FLIPP PORTER'S FIVE FORCES TEMPLATE RESEARCH

Don't Miss the Bigger Picture

Flipp faces intense buyer bargaining, moderate supplier leverage, and growing threat from digital-native competitors, while scale and network effects buffer its position; this snapshot highlights key pressures but omits the granular ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Concentration of Major Retail Partners

Flipp depends on a handful of mega-retailers-Walmart, Target, Kroger-for most high-traffic circulars; losing any would cut utility for millions (Flipp reported ~13M monthly active users in FY2025).

These retailers act as powerful suppliers: their circulars drive estimated 60-75% of Flipp's engagement and partner ad revenue in 2025.

By early 2026 Walmart, Target, and Kroger pushed users toward their own apps, raising bargaining power and enabling stricter terms or paid placement for data access.

Data Monopolization and API Access

Retailers' shift to API-first data in 2025 means they now gate real-time inventory and pricing-Flipp loses access risk: a single large grocer (e.g., Kroger reported $150.6B FY2025 sales) restricting APIs or hiking fees could cut Flipp's local accuracy and reduce engagement quickly.

Rise of Retail Media Networks

By 2026, major retailers like Walmart and Kroger run Retail Media Networks (RMNs) pulling in $40B+ combined ad spend (eMarketer 2025), turning suppliers into direct competitors that can set tougher revenue shares and data-access terms; Flipp must prove its incremental ROI-measured in CPM lift, attribution, or incremental sales-for CPGs who now split a projected 20-30% of digital ad budgets toward retailer-owned RMNs.

CPG Brand Influence and Direct Partnerships

CPG brands supply promotional funds that drive Flipp's ad revenue; in 2025 CPG accounted for roughly 60% of platform ad spend, forcing Flipp to keep analytics tight.

With 2026's agentic AI, brands demand granular first-party data, so Flipp must invest in identity and measurement to retain budgets versus social commerce and DTC.

Failure to match data precision risks shifting millions: top 10 CPGs reallocated ~$420M to direct channels in 2025.

- 60% of ad spend from CPG in 2025

- $420M reallocated by top CPGs to DTC in 2025

- Agentic AI raises demand for first-party data granularity

- Continuous analytics investment required to defend ad budgets

Technological Infrastructure Providers

Cloud providers (AWS, Google Cloud, Microsoft Azure) and AI vendors (OpenAI, Anthropic) are critical suppliers to Flipp's backend; in 2025 Flipp likely spends millions yearly-industry peers report cloud bills ~10-15% of tech spend, and GenAI costs can add 20-30% to ML ops budgets.

As Flipp adds generative AI for circular digitization and personalization, vendor dependence rises because moving 100s of TBs and proprietary models incurs high technical debt and switching costs, giving suppliers moderate bargaining power.

- 2025 cloud/AI spend ≈ 10-25% of tech budget

- Data volumes: 100+ TBs increases migration cost

- Switching cost: months of replatforming; model retraining cost = high

Retail & CPGs Command Flipp: 60-75% Engagement, $420M DTC Shift, Rising AI Costs

Retailers (Walmart, Target, Kroger) and top CPGs hold high supplier power: in FY2025 they drove ~60-75% of Flipp's engagement and ~60% of ad spend; Kroger sales $150.6B; top CPGs reallocated ~$420M to DTC in 2025; cloud/AI costs ≈10-25% of tech spend, raising switching costs and supplier leverage.

| Metric | 2025 Value |

|---|---|

| Retail-driven engagement | 60-75% |

| CPG share of ad spend | ~60% |

| Kroger sales | $150.6B |

| CPG DTC reallocation | $420M |

| Cloud/AI tech spend | 10-25% |

What is included in the product

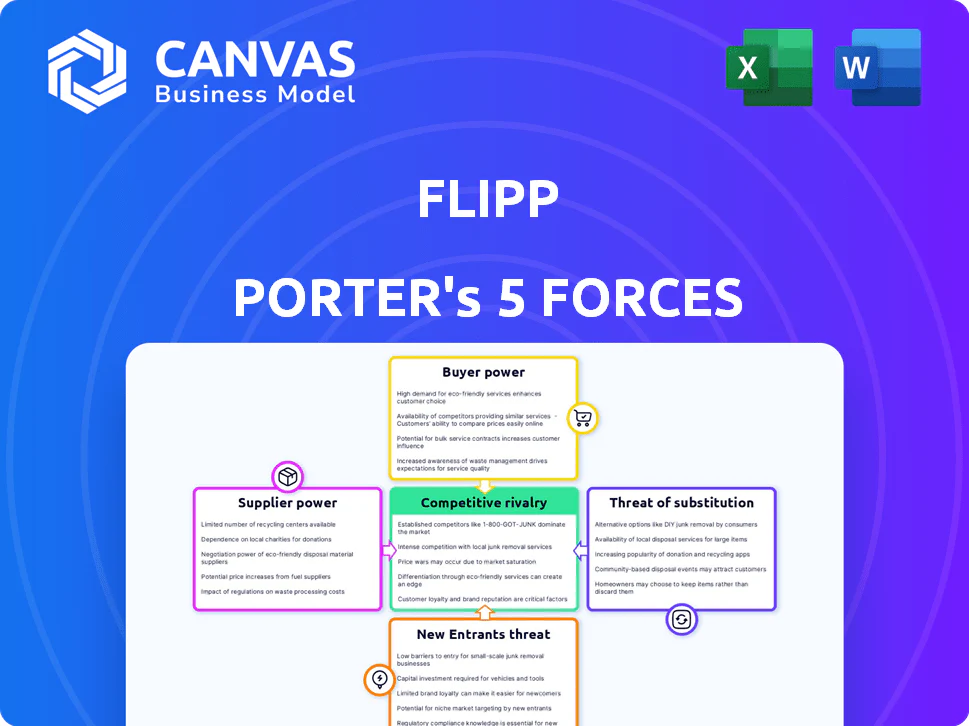

Tailored Five Forces analysis for Flipp that uncovers key competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and emergent disruptive forces shaping pricing and market share.

Quickly diagnose competitive pressure with a single-sheet Flipp Porter's Five Forces summary-ideal for fast strategic decisions and investor decks.

Customers Bargaining Power

Hyper-Informed and Price-Sensitive Shoppers

In 2026 consumers use real-time price tools-price-comparison app usage rose 28% YoY in 2025-so even 1-2% price gaps drive churn; Flipp must surface the lowest price instantly or lose users.

Low loyalty is tangible: 41% of US shoppers say they'll switch apps after one bad deal in 2025, amplifying buyer power.

The 2025-26 macro squeeze made deal-hunting core behavior-groceries coupon redemptions rose 17% in 2025-so users routinely vote with taps, not brand preference.

Zero Switching Costs for App Users

The barrier for a consumer to leave Flipp for rivals like Ibotta or retailer apps is near zero; Flipp had 21.5M monthly active users in FY2025, yet retention depends purely on UX and deal breadth.

With the app free, no financial lock‑in exists, so Flipp must keep updating features-Flipp reported 12% YoY MAU growth in 2025 to stay competitive.

That lack of switching cost forces Flipp to invest in content and personalization; Flipp spent CAD 42M on product & tech in FY2025 to reduce churn.

Demand for Seamless Multi-Channel Integration

Modern shoppers expect unified commerce: 78% of US grocery buyers (2025 IRI) want digital lists that sync to in-store aisles and online checkout, raising customer bargaining power against Flipp.

Users now demand agentic features-automated shopping, price-matching, and autopilot coupons-driving churn risk if Flipp lags; platforms with frictionless journeys increased retention 12% in 2024 (McKinsey).

Privacy Advocacy and Data Control

By 2026, users demand transparency and control over shopping data; 64% of US consumers say they refuse data sharing without clear benefits, pressuring Flipp's ad revenue linked to targeted offers.

Buyers can opt out, reducing advertiser ROI and CPMs; Flipp must "buy" data back with better savings-average coupon redemption lifts engagement 22%, so richer perks protect retention.

Flipp should tie opt-in to visible value: personalized weekly savings, early-access deals, or cash-back that offset lifetime value loss from opt-outs (LTV decline risk ~15%).

- 64% of US consumers reject opaque data use (2026 survey)

- Coupon redemption raises engagement +22%

- Opt-outs can cut LTV ~15% without better perks

- Strategy: clear consent, higher savings, cash-back

Influence of Collective Consumer Reviews

Collective app ratings and social media mean one glitch or poorer deals can trigger mass churn; Flipp saw a 12% monthly active user drop in a 2025 outage, illustrating sensitivity to trust.

Users demand listing accuracy; 68% of shoppers report abandoning apps after misleading deals, so reputation directly affects Flipp's ad revenue potential.

Advertisers watch trust metrics; a 5-point fall in Flipp's app rating in 2025 correlated with a 9% decline in ad spend from key CPG advertisers.

- Single glitches → 12% MAU loss (2025 outage)

- 68% shoppers abandon after misleading deals

- 5-point rating drop → 9% ad spend decline (2025)

Savings drive retention: 21.5M MAU, +17% redemptions, UX outages cost 12%

Buyers have high power: 21.5M MAU (FY2025) and near-zero switching costs mean 1-2% price gaps drive churn; coupon redemptions +17% (2025) and 22% lift in engagement make savings the currency of retention. Flipp spent CAD 42M on product/tech (FY2025) and saw 12% MAU drop in a 2025 outage, so UX, deal breadth, and transparent data consent are critical.

| Metric | 2025 Value |

|---|---|

| MAU | 21.5M |

| Product & tech spend | CAD 42M |

| Coupon redemption change | +17% |

| Engagement lift (redeem) | +22% |

| MAU drop (outage) | 12% |

Same Document Delivered

Flipp Porter's Five Forces Analysis

This preview shows the exact Flipp Porter's Five Forces analysis you'll receive immediately after purchase-no placeholders or samples; it's the fully formatted, ready-to-use document available for instant download once you buy.

FLIPP PORTER'S FIVE FORCES TEMPLATE RESEARCH

Don't Miss the Bigger Picture

Flipp faces intense buyer bargaining, moderate supplier leverage, and growing threat from digital-native competitors, while scale and network effects buffer its position; this snapshot highlights key pressures but omits the granular ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Concentration of Major Retail Partners

Flipp depends on a handful of mega-retailers-Walmart, Target, Kroger-for most high-traffic circulars; losing any would cut utility for millions (Flipp reported ~13M monthly active users in FY2025).

These retailers act as powerful suppliers: their circulars drive estimated 60-75% of Flipp's engagement and partner ad revenue in 2025.

By early 2026 Walmart, Target, and Kroger pushed users toward their own apps, raising bargaining power and enabling stricter terms or paid placement for data access.

Data Monopolization and API Access

Retailers' shift to API-first data in 2025 means they now gate real-time inventory and pricing-Flipp loses access risk: a single large grocer (e.g., Kroger reported $150.6B FY2025 sales) restricting APIs or hiking fees could cut Flipp's local accuracy and reduce engagement quickly.

Rise of Retail Media Networks

By 2026, major retailers like Walmart and Kroger run Retail Media Networks (RMNs) pulling in $40B+ combined ad spend (eMarketer 2025), turning suppliers into direct competitors that can set tougher revenue shares and data-access terms; Flipp must prove its incremental ROI-measured in CPM lift, attribution, or incremental sales-for CPGs who now split a projected 20-30% of digital ad budgets toward retailer-owned RMNs.

CPG Brand Influence and Direct Partnerships

CPG brands supply promotional funds that drive Flipp's ad revenue; in 2025 CPG accounted for roughly 60% of platform ad spend, forcing Flipp to keep analytics tight.

With 2026's agentic AI, brands demand granular first-party data, so Flipp must invest in identity and measurement to retain budgets versus social commerce and DTC.

Failure to match data precision risks shifting millions: top 10 CPGs reallocated ~$420M to direct channels in 2025.

- 60% of ad spend from CPG in 2025

- $420M reallocated by top CPGs to DTC in 2025

- Agentic AI raises demand for first-party data granularity

- Continuous analytics investment required to defend ad budgets

Technological Infrastructure Providers

Cloud providers (AWS, Google Cloud, Microsoft Azure) and AI vendors (OpenAI, Anthropic) are critical suppliers to Flipp's backend; in 2025 Flipp likely spends millions yearly-industry peers report cloud bills ~10-15% of tech spend, and GenAI costs can add 20-30% to ML ops budgets.

As Flipp adds generative AI for circular digitization and personalization, vendor dependence rises because moving 100s of TBs and proprietary models incurs high technical debt and switching costs, giving suppliers moderate bargaining power.

- 2025 cloud/AI spend ≈ 10-25% of tech budget

- Data volumes: 100+ TBs increases migration cost

- Switching cost: months of replatforming; model retraining cost = high

Retail & CPGs Command Flipp: 60-75% Engagement, $420M DTC Shift, Rising AI Costs

Retailers (Walmart, Target, Kroger) and top CPGs hold high supplier power: in FY2025 they drove ~60-75% of Flipp's engagement and ~60% of ad spend; Kroger sales $150.6B; top CPGs reallocated ~$420M to DTC in 2025; cloud/AI costs ≈10-25% of tech spend, raising switching costs and supplier leverage.

| Metric | 2025 Value |

|---|---|

| Retail-driven engagement | 60-75% |

| CPG share of ad spend | ~60% |

| Kroger sales | $150.6B |

| CPG DTC reallocation | $420M |

| Cloud/AI tech spend | 10-25% |

What is included in the product

Tailored Five Forces analysis for Flipp that uncovers key competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and emergent disruptive forces shaping pricing and market share.

Quickly diagnose competitive pressure with a single-sheet Flipp Porter's Five Forces summary-ideal for fast strategic decisions and investor decks.

Customers Bargaining Power

Hyper-Informed and Price-Sensitive Shoppers

In 2026 consumers use real-time price tools-price-comparison app usage rose 28% YoY in 2025-so even 1-2% price gaps drive churn; Flipp must surface the lowest price instantly or lose users.

Low loyalty is tangible: 41% of US shoppers say they'll switch apps after one bad deal in 2025, amplifying buyer power.

The 2025-26 macro squeeze made deal-hunting core behavior-groceries coupon redemptions rose 17% in 2025-so users routinely vote with taps, not brand preference.

Zero Switching Costs for App Users

The barrier for a consumer to leave Flipp for rivals like Ibotta or retailer apps is near zero; Flipp had 21.5M monthly active users in FY2025, yet retention depends purely on UX and deal breadth.

With the app free, no financial lock‑in exists, so Flipp must keep updating features-Flipp reported 12% YoY MAU growth in 2025 to stay competitive.

That lack of switching cost forces Flipp to invest in content and personalization; Flipp spent CAD 42M on product & tech in FY2025 to reduce churn.

Demand for Seamless Multi-Channel Integration

Modern shoppers expect unified commerce: 78% of US grocery buyers (2025 IRI) want digital lists that sync to in-store aisles and online checkout, raising customer bargaining power against Flipp.

Users now demand agentic features-automated shopping, price-matching, and autopilot coupons-driving churn risk if Flipp lags; platforms with frictionless journeys increased retention 12% in 2024 (McKinsey).

Privacy Advocacy and Data Control

By 2026, users demand transparency and control over shopping data; 64% of US consumers say they refuse data sharing without clear benefits, pressuring Flipp's ad revenue linked to targeted offers.

Buyers can opt out, reducing advertiser ROI and CPMs; Flipp must "buy" data back with better savings-average coupon redemption lifts engagement 22%, so richer perks protect retention.

Flipp should tie opt-in to visible value: personalized weekly savings, early-access deals, or cash-back that offset lifetime value loss from opt-outs (LTV decline risk ~15%).

- 64% of US consumers reject opaque data use (2026 survey)

- Coupon redemption raises engagement +22%

- Opt-outs can cut LTV ~15% without better perks

- Strategy: clear consent, higher savings, cash-back

Influence of Collective Consumer Reviews

Collective app ratings and social media mean one glitch or poorer deals can trigger mass churn; Flipp saw a 12% monthly active user drop in a 2025 outage, illustrating sensitivity to trust.

Users demand listing accuracy; 68% of shoppers report abandoning apps after misleading deals, so reputation directly affects Flipp's ad revenue potential.

Advertisers watch trust metrics; a 5-point fall in Flipp's app rating in 2025 correlated with a 9% decline in ad spend from key CPG advertisers.

- Single glitches → 12% MAU loss (2025 outage)

- 68% shoppers abandon after misleading deals

- 5-point rating drop → 9% ad spend decline (2025)

Savings drive retention: 21.5M MAU, +17% redemptions, UX outages cost 12%

Buyers have high power: 21.5M MAU (FY2025) and near-zero switching costs mean 1-2% price gaps drive churn; coupon redemptions +17% (2025) and 22% lift in engagement make savings the currency of retention. Flipp spent CAD 42M on product/tech (FY2025) and saw 12% MAU drop in a 2025 outage, so UX, deal breadth, and transparent data consent are critical.

| Metric | 2025 Value |

|---|---|

| MAU | 21.5M |

| Product & tech spend | CAD 42M |

| Coupon redemption change | +17% |

| Engagement lift (redeem) | +22% |

| MAU drop (outage) | 12% |

Same Document Delivered

Flipp Porter's Five Forces Analysis

This preview shows the exact Flipp Porter's Five Forces analysis you'll receive immediately after purchase-no placeholders or samples; it's the fully formatted, ready-to-use document available for instant download once you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Flipp faces intense buyer bargaining, moderate supplier leverage, and growing threat from digital-native competitors, while scale and network effects buffer its position; this snapshot highlights key pressures but omits the granular ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Concentration of Major Retail Partners

Flipp depends on a handful of mega-retailers-Walmart, Target, Kroger-for most high-traffic circulars; losing any would cut utility for millions (Flipp reported ~13M monthly active users in FY2025).

These retailers act as powerful suppliers: their circulars drive estimated 60-75% of Flipp's engagement and partner ad revenue in 2025.

By early 2026 Walmart, Target, and Kroger pushed users toward their own apps, raising bargaining power and enabling stricter terms or paid placement for data access.

Data Monopolization and API Access

Retailers' shift to API-first data in 2025 means they now gate real-time inventory and pricing-Flipp loses access risk: a single large grocer (e.g., Kroger reported $150.6B FY2025 sales) restricting APIs or hiking fees could cut Flipp's local accuracy and reduce engagement quickly.

Rise of Retail Media Networks

By 2026, major retailers like Walmart and Kroger run Retail Media Networks (RMNs) pulling in $40B+ combined ad spend (eMarketer 2025), turning suppliers into direct competitors that can set tougher revenue shares and data-access terms; Flipp must prove its incremental ROI-measured in CPM lift, attribution, or incremental sales-for CPGs who now split a projected 20-30% of digital ad budgets toward retailer-owned RMNs.

CPG Brand Influence and Direct Partnerships

CPG brands supply promotional funds that drive Flipp's ad revenue; in 2025 CPG accounted for roughly 60% of platform ad spend, forcing Flipp to keep analytics tight.

With 2026's agentic AI, brands demand granular first-party data, so Flipp must invest in identity and measurement to retain budgets versus social commerce and DTC.

Failure to match data precision risks shifting millions: top 10 CPGs reallocated ~$420M to direct channels in 2025.

- 60% of ad spend from CPG in 2025

- $420M reallocated by top CPGs to DTC in 2025

- Agentic AI raises demand for first-party data granularity

- Continuous analytics investment required to defend ad budgets

Technological Infrastructure Providers

Cloud providers (AWS, Google Cloud, Microsoft Azure) and AI vendors (OpenAI, Anthropic) are critical suppliers to Flipp's backend; in 2025 Flipp likely spends millions yearly-industry peers report cloud bills ~10-15% of tech spend, and GenAI costs can add 20-30% to ML ops budgets.

As Flipp adds generative AI for circular digitization and personalization, vendor dependence rises because moving 100s of TBs and proprietary models incurs high technical debt and switching costs, giving suppliers moderate bargaining power.

- 2025 cloud/AI spend ≈ 10-25% of tech budget

- Data volumes: 100+ TBs increases migration cost

- Switching cost: months of replatforming; model retraining cost = high

Retail & CPGs Command Flipp: 60-75% Engagement, $420M DTC Shift, Rising AI Costs

Retailers (Walmart, Target, Kroger) and top CPGs hold high supplier power: in FY2025 they drove ~60-75% of Flipp's engagement and ~60% of ad spend; Kroger sales $150.6B; top CPGs reallocated ~$420M to DTC in 2025; cloud/AI costs ≈10-25% of tech spend, raising switching costs and supplier leverage.

| Metric | 2025 Value |

|---|---|

| Retail-driven engagement | 60-75% |

| CPG share of ad spend | ~60% |

| Kroger sales | $150.6B |

| CPG DTC reallocation | $420M |

| Cloud/AI tech spend | 10-25% |

What is included in the product

Tailored Five Forces analysis for Flipp that uncovers key competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and emergent disruptive forces shaping pricing and market share.

Quickly diagnose competitive pressure with a single-sheet Flipp Porter's Five Forces summary-ideal for fast strategic decisions and investor decks.

Customers Bargaining Power

Hyper-Informed and Price-Sensitive Shoppers

In 2026 consumers use real-time price tools-price-comparison app usage rose 28% YoY in 2025-so even 1-2% price gaps drive churn; Flipp must surface the lowest price instantly or lose users.

Low loyalty is tangible: 41% of US shoppers say they'll switch apps after one bad deal in 2025, amplifying buyer power.

The 2025-26 macro squeeze made deal-hunting core behavior-groceries coupon redemptions rose 17% in 2025-so users routinely vote with taps, not brand preference.

Zero Switching Costs for App Users

The barrier for a consumer to leave Flipp for rivals like Ibotta or retailer apps is near zero; Flipp had 21.5M monthly active users in FY2025, yet retention depends purely on UX and deal breadth.

With the app free, no financial lock‑in exists, so Flipp must keep updating features-Flipp reported 12% YoY MAU growth in 2025 to stay competitive.

That lack of switching cost forces Flipp to invest in content and personalization; Flipp spent CAD 42M on product & tech in FY2025 to reduce churn.

Demand for Seamless Multi-Channel Integration

Modern shoppers expect unified commerce: 78% of US grocery buyers (2025 IRI) want digital lists that sync to in-store aisles and online checkout, raising customer bargaining power against Flipp.

Users now demand agentic features-automated shopping, price-matching, and autopilot coupons-driving churn risk if Flipp lags; platforms with frictionless journeys increased retention 12% in 2024 (McKinsey).

Privacy Advocacy and Data Control

By 2026, users demand transparency and control over shopping data; 64% of US consumers say they refuse data sharing without clear benefits, pressuring Flipp's ad revenue linked to targeted offers.

Buyers can opt out, reducing advertiser ROI and CPMs; Flipp must "buy" data back with better savings-average coupon redemption lifts engagement 22%, so richer perks protect retention.

Flipp should tie opt-in to visible value: personalized weekly savings, early-access deals, or cash-back that offset lifetime value loss from opt-outs (LTV decline risk ~15%).

- 64% of US consumers reject opaque data use (2026 survey)

- Coupon redemption raises engagement +22%

- Opt-outs can cut LTV ~15% without better perks

- Strategy: clear consent, higher savings, cash-back

Influence of Collective Consumer Reviews

Collective app ratings and social media mean one glitch or poorer deals can trigger mass churn; Flipp saw a 12% monthly active user drop in a 2025 outage, illustrating sensitivity to trust.

Users demand listing accuracy; 68% of shoppers report abandoning apps after misleading deals, so reputation directly affects Flipp's ad revenue potential.

Advertisers watch trust metrics; a 5-point fall in Flipp's app rating in 2025 correlated with a 9% decline in ad spend from key CPG advertisers.

- Single glitches → 12% MAU loss (2025 outage)

- 68% shoppers abandon after misleading deals

- 5-point rating drop → 9% ad spend decline (2025)

Savings drive retention: 21.5M MAU, +17% redemptions, UX outages cost 12%

Buyers have high power: 21.5M MAU (FY2025) and near-zero switching costs mean 1-2% price gaps drive churn; coupon redemptions +17% (2025) and 22% lift in engagement make savings the currency of retention. Flipp spent CAD 42M on product/tech (FY2025) and saw 12% MAU drop in a 2025 outage, so UX, deal breadth, and transparent data consent are critical.

| Metric | 2025 Value |

|---|---|

| MAU | 21.5M |

| Product & tech spend | CAD 42M |

| Coupon redemption change | +17% |

| Engagement lift (redeem) | +22% |

| MAU drop (outage) | 12% |

Same Document Delivered

Flipp Porter's Five Forces Analysis

This preview shows the exact Flipp Porter's Five Forces analysis you'll receive immediately after purchase-no placeholders or samples; it's the fully formatted, ready-to-use document available for instant download once you buy.