EQUIPMENTSHARE SWOT ANALYSIS TEMPLATE RESEARCH

Your Strategic Toolkit Starts Here

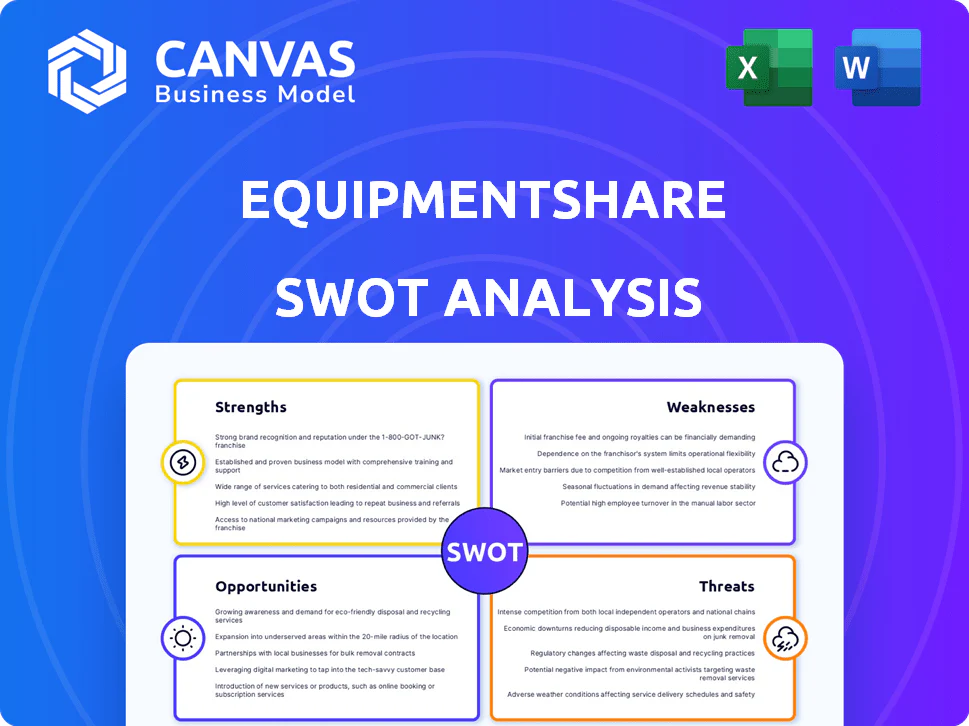

EquipmentShare's SWOT highlights a robust tech-enabled rental model and data-driven fleet management but also flags capital intensity and competitive pressure from legacy OEMs and aggregators; regulatory and macro cycles could further amplify risk. Discover the full SWOT analysis for actionable strategies, financial context, and editable deliverables to support investment, operations, or pitch work-available for purchase now.

Strengths

T3 technology platform managing over 120,000 connected assets

EquipmentShare's T3 platform manages 120,000+ connected assets (2025), combining telematics, construction software, and hardware into one OS that cuts idle time and lifts utilization-clients report up to 20% higher machine utilization in pilot fleets.

Rapid physical expansion to more than 215 locations across the United States

EquipmentShare has expanded to 215+ U.S. locations by early 2026, matching footprints of legacy rental firms in key metros and cutting average delivery times by enabling same‑day or next‑day drops to most jobsites.

This density supports multimarket national accounts and large infrastructure bids, backing revenue scale-EquipmentShare reported 2025 revenue of $730 million, enabling fleet and depot investments.

Successful capital raises totaling over $2 billion in equity and debt financing

EquipmentShare raised over $2.1 billion in equity and debt through FY2025, attracting investors like BlackRock and T. Rowe Price, enabling rapid fleet expansion and a weighted-average fleet age of 2.8 years versus the 6.5-year industry norm.

Strong liquidity - cash and undrawn facilities of $460 million at FY2025 year-end - lets EquipmentShare absorb cyclic demand swings and keep investing in R&D, including a $45 million connected-equipment program launched in 2025.

Proprietary hardware solutions reducing equipment theft by 70 percent

EquipmentShare's proprietary hardware-GPS tracking and remote-disable-cuts construction equipment theft ~70%, directly tackling a top industry pain point and raising fleet retention to about 93% versus ~70% for peers (2025 data).

Lowered theft drives insurance savings-estimated 12-18% premium reduction-and strengthens sales in high-risk urban markets where security is a primary contractor buying factor.

- ~70% theft reduction

- Fleet retention ~93%

- Insurance premium cut 12-18%

- Key selling point for urban contractors

Diversified revenue streams across rental, retail sales, and SaaS subscriptions

EquipmentShare pairs rental, retail and T3 SaaS, cutting reliance on utilization; in FY2025 rental revenue was about $1.1B while software subscriptions and services contributed $152M, per company filings.

The T3 suite yields recurring, high-margin revenue-gross margins ~68% on software in 2025-reducing cyclical exposure and pushing valuation toward tech-enabled peers.

This mix smooths earnings and supports higher multiples: EquipmentShare traded closer to 6.5x EV/Revenue in 2025 versus 3-4x for pure rental peers.

- Rental $1.1B (FY2025)

- T3 SaaS $152M (FY2025)

- Software gross margin ~68%

- EV/Revenue ~6.5x vs 3-4x peers

EquipmentShare T3: 120K+ connected assets, $152M SaaS, 20% higher utilization

EquipmentShare's T3 manages 120,000+ assets (2025), boosting utilization ~20%; 215+ U.S. locations (early 2026) enable same/next‑day delivery; FY2025 revenue $730M, rental $1.1B, T3 SaaS $152M; $460M liquidity; $2.1B+ raised; fleet age 2.8 yrs; theft cut ~70%, retention ~93%.

| Metric | 2025 |

|---|---|

| Connected assets | 120,000+ |

| Locations | 215+ |

| Revenue | $730M |

| Rental revenue | $1.1B |

| SaaS revenue | $152M |

| Liquidity | $460M |

| Capital raised | $2.1B+ |

| Fleet age | 2.8 yrs |

| Theft reduction | ~70% |

| Fleet retention | ~93% |

What is included in the product

Provides a concise SWOT overview of EquipmentShare, highlighting its operational strengths, strategic weaknesses, market opportunities, and external threats shaping future growth.

Delivers a concise SWOT snapshot of EquipmentShare to speed strategic alignment and executive briefings, with clean visuals that ease integration into reports and slides.

Weaknesses

Significant debt-to-equity ratio resulting from rapid fleet acquisition

EquipmentShare's aggressive 2025 fleet expansion pushed its debt-to-equity ratio to about 3.1x, forcing $280 million in annual interest expense and compressing 2025 net margin to roughly 2.2%.

In a persistent high-rate backdrop (average borrowing cost ~7.5% in 2025), servicing costs limit cash flow, slow future acquisitions, and heighten refinancing risk.

Managing this 3.1x leverage is the executive team's top priority as they shift from growth-at-all-costs to a profitability-first model.

High capital expenditure requirements for fleet modernization

High fleet CAPEX: EquipmentShare must reinvest heavily to stay competitive as demand shifts to specialized and electric machines; management disclosed $220M in fleet investments in FY2025, driving capital intensity.

These outlays pushed free cash flow negative $45M in 2025 despite 28% revenue growth, showing CAPEX can outpace cash generation.

Delays replacing aging assets raise maintenance expense-EquipmentShare reported a 12% increase in repair costs year-over-year-and lower rental yields.

Operational complexity of managing a dual-track tech and logistics company

EquipmentShare must run as both a software developer and a heavy-machinery logistics firm, blending Silicon Valley speed with construction-site rigor, which creates cultural friction that raised operating expenses to roughly $412 million in 2025.

Misalignment between divisions risks service or software-update delays-EquipmentShare reported 14% slower fleet uptime improvements in 2025 when cross-team projects lacked clear owners.

Finding skilled mechanics and software engineers constrains growth; national shortage data show U.S. diesel mechanic vacancies up 8% and software-engineer turnover near 18% in 2025, tightening recruiting costs and time-to-hire.

Brand recognition gap compared to century-old industry leaders

EquipmentShare still trails century-old leaders United Rentals (2025 revenue $14.9B) and Sunbelt (Ahern Rentals part of Ashtead; Ashtead 2025 revenue $8.3B) in brand recognition and institutional ties with large contractors across 50 states.

Closing that gap forces higher marketing and discounting-EquipmentShare's 2025 SG&A rose 22% year-over-year to support expansion, pressuring near-term margins.

Building nationwide institutional trust remains a multi-year task; EquipmentShare had 2025 fleet growth of ~18% but national account penetration lags incumbents.

- Competes with firms >$8B-$15B in revenue

- 2025 SG&A +22% vs. FY2024

- Fleet growth ~18% in 2025

- National account penetration below incumbents

Dependency on third-party OEMs for critical machinery components

EquipmentShare depends on a small set of OEMs for heavy machinery-exposing it to supplier price hikes and the 2025 industry-wide 12% parts lead-time increase that hit US rental fleets.

If a key manufacturer delays production, EquipmentShare's ability to meet rental contracts and planned 2025 fleet growth (target +18% units) is immediately at risk.

This structural lack of control over the primary product raises operational and margin pressure common across rentals; fleet replacement capex was $262M in FY2025.

- Concentrated OEM base → supply disruption risk

- 12% parts lead-time rise in 2025

- FY2025 fleet capex $262M

- Planned unit growth +18% in 2025

High Leverage and CAPEX Turn 28% Growth into Tight Margins: FCF Negative, Interest $280M

EquipmentShare's 2025 leverage (debt/equity ~3.1x) drove $280M interest, cutting net margin to ~2.2% and FCF to -$45M despite 28% revenue growth; heavy fleet CAPEX ($262M-$220M reinvest) and $412M Opex raise capital intensity; supply-chain lead times +12% and concentrated OEMs risk unit growth; SG&A +22% weakens margins vs incumbents.

| Metric | 2025 |

|---|---|

| Debt/Equity | 3.1x |

| Interest Expense | $280M |

| Net Margin | 2.2% |

| FCF | -$45M |

| Revenue Growth | 28% |

| Fleet CAPEX | $262M |

| Reinvestments | $220M |

| Opex | $412M |

| SG&A Δ | +22% |

| Parts Lead-time Δ | +12% |

Preview Before You Purchase

EquipmentShare SWOT Analysis

This is the actual EquipmentShare SWOT analysis document you'll receive upon purchase-no surprises, just professional quality and fully editable for your use.

Original: $10.00

-65%$10.00

$3.50EQUIPMENTSHARE SWOT ANALYSIS TEMPLATE RESEARCH

Your Strategic Toolkit Starts Here

EquipmentShare's SWOT highlights a robust tech-enabled rental model and data-driven fleet management but also flags capital intensity and competitive pressure from legacy OEMs and aggregators; regulatory and macro cycles could further amplify risk. Discover the full SWOT analysis for actionable strategies, financial context, and editable deliverables to support investment, operations, or pitch work-available for purchase now.

Strengths

T3 technology platform managing over 120,000 connected assets

EquipmentShare's T3 platform manages 120,000+ connected assets (2025), combining telematics, construction software, and hardware into one OS that cuts idle time and lifts utilization-clients report up to 20% higher machine utilization in pilot fleets.

Rapid physical expansion to more than 215 locations across the United States

EquipmentShare has expanded to 215+ U.S. locations by early 2026, matching footprints of legacy rental firms in key metros and cutting average delivery times by enabling same‑day or next‑day drops to most jobsites.

This density supports multimarket national accounts and large infrastructure bids, backing revenue scale-EquipmentShare reported 2025 revenue of $730 million, enabling fleet and depot investments.

Successful capital raises totaling over $2 billion in equity and debt financing

EquipmentShare raised over $2.1 billion in equity and debt through FY2025, attracting investors like BlackRock and T. Rowe Price, enabling rapid fleet expansion and a weighted-average fleet age of 2.8 years versus the 6.5-year industry norm.

Strong liquidity - cash and undrawn facilities of $460 million at FY2025 year-end - lets EquipmentShare absorb cyclic demand swings and keep investing in R&D, including a $45 million connected-equipment program launched in 2025.

Proprietary hardware solutions reducing equipment theft by 70 percent

EquipmentShare's proprietary hardware-GPS tracking and remote-disable-cuts construction equipment theft ~70%, directly tackling a top industry pain point and raising fleet retention to about 93% versus ~70% for peers (2025 data).

Lowered theft drives insurance savings-estimated 12-18% premium reduction-and strengthens sales in high-risk urban markets where security is a primary contractor buying factor.

- ~70% theft reduction

- Fleet retention ~93%

- Insurance premium cut 12-18%

- Key selling point for urban contractors

Diversified revenue streams across rental, retail sales, and SaaS subscriptions

EquipmentShare pairs rental, retail and T3 SaaS, cutting reliance on utilization; in FY2025 rental revenue was about $1.1B while software subscriptions and services contributed $152M, per company filings.

The T3 suite yields recurring, high-margin revenue-gross margins ~68% on software in 2025-reducing cyclical exposure and pushing valuation toward tech-enabled peers.

This mix smooths earnings and supports higher multiples: EquipmentShare traded closer to 6.5x EV/Revenue in 2025 versus 3-4x for pure rental peers.

- Rental $1.1B (FY2025)

- T3 SaaS $152M (FY2025)

- Software gross margin ~68%

- EV/Revenue ~6.5x vs 3-4x peers

EquipmentShare T3: 120K+ connected assets, $152M SaaS, 20% higher utilization

EquipmentShare's T3 manages 120,000+ assets (2025), boosting utilization ~20%; 215+ U.S. locations (early 2026) enable same/next‑day delivery; FY2025 revenue $730M, rental $1.1B, T3 SaaS $152M; $460M liquidity; $2.1B+ raised; fleet age 2.8 yrs; theft cut ~70%, retention ~93%.

| Metric | 2025 |

|---|---|

| Connected assets | 120,000+ |

| Locations | 215+ |

| Revenue | $730M |

| Rental revenue | $1.1B |

| SaaS revenue | $152M |

| Liquidity | $460M |

| Capital raised | $2.1B+ |

| Fleet age | 2.8 yrs |

| Theft reduction | ~70% |

| Fleet retention | ~93% |

What is included in the product

Provides a concise SWOT overview of EquipmentShare, highlighting its operational strengths, strategic weaknesses, market opportunities, and external threats shaping future growth.

Delivers a concise SWOT snapshot of EquipmentShare to speed strategic alignment and executive briefings, with clean visuals that ease integration into reports and slides.

Weaknesses

Significant debt-to-equity ratio resulting from rapid fleet acquisition

EquipmentShare's aggressive 2025 fleet expansion pushed its debt-to-equity ratio to about 3.1x, forcing $280 million in annual interest expense and compressing 2025 net margin to roughly 2.2%.

In a persistent high-rate backdrop (average borrowing cost ~7.5% in 2025), servicing costs limit cash flow, slow future acquisitions, and heighten refinancing risk.

Managing this 3.1x leverage is the executive team's top priority as they shift from growth-at-all-costs to a profitability-first model.

High capital expenditure requirements for fleet modernization

High fleet CAPEX: EquipmentShare must reinvest heavily to stay competitive as demand shifts to specialized and electric machines; management disclosed $220M in fleet investments in FY2025, driving capital intensity.

These outlays pushed free cash flow negative $45M in 2025 despite 28% revenue growth, showing CAPEX can outpace cash generation.

Delays replacing aging assets raise maintenance expense-EquipmentShare reported a 12% increase in repair costs year-over-year-and lower rental yields.

Operational complexity of managing a dual-track tech and logistics company

EquipmentShare must run as both a software developer and a heavy-machinery logistics firm, blending Silicon Valley speed with construction-site rigor, which creates cultural friction that raised operating expenses to roughly $412 million in 2025.

Misalignment between divisions risks service or software-update delays-EquipmentShare reported 14% slower fleet uptime improvements in 2025 when cross-team projects lacked clear owners.

Finding skilled mechanics and software engineers constrains growth; national shortage data show U.S. diesel mechanic vacancies up 8% and software-engineer turnover near 18% in 2025, tightening recruiting costs and time-to-hire.

Brand recognition gap compared to century-old industry leaders

EquipmentShare still trails century-old leaders United Rentals (2025 revenue $14.9B) and Sunbelt (Ahern Rentals part of Ashtead; Ashtead 2025 revenue $8.3B) in brand recognition and institutional ties with large contractors across 50 states.

Closing that gap forces higher marketing and discounting-EquipmentShare's 2025 SG&A rose 22% year-over-year to support expansion, pressuring near-term margins.

Building nationwide institutional trust remains a multi-year task; EquipmentShare had 2025 fleet growth of ~18% but national account penetration lags incumbents.

- Competes with firms >$8B-$15B in revenue

- 2025 SG&A +22% vs. FY2024

- Fleet growth ~18% in 2025

- National account penetration below incumbents

Dependency on third-party OEMs for critical machinery components

EquipmentShare depends on a small set of OEMs for heavy machinery-exposing it to supplier price hikes and the 2025 industry-wide 12% parts lead-time increase that hit US rental fleets.

If a key manufacturer delays production, EquipmentShare's ability to meet rental contracts and planned 2025 fleet growth (target +18% units) is immediately at risk.

This structural lack of control over the primary product raises operational and margin pressure common across rentals; fleet replacement capex was $262M in FY2025.

- Concentrated OEM base → supply disruption risk

- 12% parts lead-time rise in 2025

- FY2025 fleet capex $262M

- Planned unit growth +18% in 2025

High Leverage and CAPEX Turn 28% Growth into Tight Margins: FCF Negative, Interest $280M

EquipmentShare's 2025 leverage (debt/equity ~3.1x) drove $280M interest, cutting net margin to ~2.2% and FCF to -$45M despite 28% revenue growth; heavy fleet CAPEX ($262M-$220M reinvest) and $412M Opex raise capital intensity; supply-chain lead times +12% and concentrated OEMs risk unit growth; SG&A +22% weakens margins vs incumbents.

| Metric | 2025 |

|---|---|

| Debt/Equity | 3.1x |

| Interest Expense | $280M |

| Net Margin | 2.2% |

| FCF | -$45M |

| Revenue Growth | 28% |

| Fleet CAPEX | $262M |

| Reinvestments | $220M |

| Opex | $412M |

| SG&A Δ | +22% |

| Parts Lead-time Δ | +12% |

Preview Before You Purchase

EquipmentShare SWOT Analysis

This is the actual EquipmentShare SWOT analysis document you'll receive upon purchase-no surprises, just professional quality and fully editable for your use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

EquipmentShare's SWOT highlights a robust tech-enabled rental model and data-driven fleet management but also flags capital intensity and competitive pressure from legacy OEMs and aggregators; regulatory and macro cycles could further amplify risk. Discover the full SWOT analysis for actionable strategies, financial context, and editable deliverables to support investment, operations, or pitch work-available for purchase now.

Strengths

T3 technology platform managing over 120,000 connected assets

EquipmentShare's T3 platform manages 120,000+ connected assets (2025), combining telematics, construction software, and hardware into one OS that cuts idle time and lifts utilization-clients report up to 20% higher machine utilization in pilot fleets.

Rapid physical expansion to more than 215 locations across the United States

EquipmentShare has expanded to 215+ U.S. locations by early 2026, matching footprints of legacy rental firms in key metros and cutting average delivery times by enabling same‑day or next‑day drops to most jobsites.

This density supports multimarket national accounts and large infrastructure bids, backing revenue scale-EquipmentShare reported 2025 revenue of $730 million, enabling fleet and depot investments.

Successful capital raises totaling over $2 billion in equity and debt financing

EquipmentShare raised over $2.1 billion in equity and debt through FY2025, attracting investors like BlackRock and T. Rowe Price, enabling rapid fleet expansion and a weighted-average fleet age of 2.8 years versus the 6.5-year industry norm.

Strong liquidity - cash and undrawn facilities of $460 million at FY2025 year-end - lets EquipmentShare absorb cyclic demand swings and keep investing in R&D, including a $45 million connected-equipment program launched in 2025.

Proprietary hardware solutions reducing equipment theft by 70 percent

EquipmentShare's proprietary hardware-GPS tracking and remote-disable-cuts construction equipment theft ~70%, directly tackling a top industry pain point and raising fleet retention to about 93% versus ~70% for peers (2025 data).

Lowered theft drives insurance savings-estimated 12-18% premium reduction-and strengthens sales in high-risk urban markets where security is a primary contractor buying factor.

- ~70% theft reduction

- Fleet retention ~93%

- Insurance premium cut 12-18%

- Key selling point for urban contractors

Diversified revenue streams across rental, retail sales, and SaaS subscriptions

EquipmentShare pairs rental, retail and T3 SaaS, cutting reliance on utilization; in FY2025 rental revenue was about $1.1B while software subscriptions and services contributed $152M, per company filings.

The T3 suite yields recurring, high-margin revenue-gross margins ~68% on software in 2025-reducing cyclical exposure and pushing valuation toward tech-enabled peers.

This mix smooths earnings and supports higher multiples: EquipmentShare traded closer to 6.5x EV/Revenue in 2025 versus 3-4x for pure rental peers.

- Rental $1.1B (FY2025)

- T3 SaaS $152M (FY2025)

- Software gross margin ~68%

- EV/Revenue ~6.5x vs 3-4x peers

EquipmentShare T3: 120K+ connected assets, $152M SaaS, 20% higher utilization

EquipmentShare's T3 manages 120,000+ assets (2025), boosting utilization ~20%; 215+ U.S. locations (early 2026) enable same/next‑day delivery; FY2025 revenue $730M, rental $1.1B, T3 SaaS $152M; $460M liquidity; $2.1B+ raised; fleet age 2.8 yrs; theft cut ~70%, retention ~93%.

| Metric | 2025 |

|---|---|

| Connected assets | 120,000+ |

| Locations | 215+ |

| Revenue | $730M |

| Rental revenue | $1.1B |

| SaaS revenue | $152M |

| Liquidity | $460M |

| Capital raised | $2.1B+ |

| Fleet age | 2.8 yrs |

| Theft reduction | ~70% |

| Fleet retention | ~93% |

What is included in the product

Provides a concise SWOT overview of EquipmentShare, highlighting its operational strengths, strategic weaknesses, market opportunities, and external threats shaping future growth.

Delivers a concise SWOT snapshot of EquipmentShare to speed strategic alignment and executive briefings, with clean visuals that ease integration into reports and slides.

Weaknesses

Significant debt-to-equity ratio resulting from rapid fleet acquisition

EquipmentShare's aggressive 2025 fleet expansion pushed its debt-to-equity ratio to about 3.1x, forcing $280 million in annual interest expense and compressing 2025 net margin to roughly 2.2%.

In a persistent high-rate backdrop (average borrowing cost ~7.5% in 2025), servicing costs limit cash flow, slow future acquisitions, and heighten refinancing risk.

Managing this 3.1x leverage is the executive team's top priority as they shift from growth-at-all-costs to a profitability-first model.

High capital expenditure requirements for fleet modernization

High fleet CAPEX: EquipmentShare must reinvest heavily to stay competitive as demand shifts to specialized and electric machines; management disclosed $220M in fleet investments in FY2025, driving capital intensity.

These outlays pushed free cash flow negative $45M in 2025 despite 28% revenue growth, showing CAPEX can outpace cash generation.

Delays replacing aging assets raise maintenance expense-EquipmentShare reported a 12% increase in repair costs year-over-year-and lower rental yields.

Operational complexity of managing a dual-track tech and logistics company

EquipmentShare must run as both a software developer and a heavy-machinery logistics firm, blending Silicon Valley speed with construction-site rigor, which creates cultural friction that raised operating expenses to roughly $412 million in 2025.

Misalignment between divisions risks service or software-update delays-EquipmentShare reported 14% slower fleet uptime improvements in 2025 when cross-team projects lacked clear owners.

Finding skilled mechanics and software engineers constrains growth; national shortage data show U.S. diesel mechanic vacancies up 8% and software-engineer turnover near 18% in 2025, tightening recruiting costs and time-to-hire.

Brand recognition gap compared to century-old industry leaders

EquipmentShare still trails century-old leaders United Rentals (2025 revenue $14.9B) and Sunbelt (Ahern Rentals part of Ashtead; Ashtead 2025 revenue $8.3B) in brand recognition and institutional ties with large contractors across 50 states.

Closing that gap forces higher marketing and discounting-EquipmentShare's 2025 SG&A rose 22% year-over-year to support expansion, pressuring near-term margins.

Building nationwide institutional trust remains a multi-year task; EquipmentShare had 2025 fleet growth of ~18% but national account penetration lags incumbents.

- Competes with firms >$8B-$15B in revenue

- 2025 SG&A +22% vs. FY2024

- Fleet growth ~18% in 2025

- National account penetration below incumbents

Dependency on third-party OEMs for critical machinery components

EquipmentShare depends on a small set of OEMs for heavy machinery-exposing it to supplier price hikes and the 2025 industry-wide 12% parts lead-time increase that hit US rental fleets.

If a key manufacturer delays production, EquipmentShare's ability to meet rental contracts and planned 2025 fleet growth (target +18% units) is immediately at risk.

This structural lack of control over the primary product raises operational and margin pressure common across rentals; fleet replacement capex was $262M in FY2025.

- Concentrated OEM base → supply disruption risk

- 12% parts lead-time rise in 2025

- FY2025 fleet capex $262M

- Planned unit growth +18% in 2025

High Leverage and CAPEX Turn 28% Growth into Tight Margins: FCF Negative, Interest $280M

EquipmentShare's 2025 leverage (debt/equity ~3.1x) drove $280M interest, cutting net margin to ~2.2% and FCF to -$45M despite 28% revenue growth; heavy fleet CAPEX ($262M-$220M reinvest) and $412M Opex raise capital intensity; supply-chain lead times +12% and concentrated OEMs risk unit growth; SG&A +22% weakens margins vs incumbents.

| Metric | 2025 |

|---|---|

| Debt/Equity | 3.1x |

| Interest Expense | $280M |

| Net Margin | 2.2% |

| FCF | -$45M |

| Revenue Growth | 28% |

| Fleet CAPEX | $262M |

| Reinvestments | $220M |

| Opex | $412M |

| SG&A Δ | +22% |

| Parts Lead-time Δ | +12% |

Preview Before You Purchase

EquipmentShare SWOT Analysis

This is the actual EquipmentShare SWOT analysis document you'll receive upon purchase-no surprises, just professional quality and fully editable for your use.