Versius production. Any supply disruption could cut CMR's 2026 unit growth target (management guided ~+40% system deployments) and delay revenue recognition tied to installations.

Proprietary Technology Integration

The Versius system's patented V-Wrist and modular arms use custom-fabricated parts, creating supplier lock-in: replacing a supplier would demand months of re-engineering and fresh regulatory clearance (e.g., 510(k) or CE-IVDR), raising switching costs above $20-50m in development and validation; thus partners wield substantial bargaining power given technical complexity and high exit costs.

Geopolitical and Tariff Risks

With manufacturing concentrated in the UK and global sourcing, CMR Surgical faced a 12-18% rise in input costs in 2025 after UK-EU customs frictions and US tariffs reshaped medtech trade, forcing suppliers to pass on price hikes and strengthening supplier bargaining power.

Regulatory and Quality Standards

Suppliers in surgical robotics must meet ISO 13485 and pass audits, shrinking the vendor pool; globally, roughly 1,200 medical device firms hold ISO 13485 and fewer than 150 supply precision robotic components suitable for CMR Surgical as of 2025.

CMR Surgical's FDA and CE Mark approvals tie to specific qualified suppliers, so replacing a vendor risks revalidation costs-often $5-15M and 12-18 months-raising supplier leverage.

This regulatory moat boosts bargaining power of the few compliant vendors, concentrating pricing and delivery risk amid CMR's high-stakes clinical safety requirements.

- ISO 13485: ~1,200 certified firms (2025)

- Qualified component suppliers: <150 (2025)

- Revalidation cost to swap supplier: $5-15M, 12-18 months

Scaling and Volume Pressure

As CMR Surgical ramps US launch for 2026, demand for high-tier manufacturing pits it against Intuitive Surgical (2025 revenue $7.0bn) and Medtronic ($35.5bn), letting suppliers favor larger, higher-volume buyers.

Suppliers of semiconductors and advanced alloys can push longer lead times or tougher pricing; volume-based leverage raises CMR's procurement risk.

- CMR must secure contracts before 2026 launch to avoid 6-12 month lead-time squeezes

Supplier squeeze: long lead times, cost spikes & costly revalidation threaten 2026 growth

Suppliers hold moderate-to-high power: ~<150 qualified precision vendors (2025), ISO13485 pool ~1,200; lead times 16-24 weeks; input costs +12-18% in 2025; switching/revalidation $5-15M and 12-18 months; CMR's 2026 deployment guide ~+40%-supplier disruption could cut growth.

| Metric | 2025 |

|---|---|

| Qualified suppliers | <150 |

| ISO13485 holders | ~1,200 |

| Lead times | 16-24 wks |

| Input cost rise | 12-18% |

| Revalidation cost/time | $5-15M /12-18 mths |

What is included in the product

Tailored Porter's Five Forces for CMR Surgical, revealing competitive intensity, buyer and supplier leverage, substitution risks from alternative surgical technologies, and entry barriers shaping its surgical robotics profitability and strategic positioning.

A concise Porter's Five Forces snapshot for CMR Surgical-shows competitive intensity, supplier and buyer leverage, threat of substitutes and entrants, and industry rivalry in one slide to speed strategic decisions.

Customers Bargaining Power

High Switching Costs and Training

Hospitals invest millions and hundreds of training hours in CMR Surgical's Versius modular system-CMR reported 2025 installed base growth of 48% and per-hospital capex averaging $1.2-1.8M-making switching to Intuitive's da Vinci 5 operationally disruptive and costly.

Alternative Platform Availability

In 2026 hospitals pick among CMR Surgical, Medtronic's Hugo RAS, and Intuitive's da Vinci 5, giving buyers strong leverage; global RAS installations rose ~18% in 2025 to ~9,600 systems, concentrating purchasing power in large networks.

CMR's modularity helps, but well-funded rivals (Intuitive FY2025 revenue $8.0B, Medtronic FY2025 revenue $34.3B) let networks extract discounts, lower per-procedure consumable fees, and better service or financing.

Consolidated Hospital Purchasing Power

Large US IDNs (e.g., Kaiser, HCA) and centralized systems in UK/NHS and India (AIIMS networks) push bulk discounts; in 2025 IDNs accounted for ~45% of hospital procurement spend and can demand 10-25% price cuts.

These super-buyers represent most of CMR Surgical's addressable revenue-losing one major network contract can cut regional share by 10-30%, given CMR's limited installed base in 2025 (estimated ~120 units globally).

Demand for Measurable ROI

Hospital CFOs in 2025-26, facing higher borrowing costs (US rates ~5%+), require proof that CMR Surgical systems improve throughput and cut total cost per procedure before approving $2-10m capital buys.

Buyers insist on clinical evidence and risk-sharing contracts tying manufacturer payments to procedure volume or outcomes, shifting pricing leverage to hospitals.

- Hospitals demand ROI within 3-5 years

- Risk-sharing deals commonly tie 10-30% of payments to outcomes

- Procurement teams control service-level and utilization clauses

Modular Flexibility as a Buyer Advantage

CMR Surgical's Versius modular design lets hospitals buy a single arm and add units later, making robotics affordable for mid-tier hospitals and ASCs; by FY2025 CMR reported 400+ worldwide installations, with ASCs representing ~28% of new customers, boosting bargaining power for smaller buyers who can scale spend over multiple CAPEX cycles.

- Modular entry lowers initial CAPEX (single-arm cost ~£150-200k vs legacy £1-2M)

- 400+ installations by FY2025; ASCs ~28% of new clients

- Buyers can customize upgrades, reducing lock-in and increasing negotiating leverage

IDNs and ASCs Drive Tough Price Cuts: 10-25% Discounts, 3-5yr ROI, 10-30% Risk Share

Buyers hold strong leverage: large IDNs (≈45% procurement share in 2025) and 9,600 global RAS systems let networks extract 10-25% discounts; CMR Surgical had ~400 installations (≈120 hospital units) in FY2025, with ASCs 28% of new customers and per-hospital capex £1.0-1.5M; buyers demand 3-5yr ROI and 10-30% risk‑share.

| Metric | 2025 |

|---|---|

| Global RAS systems | ~9,600 |

| CMR Surgical installations | ~400 |

| CMR hospital units | ~120 |

| ASC share of new clients | 28% |

| IDN procurement share | 45% |

| Typical buyer price cuts | 10-25% |

| Risk‑share portion | 10-30% |

| Required ROI window | 3-5 years |

What You See Is What You Get

CMR Surgical Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of CMR Surgical you'll receive immediately after purchase-no placeholders, no mockups.

The document displayed here is the professionally formatted, ready-to-use file you'll be able to download and employ the moment you buy; it contains the full competitive intensity, supplier/customer power, threat of substitutes and entrants, and rivalry assessment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

CMR Surgical faces intense competitive rivalry from established robotic-surgery players, moderate supplier power tied to specialized components, and significant buyer scrutiny as hospitals demand clear ROI-while regulatory hurdles and emerging substitutes shape its growth runway. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore CMR Surgical's competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Component Dependency

CMR Surgical depends on scarce medical-grade parts-precision sensors, HD imaging chips, and micro-motors-sourced from a few suppliers, giving suppliers moderate bargaining power as global surgical-robotics demand rose ~18% YoY into 2026. Suppliers' leverage tightened after 2025 when multi-vendor orders increased and lead times extended to 16-24 weeks, raising parts cost pressure on Versius production. Any supply disruption could cut CMR's 2026 unit growth target (management guided ~+40% system deployments) and delay revenue recognition tied to installations.

Proprietary Technology Integration

The Versius system's patented V-Wrist and modular arms use custom-fabricated parts, creating supplier lock-in: replacing a supplier would demand months of re-engineering and fresh regulatory clearance (e.g., 510(k) or CE-IVDR), raising switching costs above $20-50m in development and validation; thus partners wield substantial bargaining power given technical complexity and high exit costs.

Geopolitical and Tariff Risks

With manufacturing concentrated in the UK and global sourcing, CMR Surgical faced a 12-18% rise in input costs in 2025 after UK-EU customs frictions and US tariffs reshaped medtech trade, forcing suppliers to pass on price hikes and strengthening supplier bargaining power.

Regulatory and Quality Standards

Suppliers in surgical robotics must meet ISO 13485 and pass audits, shrinking the vendor pool; globally, roughly 1,200 medical device firms hold ISO 13485 and fewer than 150 supply precision robotic components suitable for CMR Surgical as of 2025.

CMR Surgical's FDA and CE Mark approvals tie to specific qualified suppliers, so replacing a vendor risks revalidation costs-often $5-15M and 12-18 months-raising supplier leverage.

This regulatory moat boosts bargaining power of the few compliant vendors, concentrating pricing and delivery risk amid CMR's high-stakes clinical safety requirements.

- ISO 13485: ~1,200 certified firms (2025)

- Qualified component suppliers: <150 (2025)

- Revalidation cost to swap supplier: $5-15M, 12-18 months

Scaling and Volume Pressure

As CMR Surgical ramps US launch for 2026, demand for high-tier manufacturing pits it against Intuitive Surgical (2025 revenue $7.0bn) and Medtronic ($35.5bn), letting suppliers favor larger, higher-volume buyers.

Suppliers of semiconductors and advanced alloys can push longer lead times or tougher pricing; volume-based leverage raises CMR's procurement risk.

- CMR must secure contracts before 2026 launch to avoid 6-12 month lead-time squeezes

Supplier squeeze: long lead times, cost spikes & costly revalidation threaten 2026 growth

Suppliers hold moderate-to-high power: ~<150 qualified precision vendors (2025), ISO13485 pool ~1,200; lead times 16-24 weeks; input costs +12-18% in 2025; switching/revalidation $5-15M and 12-18 months; CMR's 2026 deployment guide ~+40%-supplier disruption could cut growth.

| Metric | 2025 |

|---|---|

| Qualified suppliers | <150 |

| ISO13485 holders | ~1,200 |

| Lead times | 16-24 wks |

| Input cost rise | 12-18% |

| Revalidation cost/time | $5-15M /12-18 mths |

What is included in the product

Tailored Porter's Five Forces for CMR Surgical, revealing competitive intensity, buyer and supplier leverage, substitution risks from alternative surgical technologies, and entry barriers shaping its surgical robotics profitability and strategic positioning.

A concise Porter's Five Forces snapshot for CMR Surgical-shows competitive intensity, supplier and buyer leverage, threat of substitutes and entrants, and industry rivalry in one slide to speed strategic decisions.

Customers Bargaining Power

High Switching Costs and Training

Hospitals invest millions and hundreds of training hours in CMR Surgical's Versius modular system-CMR reported 2025 installed base growth of 48% and per-hospital capex averaging $1.2-1.8M-making switching to Intuitive's da Vinci 5 operationally disruptive and costly.

Alternative Platform Availability

In 2026 hospitals pick among CMR Surgical, Medtronic's Hugo RAS, and Intuitive's da Vinci 5, giving buyers strong leverage; global RAS installations rose ~18% in 2025 to ~9,600 systems, concentrating purchasing power in large networks.

CMR's modularity helps, but well-funded rivals (Intuitive FY2025 revenue $8.0B, Medtronic FY2025 revenue $34.3B) let networks extract discounts, lower per-procedure consumable fees, and better service or financing.

Consolidated Hospital Purchasing Power

Large US IDNs (e.g., Kaiser, HCA) and centralized systems in UK/NHS and India (AIIMS networks) push bulk discounts; in 2025 IDNs accounted for ~45% of hospital procurement spend and can demand 10-25% price cuts.

These super-buyers represent most of CMR Surgical's addressable revenue-losing one major network contract can cut regional share by 10-30%, given CMR's limited installed base in 2025 (estimated ~120 units globally).

Demand for Measurable ROI

Hospital CFOs in 2025-26, facing higher borrowing costs (US rates ~5%+), require proof that CMR Surgical systems improve throughput and cut total cost per procedure before approving $2-10m capital buys.

Buyers insist on clinical evidence and risk-sharing contracts tying manufacturer payments to procedure volume or outcomes, shifting pricing leverage to hospitals.

- Hospitals demand ROI within 3-5 years

- Risk-sharing deals commonly tie 10-30% of payments to outcomes

- Procurement teams control service-level and utilization clauses

Modular Flexibility as a Buyer Advantage

CMR Surgical's Versius modular design lets hospitals buy a single arm and add units later, making robotics affordable for mid-tier hospitals and ASCs; by FY2025 CMR reported 400+ worldwide installations, with ASCs representing ~28% of new customers, boosting bargaining power for smaller buyers who can scale spend over multiple CAPEX cycles.

- Modular entry lowers initial CAPEX (single-arm cost ~£150-200k vs legacy £1-2M)

- 400+ installations by FY2025; ASCs ~28% of new clients

- Buyers can customize upgrades, reducing lock-in and increasing negotiating leverage

IDNs and ASCs Drive Tough Price Cuts: 10-25% Discounts, 3-5yr ROI, 10-30% Risk Share

Buyers hold strong leverage: large IDNs (≈45% procurement share in 2025) and 9,600 global RAS systems let networks extract 10-25% discounts; CMR Surgical had ~400 installations (≈120 hospital units) in FY2025, with ASCs 28% of new customers and per-hospital capex £1.0-1.5M; buyers demand 3-5yr ROI and 10-30% risk‑share.

| Metric | 2025 |

|---|---|

| Global RAS systems | ~9,600 |

| CMR Surgical installations | ~400 |

| CMR hospital units | ~120 |

| ASC share of new clients | 28% |

| IDN procurement share | 45% |

| Typical buyer price cuts | 10-25% |

| Risk‑share portion | 10-30% |

| Required ROI window | 3-5 years |

What You See Is What You Get

CMR Surgical Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of CMR Surgical you'll receive immediately after purchase-no placeholders, no mockups.

The document displayed here is the professionally formatted, ready-to-use file you'll be able to download and employ the moment you buy; it contains the full competitive intensity, supplier/customer power, threat of substitutes and entrants, and rivalry assessment.