FULCRUM THERAPEUTICS PORTER'S FIVE FORCES TEMPLATE RESEARCH

What is included in the product

Analyzes Fulcrum's competitive landscape: rivalry, new entrants, suppliers, buyers, and substitutes.

Quickly identify threats and opportunities with a dynamic visual tool.

Preview the Actual Deliverable

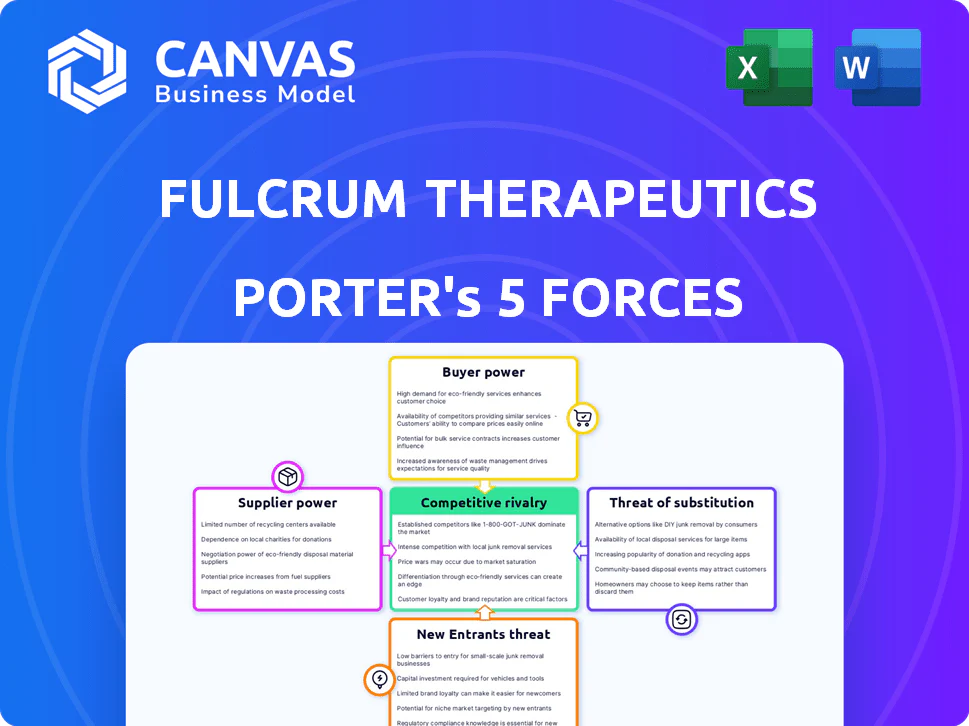

Fulcrum Therapeutics Porter's Five Forces Analysis

This is the complete Fulcrum Therapeutics Porter's Five Forces analysis. The preview showcases the identical document you'll receive immediately upon purchase.

Porter's Five Forces Analysis Template

Don't Miss the Bigger Picture

Fulcrum Therapeutics operates in a biopharmaceutical market shaped by fierce competition and regulatory hurdles.

Buyer power is moderate, with healthcare providers and payers influencing pricing.

Threat of new entrants is high due to the capital-intensive nature of drug development.

Substitute products pose a moderate threat given ongoing research and development.

Supplier power, primarily from research institutions, is also a factor.

Rivalry among competitors is intense, demanding innovation and strategic partnerships.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Fulcrum Therapeutics’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Limited number of specialized suppliers

Fulcrum Therapeutics depends on a specialized supplier network for biotechnology materials. The limited supplier base for high-quality materials strengthens their pricing power. Around 80% of biopharmaceutical manufacturing reagents come from a few suppliers, impacting costs. This concentration allows suppliers to dictate terms more effectively. This dynamic can affect Fulcrum's cost structure.

High switching costs

High switching costs significantly elevate the bargaining power of suppliers for Fulcrum Therapeutics. Changing suppliers, especially for critical raw materials like cell culture media, is expensive. Re-validating manufacturing processes could cost between $250,000 to $1 million per product line.

Suppliers with proprietary technology

Suppliers with proprietary technology in biopharmaceutical manufacturing wield considerable power. They can command premium prices; recent data shows up to 30% more than generics. Fulcrum Therapeutics must manage relationships with these key suppliers. These suppliers hold significant intellectual property, impacting Fulcrum's costs.

Supplier consolidation trends

Consolidation among biopharmaceutical suppliers is reshaping the industry. Mergers and acquisitions among suppliers can reduce competition. This could lead to increased costs for companies like Fulcrum Therapeutics. For example, in 2024, the biopharma supply chain saw significant consolidation, with several key suppliers merging. These trends impact Fulcrum Therapeutics' operational costs and negotiation leverage.

- Supplier consolidation reduces competition.

- This can increase input costs.

- Fulcrum Therapeutics must manage these pressures.

- Negotiating power is essential.

Importance of strong supplier relationships

Fulcrum Therapeutics' ability to negotiate prices hinges on its relationships with suppliers. Strong relationships can lead to favorable pricing, but long-term contracts might create dependencies. Dependence on specific suppliers can make Fulcrum vulnerable to price hikes. This is crucial for cost management.

- Fulcrum's R&D expenses were $109.3 million in 2023, highlighting the importance of cost control.

- The pharmaceutical industry's average cost of goods sold (COGS) is around 30-40% of revenue, impacting profitability.

- Supplier concentration can increase risk; diversification is key to mitigating this.

- Negotiating power is vital to maintain margins, especially with high R&D costs.

Supplier Power Dynamics: A Critical Look

Fulcrum Therapeutics faces supplier power from concentrated markets and high switching costs. Supplier consolidation and proprietary tech further increase their leverage. Strong supplier relationships are crucial for cost management and margin preservation.

| Aspect | Impact | Data |

|---|---|---|

| Concentrated Suppliers | Higher input costs | 80% reagents from few suppliers |

| Switching Costs | Process re-validation | $250K-$1M per product line |

| Negotiation | Key to profitability | R&D expenses in 2023: $109.3M |

Customers Bargaining Power

Customers are primarily large organizations

Fulcrum Therapeutics' key customers consist of large pharmaceutical companies and healthcare organizations. These entities wield considerable bargaining power due to their substantial purchasing volumes. For example, in 2024, the top ten pharmaceutical companies accounted for over 40% of global pharmaceutical sales, indicating their significant influence. This concentration allows them to negotiate favorable terms. This can impact Fulcrum's profitability.

Customer loyalty based on treatment efficacy

Customer loyalty in biotechnology, especially for rare diseases, hinges on treatment efficacy. Fulcrum Therapeutics could see high customer retention if its therapies show significant positive results. In 2024, the biotech industry saw a 15% increase in patient retention rates for successful treatments. Positive outcomes drive customer loyalty, reducing the impact of customer bargaining power.

Government and institutional buyers

Government agencies and institutional buyers, such as hospitals, can significantly affect pricing for Fulcrum Therapeutics. In 2024, government healthcare spending in the US reached approximately $1.9 trillion. These entities often negotiate prices, potentially lowering Fulcrum's revenue. Their influence stems from their substantial purchasing power and impact on reimbursement rates.

Price sensitivity for non-patented drugs

The bargaining power of customers can be significant, particularly concerning price sensitivity for non-patented drugs. Buyers, while valuing quality, often become more price-sensitive when faced with generic or biosimilar alternatives. This situation intensifies if Fulcrum Therapeutics' products lack strong patent protection or unique medical advantages. For instance, in 2024, the generic drug market accounted for approximately 90% of all prescriptions dispensed in the U.S., indicating substantial customer leverage in pricing negotiations.

- Generic drugs represented about 90% of prescriptions in the U.S. in 2024.

- Price competition increases when there are multiple generic drug manufacturers.

- Customers may switch to lower-priced alternatives if the perceived value is similar.

- Patent expiration significantly impacts pricing dynamics.

Regulatory and capital requirements as barriers for customer integration

The pharmaceutical industry's stringent regulations and substantial capital demands erect significant barriers, hindering customer integration into the supply chain, thus curbing their bargaining power. According to the FDA, the average cost to develop a new drug is approximately $2.6 billion, showcasing the capital intensity. These high entry costs restrict customers' ability to exert influence. This situation limits their ability to negotiate favorable terms.

- FDA approval process takes several years, increasing development costs and regulatory hurdles.

- Capital-intensive manufacturing requires significant investment in facilities and equipment.

- Customers lack the financial resources to compete with established pharmaceutical companies.

- Regulatory compliance adds to the complexity and expense, reducing the likelihood of backward integration.

Bargaining Power's Impact on Drug Firm's Profits

Customer bargaining power affects Fulcrum Therapeutics' profitability. Large buyers, like pharmaceutical companies, can negotiate favorable terms, impacting revenue. Price sensitivity is crucial, particularly for non-patented drugs, where generics offer alternatives. However, high industry entry barriers limit customer influence.

| Aspect | Details | 2024 Data |

|---|---|---|

| Generic Drug Market Share | Percentage of prescriptions filled by generics | ~90% in the U.S. |

| R&D Cost | Average cost to develop a new drug | ~$2.6 billion |

| US Gov Healthcare Spending | Government healthcare expenditure | ~$1.9 trillion |

Rivalry Among Competitors

Presence of major pharmaceutical companies

The biotechnology sector, where Fulcrum Therapeutics competes, is dominated by major pharmaceutical companies. These companies have substantial financial resources and deep expertise. This presence significantly increases competition for market share. For instance, in 2024, the top 10 pharmaceutical companies collectively generated over $600 billion in revenue. This financial muscle makes it challenging for smaller firms like Fulcrum to compete.

Competition in rare disease landscape

Fulcrum Therapeutics operates in the competitive rare disease market, targeting genetically defined conditions. This area faces growing rivalry due to the high unmet need, attracting numerous companies. For instance, in 2024, the rare disease therapeutics market was valued at approximately $180 billion, demonstrating substantial growth. This attracts competitors like Vertex and Sarepta, intensifying competition for market share and resources.

Clinical trial outcomes and pipeline progress

Clinical trial outcomes and pipeline advancements significantly shape competitive rivalry. Successful trials and pipeline progression strengthen a company's market stance. For instance, in 2024, positive Phase 3 trial results for a novel drug could substantially boost a company's valuation. Conversely, setbacks can lead to decreased investor confidence and market share erosion. The competitive landscape is constantly shifting, dependent on clinical and pipeline developments.

Development of similar therapeutic approaches

Fulcrum Therapeutics faces intense competition as other firms develop similar therapeutic strategies. Competitors might target the same genetic pathways or diseases, heightening the pressure on Fulcrum's drug candidates. For example, in 2024, several companies are advancing therapies for facioscapulohumeral muscular dystrophy (FSHD), a key area for Fulcrum. This rivalry can slow market entry and reduce potential revenue. The competition includes established pharmaceutical giants and smaller biotech firms.

- Competitors developing FSHD treatments include Novartis and Acceleron Pharma (now part of Bristol Myers Squibb).

- Fulcrum’s primary drug candidate for FSHD is losmapimod.

- Clinical trial timelines and success rates are critical factors in this rivalry.

- The FSHD market is projected to reach significant value in the coming years.

Impact of failed clinical trials

Failed clinical trials can severely damage a company's competitive position. A setback can force a strategic shift, potentially benefiting rivals. For instance, in 2024, approximately 60% of Phase 3 clinical trials for novel drugs failed. This creates opportunities for competitors to advance their products.

- Negative trial results often lead to a 30-50% drop in stock price.

- Competitors with similar drug candidates gain market share.

- Regulatory delays further disadvantage the affected company.

- Investor confidence and future funding become more challenging.

Rare Disease Market's Competitive Battlefield

Competitive rivalry in Fulcrum Therapeutics' market is fierce, driven by major pharmaceutical companies and numerous biotech firms. The rare disease market, valued at $180 billion in 2024, attracts intense competition. Clinical trial outcomes significantly impact market share; for instance, 60% of Phase 3 trials failed in 2024, shifting the competitive landscape.

| Factor | Impact | Example (2024) |

|---|---|---|

| Market Size | Attracts Rivals | Rare disease market: $180B |

| Clinical Trials | Success/Failure | 60% Phase 3 failures |

| Competitors | Direct Pressure | Novartis, Acceleron |

Original: $10.00

-65%$10.00

$3.50FULCRUM THERAPEUTICS PORTER'S FIVE FORCES TEMPLATE RESEARCH

What is included in the product

Analyzes Fulcrum's competitive landscape: rivalry, new entrants, suppliers, buyers, and substitutes.

Quickly identify threats and opportunities with a dynamic visual tool.

Preview the Actual Deliverable

Fulcrum Therapeutics Porter's Five Forces Analysis

This is the complete Fulcrum Therapeutics Porter's Five Forces analysis. The preview showcases the identical document you'll receive immediately upon purchase.

Porter's Five Forces Analysis Template

Don't Miss the Bigger Picture

Fulcrum Therapeutics operates in a biopharmaceutical market shaped by fierce competition and regulatory hurdles.

Buyer power is moderate, with healthcare providers and payers influencing pricing.

Threat of new entrants is high due to the capital-intensive nature of drug development.

Substitute products pose a moderate threat given ongoing research and development.

Supplier power, primarily from research institutions, is also a factor.

Rivalry among competitors is intense, demanding innovation and strategic partnerships.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Fulcrum Therapeutics’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Limited number of specialized suppliers

Fulcrum Therapeutics depends on a specialized supplier network for biotechnology materials. The limited supplier base for high-quality materials strengthens their pricing power. Around 80% of biopharmaceutical manufacturing reagents come from a few suppliers, impacting costs. This concentration allows suppliers to dictate terms more effectively. This dynamic can affect Fulcrum's cost structure.

High switching costs

High switching costs significantly elevate the bargaining power of suppliers for Fulcrum Therapeutics. Changing suppliers, especially for critical raw materials like cell culture media, is expensive. Re-validating manufacturing processes could cost between $250,000 to $1 million per product line.

Suppliers with proprietary technology

Suppliers with proprietary technology in biopharmaceutical manufacturing wield considerable power. They can command premium prices; recent data shows up to 30% more than generics. Fulcrum Therapeutics must manage relationships with these key suppliers. These suppliers hold significant intellectual property, impacting Fulcrum's costs.

Supplier consolidation trends

Consolidation among biopharmaceutical suppliers is reshaping the industry. Mergers and acquisitions among suppliers can reduce competition. This could lead to increased costs for companies like Fulcrum Therapeutics. For example, in 2024, the biopharma supply chain saw significant consolidation, with several key suppliers merging. These trends impact Fulcrum Therapeutics' operational costs and negotiation leverage.

- Supplier consolidation reduces competition.

- This can increase input costs.

- Fulcrum Therapeutics must manage these pressures.

- Negotiating power is essential.

Importance of strong supplier relationships

Fulcrum Therapeutics' ability to negotiate prices hinges on its relationships with suppliers. Strong relationships can lead to favorable pricing, but long-term contracts might create dependencies. Dependence on specific suppliers can make Fulcrum vulnerable to price hikes. This is crucial for cost management.

- Fulcrum's R&D expenses were $109.3 million in 2023, highlighting the importance of cost control.

- The pharmaceutical industry's average cost of goods sold (COGS) is around 30-40% of revenue, impacting profitability.

- Supplier concentration can increase risk; diversification is key to mitigating this.

- Negotiating power is vital to maintain margins, especially with high R&D costs.

Supplier Power Dynamics: A Critical Look

Fulcrum Therapeutics faces supplier power from concentrated markets and high switching costs. Supplier consolidation and proprietary tech further increase their leverage. Strong supplier relationships are crucial for cost management and margin preservation.

| Aspect | Impact | Data |

|---|---|---|

| Concentrated Suppliers | Higher input costs | 80% reagents from few suppliers |

| Switching Costs | Process re-validation | $250K-$1M per product line |

| Negotiation | Key to profitability | R&D expenses in 2023: $109.3M |

Customers Bargaining Power

Customers are primarily large organizations

Fulcrum Therapeutics' key customers consist of large pharmaceutical companies and healthcare organizations. These entities wield considerable bargaining power due to their substantial purchasing volumes. For example, in 2024, the top ten pharmaceutical companies accounted for over 40% of global pharmaceutical sales, indicating their significant influence. This concentration allows them to negotiate favorable terms. This can impact Fulcrum's profitability.

Customer loyalty based on treatment efficacy

Customer loyalty in biotechnology, especially for rare diseases, hinges on treatment efficacy. Fulcrum Therapeutics could see high customer retention if its therapies show significant positive results. In 2024, the biotech industry saw a 15% increase in patient retention rates for successful treatments. Positive outcomes drive customer loyalty, reducing the impact of customer bargaining power.

Government and institutional buyers

Government agencies and institutional buyers, such as hospitals, can significantly affect pricing for Fulcrum Therapeutics. In 2024, government healthcare spending in the US reached approximately $1.9 trillion. These entities often negotiate prices, potentially lowering Fulcrum's revenue. Their influence stems from their substantial purchasing power and impact on reimbursement rates.

Price sensitivity for non-patented drugs

The bargaining power of customers can be significant, particularly concerning price sensitivity for non-patented drugs. Buyers, while valuing quality, often become more price-sensitive when faced with generic or biosimilar alternatives. This situation intensifies if Fulcrum Therapeutics' products lack strong patent protection or unique medical advantages. For instance, in 2024, the generic drug market accounted for approximately 90% of all prescriptions dispensed in the U.S., indicating substantial customer leverage in pricing negotiations.

- Generic drugs represented about 90% of prescriptions in the U.S. in 2024.

- Price competition increases when there are multiple generic drug manufacturers.

- Customers may switch to lower-priced alternatives if the perceived value is similar.

- Patent expiration significantly impacts pricing dynamics.

Regulatory and capital requirements as barriers for customer integration

The pharmaceutical industry's stringent regulations and substantial capital demands erect significant barriers, hindering customer integration into the supply chain, thus curbing their bargaining power. According to the FDA, the average cost to develop a new drug is approximately $2.6 billion, showcasing the capital intensity. These high entry costs restrict customers' ability to exert influence. This situation limits their ability to negotiate favorable terms.

- FDA approval process takes several years, increasing development costs and regulatory hurdles.

- Capital-intensive manufacturing requires significant investment in facilities and equipment.

- Customers lack the financial resources to compete with established pharmaceutical companies.

- Regulatory compliance adds to the complexity and expense, reducing the likelihood of backward integration.

Bargaining Power's Impact on Drug Firm's Profits

Customer bargaining power affects Fulcrum Therapeutics' profitability. Large buyers, like pharmaceutical companies, can negotiate favorable terms, impacting revenue. Price sensitivity is crucial, particularly for non-patented drugs, where generics offer alternatives. However, high industry entry barriers limit customer influence.

| Aspect | Details | 2024 Data |

|---|---|---|

| Generic Drug Market Share | Percentage of prescriptions filled by generics | ~90% in the U.S. |

| R&D Cost | Average cost to develop a new drug | ~$2.6 billion |

| US Gov Healthcare Spending | Government healthcare expenditure | ~$1.9 trillion |

Rivalry Among Competitors

Presence of major pharmaceutical companies

The biotechnology sector, where Fulcrum Therapeutics competes, is dominated by major pharmaceutical companies. These companies have substantial financial resources and deep expertise. This presence significantly increases competition for market share. For instance, in 2024, the top 10 pharmaceutical companies collectively generated over $600 billion in revenue. This financial muscle makes it challenging for smaller firms like Fulcrum to compete.

Competition in rare disease landscape

Fulcrum Therapeutics operates in the competitive rare disease market, targeting genetically defined conditions. This area faces growing rivalry due to the high unmet need, attracting numerous companies. For instance, in 2024, the rare disease therapeutics market was valued at approximately $180 billion, demonstrating substantial growth. This attracts competitors like Vertex and Sarepta, intensifying competition for market share and resources.

Clinical trial outcomes and pipeline progress

Clinical trial outcomes and pipeline advancements significantly shape competitive rivalry. Successful trials and pipeline progression strengthen a company's market stance. For instance, in 2024, positive Phase 3 trial results for a novel drug could substantially boost a company's valuation. Conversely, setbacks can lead to decreased investor confidence and market share erosion. The competitive landscape is constantly shifting, dependent on clinical and pipeline developments.

Development of similar therapeutic approaches

Fulcrum Therapeutics faces intense competition as other firms develop similar therapeutic strategies. Competitors might target the same genetic pathways or diseases, heightening the pressure on Fulcrum's drug candidates. For example, in 2024, several companies are advancing therapies for facioscapulohumeral muscular dystrophy (FSHD), a key area for Fulcrum. This rivalry can slow market entry and reduce potential revenue. The competition includes established pharmaceutical giants and smaller biotech firms.

- Competitors developing FSHD treatments include Novartis and Acceleron Pharma (now part of Bristol Myers Squibb).

- Fulcrum’s primary drug candidate for FSHD is losmapimod.

- Clinical trial timelines and success rates are critical factors in this rivalry.

- The FSHD market is projected to reach significant value in the coming years.

Impact of failed clinical trials

Failed clinical trials can severely damage a company's competitive position. A setback can force a strategic shift, potentially benefiting rivals. For instance, in 2024, approximately 60% of Phase 3 clinical trials for novel drugs failed. This creates opportunities for competitors to advance their products.

- Negative trial results often lead to a 30-50% drop in stock price.

- Competitors with similar drug candidates gain market share.

- Regulatory delays further disadvantage the affected company.

- Investor confidence and future funding become more challenging.

Rare Disease Market's Competitive Battlefield

Competitive rivalry in Fulcrum Therapeutics' market is fierce, driven by major pharmaceutical companies and numerous biotech firms. The rare disease market, valued at $180 billion in 2024, attracts intense competition. Clinical trial outcomes significantly impact market share; for instance, 60% of Phase 3 trials failed in 2024, shifting the competitive landscape.

| Factor | Impact | Example (2024) |

|---|---|---|

| Market Size | Attracts Rivals | Rare disease market: $180B |

| Clinical Trials | Success/Failure | 60% Phase 3 failures |

| Competitors | Direct Pressure | Novartis, Acceleron |

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

What is included in the product

Analyzes Fulcrum's competitive landscape: rivalry, new entrants, suppliers, buyers, and substitutes.

Quickly identify threats and opportunities with a dynamic visual tool.

Preview the Actual Deliverable

Fulcrum Therapeutics Porter's Five Forces Analysis

This is the complete Fulcrum Therapeutics Porter's Five Forces analysis. The preview showcases the identical document you'll receive immediately upon purchase.

Porter's Five Forces Analysis Template

Don't Miss the Bigger Picture

Fulcrum Therapeutics operates in a biopharmaceutical market shaped by fierce competition and regulatory hurdles.

Buyer power is moderate, with healthcare providers and payers influencing pricing.

Threat of new entrants is high due to the capital-intensive nature of drug development.

Substitute products pose a moderate threat given ongoing research and development.

Supplier power, primarily from research institutions, is also a factor.

Rivalry among competitors is intense, demanding innovation and strategic partnerships.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Fulcrum Therapeutics’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Limited number of specialized suppliers

Fulcrum Therapeutics depends on a specialized supplier network for biotechnology materials. The limited supplier base for high-quality materials strengthens their pricing power. Around 80% of biopharmaceutical manufacturing reagents come from a few suppliers, impacting costs. This concentration allows suppliers to dictate terms more effectively. This dynamic can affect Fulcrum's cost structure.

High switching costs

High switching costs significantly elevate the bargaining power of suppliers for Fulcrum Therapeutics. Changing suppliers, especially for critical raw materials like cell culture media, is expensive. Re-validating manufacturing processes could cost between $250,000 to $1 million per product line.

Suppliers with proprietary technology

Suppliers with proprietary technology in biopharmaceutical manufacturing wield considerable power. They can command premium prices; recent data shows up to 30% more than generics. Fulcrum Therapeutics must manage relationships with these key suppliers. These suppliers hold significant intellectual property, impacting Fulcrum's costs.

Supplier consolidation trends

Consolidation among biopharmaceutical suppliers is reshaping the industry. Mergers and acquisitions among suppliers can reduce competition. This could lead to increased costs for companies like Fulcrum Therapeutics. For example, in 2024, the biopharma supply chain saw significant consolidation, with several key suppliers merging. These trends impact Fulcrum Therapeutics' operational costs and negotiation leverage.

- Supplier consolidation reduces competition.

- This can increase input costs.

- Fulcrum Therapeutics must manage these pressures.

- Negotiating power is essential.

Importance of strong supplier relationships

Fulcrum Therapeutics' ability to negotiate prices hinges on its relationships with suppliers. Strong relationships can lead to favorable pricing, but long-term contracts might create dependencies. Dependence on specific suppliers can make Fulcrum vulnerable to price hikes. This is crucial for cost management.

- Fulcrum's R&D expenses were $109.3 million in 2023, highlighting the importance of cost control.

- The pharmaceutical industry's average cost of goods sold (COGS) is around 30-40% of revenue, impacting profitability.

- Supplier concentration can increase risk; diversification is key to mitigating this.

- Negotiating power is vital to maintain margins, especially with high R&D costs.

Supplier Power Dynamics: A Critical Look

Fulcrum Therapeutics faces supplier power from concentrated markets and high switching costs. Supplier consolidation and proprietary tech further increase their leverage. Strong supplier relationships are crucial for cost management and margin preservation.

| Aspect | Impact | Data |

|---|---|---|

| Concentrated Suppliers | Higher input costs | 80% reagents from few suppliers |

| Switching Costs | Process re-validation | $250K-$1M per product line |

| Negotiation | Key to profitability | R&D expenses in 2023: $109.3M |

Customers Bargaining Power

Customers are primarily large organizations

Fulcrum Therapeutics' key customers consist of large pharmaceutical companies and healthcare organizations. These entities wield considerable bargaining power due to their substantial purchasing volumes. For example, in 2024, the top ten pharmaceutical companies accounted for over 40% of global pharmaceutical sales, indicating their significant influence. This concentration allows them to negotiate favorable terms. This can impact Fulcrum's profitability.

Customer loyalty based on treatment efficacy

Customer loyalty in biotechnology, especially for rare diseases, hinges on treatment efficacy. Fulcrum Therapeutics could see high customer retention if its therapies show significant positive results. In 2024, the biotech industry saw a 15% increase in patient retention rates for successful treatments. Positive outcomes drive customer loyalty, reducing the impact of customer bargaining power.

Government and institutional buyers

Government agencies and institutional buyers, such as hospitals, can significantly affect pricing for Fulcrum Therapeutics. In 2024, government healthcare spending in the US reached approximately $1.9 trillion. These entities often negotiate prices, potentially lowering Fulcrum's revenue. Their influence stems from their substantial purchasing power and impact on reimbursement rates.

Price sensitivity for non-patented drugs

The bargaining power of customers can be significant, particularly concerning price sensitivity for non-patented drugs. Buyers, while valuing quality, often become more price-sensitive when faced with generic or biosimilar alternatives. This situation intensifies if Fulcrum Therapeutics' products lack strong patent protection or unique medical advantages. For instance, in 2024, the generic drug market accounted for approximately 90% of all prescriptions dispensed in the U.S., indicating substantial customer leverage in pricing negotiations.

- Generic drugs represented about 90% of prescriptions in the U.S. in 2024.

- Price competition increases when there are multiple generic drug manufacturers.

- Customers may switch to lower-priced alternatives if the perceived value is similar.

- Patent expiration significantly impacts pricing dynamics.

Regulatory and capital requirements as barriers for customer integration

The pharmaceutical industry's stringent regulations and substantial capital demands erect significant barriers, hindering customer integration into the supply chain, thus curbing their bargaining power. According to the FDA, the average cost to develop a new drug is approximately $2.6 billion, showcasing the capital intensity. These high entry costs restrict customers' ability to exert influence. This situation limits their ability to negotiate favorable terms.

- FDA approval process takes several years, increasing development costs and regulatory hurdles.

- Capital-intensive manufacturing requires significant investment in facilities and equipment.

- Customers lack the financial resources to compete with established pharmaceutical companies.

- Regulatory compliance adds to the complexity and expense, reducing the likelihood of backward integration.

Bargaining Power's Impact on Drug Firm's Profits

Customer bargaining power affects Fulcrum Therapeutics' profitability. Large buyers, like pharmaceutical companies, can negotiate favorable terms, impacting revenue. Price sensitivity is crucial, particularly for non-patented drugs, where generics offer alternatives. However, high industry entry barriers limit customer influence.

| Aspect | Details | 2024 Data |

|---|---|---|

| Generic Drug Market Share | Percentage of prescriptions filled by generics | ~90% in the U.S. |

| R&D Cost | Average cost to develop a new drug | ~$2.6 billion |

| US Gov Healthcare Spending | Government healthcare expenditure | ~$1.9 trillion |

Rivalry Among Competitors

Presence of major pharmaceutical companies

The biotechnology sector, where Fulcrum Therapeutics competes, is dominated by major pharmaceutical companies. These companies have substantial financial resources and deep expertise. This presence significantly increases competition for market share. For instance, in 2024, the top 10 pharmaceutical companies collectively generated over $600 billion in revenue. This financial muscle makes it challenging for smaller firms like Fulcrum to compete.

Competition in rare disease landscape

Fulcrum Therapeutics operates in the competitive rare disease market, targeting genetically defined conditions. This area faces growing rivalry due to the high unmet need, attracting numerous companies. For instance, in 2024, the rare disease therapeutics market was valued at approximately $180 billion, demonstrating substantial growth. This attracts competitors like Vertex and Sarepta, intensifying competition for market share and resources.

Clinical trial outcomes and pipeline progress

Clinical trial outcomes and pipeline advancements significantly shape competitive rivalry. Successful trials and pipeline progression strengthen a company's market stance. For instance, in 2024, positive Phase 3 trial results for a novel drug could substantially boost a company's valuation. Conversely, setbacks can lead to decreased investor confidence and market share erosion. The competitive landscape is constantly shifting, dependent on clinical and pipeline developments.

Development of similar therapeutic approaches

Fulcrum Therapeutics faces intense competition as other firms develop similar therapeutic strategies. Competitors might target the same genetic pathways or diseases, heightening the pressure on Fulcrum's drug candidates. For example, in 2024, several companies are advancing therapies for facioscapulohumeral muscular dystrophy (FSHD), a key area for Fulcrum. This rivalry can slow market entry and reduce potential revenue. The competition includes established pharmaceutical giants and smaller biotech firms.

- Competitors developing FSHD treatments include Novartis and Acceleron Pharma (now part of Bristol Myers Squibb).

- Fulcrum’s primary drug candidate for FSHD is losmapimod.

- Clinical trial timelines and success rates are critical factors in this rivalry.

- The FSHD market is projected to reach significant value in the coming years.

Impact of failed clinical trials

Failed clinical trials can severely damage a company's competitive position. A setback can force a strategic shift, potentially benefiting rivals. For instance, in 2024, approximately 60% of Phase 3 clinical trials for novel drugs failed. This creates opportunities for competitors to advance their products.

- Negative trial results often lead to a 30-50% drop in stock price.

- Competitors with similar drug candidates gain market share.

- Regulatory delays further disadvantage the affected company.

- Investor confidence and future funding become more challenging.

Rare Disease Market's Competitive Battlefield

Competitive rivalry in Fulcrum Therapeutics' market is fierce, driven by major pharmaceutical companies and numerous biotech firms. The rare disease market, valued at $180 billion in 2024, attracts intense competition. Clinical trial outcomes significantly impact market share; for instance, 60% of Phase 3 trials failed in 2024, shifting the competitive landscape.

| Factor | Impact | Example (2024) |

|---|---|---|

| Market Size | Attracts Rivals | Rare disease market: $180B |

| Clinical Trials | Success/Failure | 60% Phase 3 failures |

| Competitors | Direct Pressure | Novartis, Acceleron |