G7 NETWORKS PORTER'S FIVE FORCES TEMPLATE RESEARCH

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to G7 Networks.

Swap in your own data and labels to reflect current business conditions.

Full Version Awaits

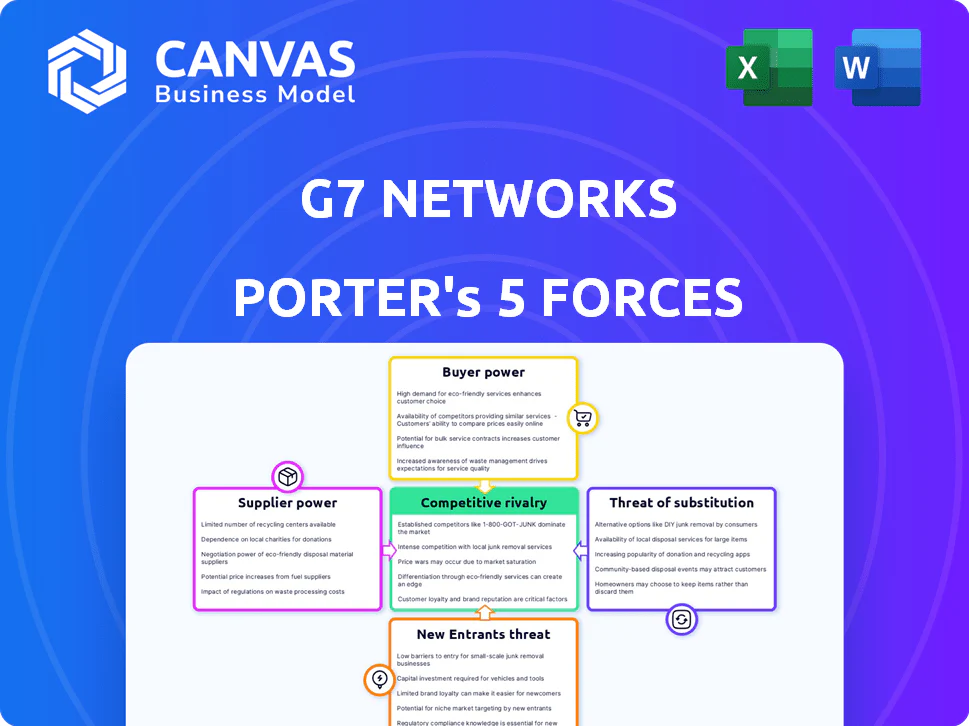

G7 Networks Porter's Five Forces Analysis

This preview displays the comprehensive G7 Networks Porter's Five Forces analysis document. The document you're seeing is the exact, fully-formatted analysis you'll receive after purchasing. It includes detailed insights into each force affecting G7 Networks. You'll gain immediate access to this ready-to-use analysis. There are no alterations to be made.

Porter's Five Forces Analysis Template

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

G7 Networks operates in a dynamic telecommunications market. Buyer power is moderate, influenced by contract negotiations. Threat of new entrants is significant, with technological barriers a key factor. Competitive rivalry is intense, driven by industry consolidation. Substitute products pose a moderate threat, evolving with tech. Supplier power is somewhat concentrated, impacting costs.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore G7 Networks’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Hardware Manufacturers

G7 Networks depends on suppliers for IoT hardware like GPS trackers. The bargaining power of these suppliers can be high if there are few providers. This impacts G7's costs and solution availability. For example, in 2024, the global IoT market was valued at over $200 billion, highlighting supplier influence.

Software and Platform Providers

G7 Networks, while having its platform, relies on third-party software, cloud, and data tools. Suppliers' power hinges on offering uniqueness and criticality, plus how easy it is to switch. In 2024, cloud services like AWS and Azure held substantial market share, impacting G7's costs and flexibility. Switching costs can be high, especially for complex integrations, increasing suppliers' leverage.

Connectivity Providers

G7 Networks relies on connectivity providers for its solutions, such as cellular and satellite services. The bargaining power of these providers, including major players like Verizon and AT&T, impacts G7's costs. For example, in 2024, the average cost of a cellular data plan in the US was around $50 per month, affecting G7's operational expenses. Limited provider options in certain areas further increase their leverage.

Data and Analytics Tools

G7 Networks utilizes data analytics and potentially AI. Suppliers of critical technologies, like advanced analytics software or unique datasets, could have considerable bargaining power. If these resources are vital to G7's services and not easily replaceable, suppliers gain leverage. This is especially true in the rapidly evolving tech landscape.

- The global market for data analytics is projected to reach $300 billion by the end of 2024.

- AI software spending is expected to hit $150 billion in 2024.

- Companies with proprietary AI algorithms often command premium pricing.

- The availability of specialized datasets significantly impacts supplier power.

Talent Pool

For G7 Networks, the bargaining power of suppliers, specifically the talent pool, is crucial. As a tech firm, its reliance on skilled engineers and developers is paramount. The limited availability of experts in IoT, AI, and logistics tech elevates the influence of potential and current employees. This impacts labor costs and innovation potential, especially in a competitive market. The average salary for AI engineers in 2024 reached $160,000.

- Scarcity of specialized skills drives up labor costs.

- Competition for talent can impede innovation.

- Employee influence affects project timelines.

- G7 needs to invest in talent retention strategies.

G7's Supplier Power: Costs, Availability, and Flexibility

G7 Networks faces supplier bargaining power across hardware, software, and connectivity. Key suppliers include IoT hardware providers, cloud services, and data analytics firms. Supplier power is amplified by scarcity and high switching costs, impacting G7's costs and operational flexibility.

| Supplier Type | Impact on G7 | 2024 Data Point |

|---|---|---|

| IoT Hardware | Cost and availability | Global IoT market > $200B |

| Cloud Services | Cost and flexibility | AWS/Azure market share |

| Connectivity | Operational expenses | US cell plan avg $50/month |

Customers Bargaining Power

Large Logistics Companies as Key Customers

G7 Networks' smart fleet focus targets large logistics companies, making them key customers. These customers, managing extensive fleets, wield substantial bargaining power. In 2024, the logistics sector saw a 6.2% revenue increase, highlighting customer influence. Large customers can threaten in-house development or switch to rivals, impacting G7's pricing and service terms.

Customer Concentration

Customer concentration significantly impacts G7's bargaining power. If a few major clients generate most revenue, their leverage increases. These key customers can demand lower prices or better terms. For example, if 60% of G7's sales come from three clients, profitability could be pressured.

Availability of Alternatives

Customers of G7 Networks have multiple fleet management choices, including competitors and traditional methods. The availability of alternatives, like those from Samsara or Geotab, gives customers leverage. This ease of switching limits G7's pricing power. In 2024, the global fleet management market was valued at approximately $28 billion, showing strong competition.

Customer's Cost Sensitivity

Logistics companies, operating on tight margins, are very cost-sensitive. They pressure G7 for affordable solutions, expecting a clear return on investment. This includes fuel savings and optimized routes. In 2024, fuel costs were a major concern, with diesel prices fluctuating significantly, impacting profitability.

- Fuel costs account for a significant portion of operational expenses, often exceeding 30%.

- Optimized routes can lead to 10-15% fuel savings.

- Efficiency improvements are critical for maintaining profitability.

- Companies are increasingly negotiating aggressively for better rates.

Demand for Customized Solutions

The bargaining power of customers in the logistics sector varies significantly. Customers, especially those needing custom solutions, can exert considerable influence. They often have specific demands based on their size, fleet type, and operational complexity, potentially requiring G7 to be flexible. This can involve tailored development investments.

- 2024 saw a rise in demand for customized logistics solutions, with a 15% increase in requests.

- Companies with complex supply chains often have more bargaining power.

- G7 might need to allocate up to 10% of its R&D budget to meet these specific customer needs.

- Flexibility in pricing and service offerings is critical to retain these clients.

G7's Bargaining Power: Customer Leverage & Market Dynamics

G7 Networks faces strong customer bargaining power due to its focus on large logistics clients and the availability of alternatives like Samsara and Geotab. In 2024, the fleet management market was about $28 billion, intensifying competition. Logistics companies' cost sensitivity, with fuel often over 30% of expenses, further amplifies their influence.

| Factor | Impact | 2024 Data |

|---|---|---|

| Customer Concentration | High concentration increases leverage | 60% of sales from 3 clients |

| Market Alternatives | Many choices limit pricing power | $28B global fleet market |

| Cost Sensitivity | Pressure for affordable solutions | Fuel costs >30% of expenses |

Rivalry Among Competitors

Numerous Competitors in the IoT Fleet Management Market

The IoT fleet management market is highly competitive. G7 Networks contends with established telematics firms and tech companies. Market analysis from 2024 shows significant competition. The global fleet management market was valued at $27.9 billion in 2024, highlighting the vast number of players.

Presence of Large Global Players

Major tech and automotive giants are increasingly involved in connected vehicles and fleet management, significantly impacting competition. Companies like Google and Tesla are investing heavily, leveraging their resources and brand power. For instance, Tesla's market cap in early 2024 was around $600 billion, underscoring its financial muscle. This influx creates tougher competition.

Price-Based Competition

Price-based competition is a key factor in the competitive rivalry for G7 Networks. The similarity in service offerings can lead to price wars. For instance, in 2024, the average revenue per user (ARPU) in the telecom sector saw a 3% decrease due to pricing pressures. G7's profit margins could be squeezed if they lower prices to compete.

Rapid Technological Advancements

The IoT and fleet management sectors see rapid tech shifts. Competitors like Samsara and Geotab constantly innovate, boosting features and platforms. G7 Networks must invest significantly in R&D to keep pace. In 2024, the global fleet management market was valued at $28.7 billion. Continuous innovation is a must.

- AI and data analytics are key drivers.

- Connectivity advancements are crucial.

- Competitors are always improving.

- R&D investment is vital for G7.

Market Growth Attracts New Competitors

The expanding global IoT fleet management market, expected to be worth billions in the coming years, draws in new competitors and investment. This growth increases rivalry as companies compete for market share. For example, the global fleet management market was valued at $24.52 billion in 2023. The market is projected to reach $53.07 billion by 2029.

- Market growth attracts new entrants.

- Increased competition intensifies rivalry.

- More players fight for market share.

- Investment and innovation are stimulated.

IoT Fleet Management: Navigating the Competitive Landscape

Competitive rivalry in the IoT fleet management market is intense, fueled by numerous players and rapid tech advancements. G7 Networks faces pressure from established firms and tech giants like Tesla, which had a market cap of around $600 billion in early 2024. Price competition and continuous innovation, with the global market valued at $28.7 billion in 2024, are significant challenges for G7.

| Aspect | Details | Impact on G7 |

|---|---|---|

| Competitors | Established telematics firms, tech giants (Tesla, Google). | Increased competition; need for differentiation. |

| Price Competition | Similarity in service offerings leads to price wars; ARPU decreased 3% in telecom in 2024. | Squeezed profit margins. |

| Innovation | Rapid tech shifts; AI, data analytics, connectivity advancements. | High R&D investment is vital to keep up. |

G7 NETWORKS PORTER'S FIVE FORCES TEMPLATE RESEARCH

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to G7 Networks.

Swap in your own data and labels to reflect current business conditions.

Full Version Awaits

G7 Networks Porter's Five Forces Analysis

This preview displays the comprehensive G7 Networks Porter's Five Forces analysis document. The document you're seeing is the exact, fully-formatted analysis you'll receive after purchasing. It includes detailed insights into each force affecting G7 Networks. You'll gain immediate access to this ready-to-use analysis. There are no alterations to be made.

Porter's Five Forces Analysis Template

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

G7 Networks operates in a dynamic telecommunications market. Buyer power is moderate, influenced by contract negotiations. Threat of new entrants is significant, with technological barriers a key factor. Competitive rivalry is intense, driven by industry consolidation. Substitute products pose a moderate threat, evolving with tech. Supplier power is somewhat concentrated, impacting costs.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore G7 Networks’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Hardware Manufacturers

G7 Networks depends on suppliers for IoT hardware like GPS trackers. The bargaining power of these suppliers can be high if there are few providers. This impacts G7's costs and solution availability. For example, in 2024, the global IoT market was valued at over $200 billion, highlighting supplier influence.

Software and Platform Providers

G7 Networks, while having its platform, relies on third-party software, cloud, and data tools. Suppliers' power hinges on offering uniqueness and criticality, plus how easy it is to switch. In 2024, cloud services like AWS and Azure held substantial market share, impacting G7's costs and flexibility. Switching costs can be high, especially for complex integrations, increasing suppliers' leverage.

Connectivity Providers

G7 Networks relies on connectivity providers for its solutions, such as cellular and satellite services. The bargaining power of these providers, including major players like Verizon and AT&T, impacts G7's costs. For example, in 2024, the average cost of a cellular data plan in the US was around $50 per month, affecting G7's operational expenses. Limited provider options in certain areas further increase their leverage.

Data and Analytics Tools

G7 Networks utilizes data analytics and potentially AI. Suppliers of critical technologies, like advanced analytics software or unique datasets, could have considerable bargaining power. If these resources are vital to G7's services and not easily replaceable, suppliers gain leverage. This is especially true in the rapidly evolving tech landscape.

- The global market for data analytics is projected to reach $300 billion by the end of 2024.

- AI software spending is expected to hit $150 billion in 2024.

- Companies with proprietary AI algorithms often command premium pricing.

- The availability of specialized datasets significantly impacts supplier power.

Talent Pool

For G7 Networks, the bargaining power of suppliers, specifically the talent pool, is crucial. As a tech firm, its reliance on skilled engineers and developers is paramount. The limited availability of experts in IoT, AI, and logistics tech elevates the influence of potential and current employees. This impacts labor costs and innovation potential, especially in a competitive market. The average salary for AI engineers in 2024 reached $160,000.

- Scarcity of specialized skills drives up labor costs.

- Competition for talent can impede innovation.

- Employee influence affects project timelines.

- G7 needs to invest in talent retention strategies.

G7's Supplier Power: Costs, Availability, and Flexibility

G7 Networks faces supplier bargaining power across hardware, software, and connectivity. Key suppliers include IoT hardware providers, cloud services, and data analytics firms. Supplier power is amplified by scarcity and high switching costs, impacting G7's costs and operational flexibility.

| Supplier Type | Impact on G7 | 2024 Data Point |

|---|---|---|

| IoT Hardware | Cost and availability | Global IoT market > $200B |

| Cloud Services | Cost and flexibility | AWS/Azure market share |

| Connectivity | Operational expenses | US cell plan avg $50/month |

Customers Bargaining Power

Large Logistics Companies as Key Customers

G7 Networks' smart fleet focus targets large logistics companies, making them key customers. These customers, managing extensive fleets, wield substantial bargaining power. In 2024, the logistics sector saw a 6.2% revenue increase, highlighting customer influence. Large customers can threaten in-house development or switch to rivals, impacting G7's pricing and service terms.

Customer Concentration

Customer concentration significantly impacts G7's bargaining power. If a few major clients generate most revenue, their leverage increases. These key customers can demand lower prices or better terms. For example, if 60% of G7's sales come from three clients, profitability could be pressured.

Availability of Alternatives

Customers of G7 Networks have multiple fleet management choices, including competitors and traditional methods. The availability of alternatives, like those from Samsara or Geotab, gives customers leverage. This ease of switching limits G7's pricing power. In 2024, the global fleet management market was valued at approximately $28 billion, showing strong competition.

Customer's Cost Sensitivity

Logistics companies, operating on tight margins, are very cost-sensitive. They pressure G7 for affordable solutions, expecting a clear return on investment. This includes fuel savings and optimized routes. In 2024, fuel costs were a major concern, with diesel prices fluctuating significantly, impacting profitability.

- Fuel costs account for a significant portion of operational expenses, often exceeding 30%.

- Optimized routes can lead to 10-15% fuel savings.

- Efficiency improvements are critical for maintaining profitability.

- Companies are increasingly negotiating aggressively for better rates.

Demand for Customized Solutions

The bargaining power of customers in the logistics sector varies significantly. Customers, especially those needing custom solutions, can exert considerable influence. They often have specific demands based on their size, fleet type, and operational complexity, potentially requiring G7 to be flexible. This can involve tailored development investments.

- 2024 saw a rise in demand for customized logistics solutions, with a 15% increase in requests.

- Companies with complex supply chains often have more bargaining power.

- G7 might need to allocate up to 10% of its R&D budget to meet these specific customer needs.

- Flexibility in pricing and service offerings is critical to retain these clients.

G7's Bargaining Power: Customer Leverage & Market Dynamics

G7 Networks faces strong customer bargaining power due to its focus on large logistics clients and the availability of alternatives like Samsara and Geotab. In 2024, the fleet management market was about $28 billion, intensifying competition. Logistics companies' cost sensitivity, with fuel often over 30% of expenses, further amplifies their influence.

| Factor | Impact | 2024 Data |

|---|---|---|

| Customer Concentration | High concentration increases leverage | 60% of sales from 3 clients |

| Market Alternatives | Many choices limit pricing power | $28B global fleet market |

| Cost Sensitivity | Pressure for affordable solutions | Fuel costs >30% of expenses |

Rivalry Among Competitors

Numerous Competitors in the IoT Fleet Management Market

The IoT fleet management market is highly competitive. G7 Networks contends with established telematics firms and tech companies. Market analysis from 2024 shows significant competition. The global fleet management market was valued at $27.9 billion in 2024, highlighting the vast number of players.

Presence of Large Global Players

Major tech and automotive giants are increasingly involved in connected vehicles and fleet management, significantly impacting competition. Companies like Google and Tesla are investing heavily, leveraging their resources and brand power. For instance, Tesla's market cap in early 2024 was around $600 billion, underscoring its financial muscle. This influx creates tougher competition.

Price-Based Competition

Price-based competition is a key factor in the competitive rivalry for G7 Networks. The similarity in service offerings can lead to price wars. For instance, in 2024, the average revenue per user (ARPU) in the telecom sector saw a 3% decrease due to pricing pressures. G7's profit margins could be squeezed if they lower prices to compete.

Rapid Technological Advancements

The IoT and fleet management sectors see rapid tech shifts. Competitors like Samsara and Geotab constantly innovate, boosting features and platforms. G7 Networks must invest significantly in R&D to keep pace. In 2024, the global fleet management market was valued at $28.7 billion. Continuous innovation is a must.

- AI and data analytics are key drivers.

- Connectivity advancements are crucial.

- Competitors are always improving.

- R&D investment is vital for G7.

Market Growth Attracts New Competitors

The expanding global IoT fleet management market, expected to be worth billions in the coming years, draws in new competitors and investment. This growth increases rivalry as companies compete for market share. For example, the global fleet management market was valued at $24.52 billion in 2023. The market is projected to reach $53.07 billion by 2029.

- Market growth attracts new entrants.

- Increased competition intensifies rivalry.

- More players fight for market share.

- Investment and innovation are stimulated.

IoT Fleet Management: Navigating the Competitive Landscape

Competitive rivalry in the IoT fleet management market is intense, fueled by numerous players and rapid tech advancements. G7 Networks faces pressure from established firms and tech giants like Tesla, which had a market cap of around $600 billion in early 2024. Price competition and continuous innovation, with the global market valued at $28.7 billion in 2024, are significant challenges for G7.

| Aspect | Details | Impact on G7 |

|---|---|---|

| Competitors | Established telematics firms, tech giants (Tesla, Google). | Increased competition; need for differentiation. |

| Price Competition | Similarity in service offerings leads to price wars; ARPU decreased 3% in telecom in 2024. | Squeezed profit margins. |

| Innovation | Rapid tech shifts; AI, data analytics, connectivity advancements. | High R&D investment is vital to keep up. |

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to G7 Networks.

Swap in your own data and labels to reflect current business conditions.

Full Version Awaits

G7 Networks Porter's Five Forces Analysis

This preview displays the comprehensive G7 Networks Porter's Five Forces analysis document. The document you're seeing is the exact, fully-formatted analysis you'll receive after purchasing. It includes detailed insights into each force affecting G7 Networks. You'll gain immediate access to this ready-to-use analysis. There are no alterations to be made.

Porter's Five Forces Analysis Template

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

G7 Networks operates in a dynamic telecommunications market. Buyer power is moderate, influenced by contract negotiations. Threat of new entrants is significant, with technological barriers a key factor. Competitive rivalry is intense, driven by industry consolidation. Substitute products pose a moderate threat, evolving with tech. Supplier power is somewhat concentrated, impacting costs.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore G7 Networks’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Hardware Manufacturers

G7 Networks depends on suppliers for IoT hardware like GPS trackers. The bargaining power of these suppliers can be high if there are few providers. This impacts G7's costs and solution availability. For example, in 2024, the global IoT market was valued at over $200 billion, highlighting supplier influence.

Software and Platform Providers

G7 Networks, while having its platform, relies on third-party software, cloud, and data tools. Suppliers' power hinges on offering uniqueness and criticality, plus how easy it is to switch. In 2024, cloud services like AWS and Azure held substantial market share, impacting G7's costs and flexibility. Switching costs can be high, especially for complex integrations, increasing suppliers' leverage.

Connectivity Providers

G7 Networks relies on connectivity providers for its solutions, such as cellular and satellite services. The bargaining power of these providers, including major players like Verizon and AT&T, impacts G7's costs. For example, in 2024, the average cost of a cellular data plan in the US was around $50 per month, affecting G7's operational expenses. Limited provider options in certain areas further increase their leverage.

Data and Analytics Tools

G7 Networks utilizes data analytics and potentially AI. Suppliers of critical technologies, like advanced analytics software or unique datasets, could have considerable bargaining power. If these resources are vital to G7's services and not easily replaceable, suppliers gain leverage. This is especially true in the rapidly evolving tech landscape.

- The global market for data analytics is projected to reach $300 billion by the end of 2024.

- AI software spending is expected to hit $150 billion in 2024.

- Companies with proprietary AI algorithms often command premium pricing.

- The availability of specialized datasets significantly impacts supplier power.

Talent Pool

For G7 Networks, the bargaining power of suppliers, specifically the talent pool, is crucial. As a tech firm, its reliance on skilled engineers and developers is paramount. The limited availability of experts in IoT, AI, and logistics tech elevates the influence of potential and current employees. This impacts labor costs and innovation potential, especially in a competitive market. The average salary for AI engineers in 2024 reached $160,000.

- Scarcity of specialized skills drives up labor costs.

- Competition for talent can impede innovation.

- Employee influence affects project timelines.

- G7 needs to invest in talent retention strategies.

G7's Supplier Power: Costs, Availability, and Flexibility

G7 Networks faces supplier bargaining power across hardware, software, and connectivity. Key suppliers include IoT hardware providers, cloud services, and data analytics firms. Supplier power is amplified by scarcity and high switching costs, impacting G7's costs and operational flexibility.

| Supplier Type | Impact on G7 | 2024 Data Point |

|---|---|---|

| IoT Hardware | Cost and availability | Global IoT market > $200B |

| Cloud Services | Cost and flexibility | AWS/Azure market share |

| Connectivity | Operational expenses | US cell plan avg $50/month |

Customers Bargaining Power

Large Logistics Companies as Key Customers

G7 Networks' smart fleet focus targets large logistics companies, making them key customers. These customers, managing extensive fleets, wield substantial bargaining power. In 2024, the logistics sector saw a 6.2% revenue increase, highlighting customer influence. Large customers can threaten in-house development or switch to rivals, impacting G7's pricing and service terms.

Customer Concentration

Customer concentration significantly impacts G7's bargaining power. If a few major clients generate most revenue, their leverage increases. These key customers can demand lower prices or better terms. For example, if 60% of G7's sales come from three clients, profitability could be pressured.

Availability of Alternatives

Customers of G7 Networks have multiple fleet management choices, including competitors and traditional methods. The availability of alternatives, like those from Samsara or Geotab, gives customers leverage. This ease of switching limits G7's pricing power. In 2024, the global fleet management market was valued at approximately $28 billion, showing strong competition.

Customer's Cost Sensitivity

Logistics companies, operating on tight margins, are very cost-sensitive. They pressure G7 for affordable solutions, expecting a clear return on investment. This includes fuel savings and optimized routes. In 2024, fuel costs were a major concern, with diesel prices fluctuating significantly, impacting profitability.

- Fuel costs account for a significant portion of operational expenses, often exceeding 30%.

- Optimized routes can lead to 10-15% fuel savings.

- Efficiency improvements are critical for maintaining profitability.

- Companies are increasingly negotiating aggressively for better rates.

Demand for Customized Solutions

The bargaining power of customers in the logistics sector varies significantly. Customers, especially those needing custom solutions, can exert considerable influence. They often have specific demands based on their size, fleet type, and operational complexity, potentially requiring G7 to be flexible. This can involve tailored development investments.

- 2024 saw a rise in demand for customized logistics solutions, with a 15% increase in requests.

- Companies with complex supply chains often have more bargaining power.

- G7 might need to allocate up to 10% of its R&D budget to meet these specific customer needs.

- Flexibility in pricing and service offerings is critical to retain these clients.

G7's Bargaining Power: Customer Leverage & Market Dynamics

G7 Networks faces strong customer bargaining power due to its focus on large logistics clients and the availability of alternatives like Samsara and Geotab. In 2024, the fleet management market was about $28 billion, intensifying competition. Logistics companies' cost sensitivity, with fuel often over 30% of expenses, further amplifies their influence.

| Factor | Impact | 2024 Data |

|---|---|---|

| Customer Concentration | High concentration increases leverage | 60% of sales from 3 clients |

| Market Alternatives | Many choices limit pricing power | $28B global fleet market |

| Cost Sensitivity | Pressure for affordable solutions | Fuel costs >30% of expenses |

Rivalry Among Competitors

Numerous Competitors in the IoT Fleet Management Market

The IoT fleet management market is highly competitive. G7 Networks contends with established telematics firms and tech companies. Market analysis from 2024 shows significant competition. The global fleet management market was valued at $27.9 billion in 2024, highlighting the vast number of players.

Presence of Large Global Players

Major tech and automotive giants are increasingly involved in connected vehicles and fleet management, significantly impacting competition. Companies like Google and Tesla are investing heavily, leveraging their resources and brand power. For instance, Tesla's market cap in early 2024 was around $600 billion, underscoring its financial muscle. This influx creates tougher competition.

Price-Based Competition

Price-based competition is a key factor in the competitive rivalry for G7 Networks. The similarity in service offerings can lead to price wars. For instance, in 2024, the average revenue per user (ARPU) in the telecom sector saw a 3% decrease due to pricing pressures. G7's profit margins could be squeezed if they lower prices to compete.

Rapid Technological Advancements

The IoT and fleet management sectors see rapid tech shifts. Competitors like Samsara and Geotab constantly innovate, boosting features and platforms. G7 Networks must invest significantly in R&D to keep pace. In 2024, the global fleet management market was valued at $28.7 billion. Continuous innovation is a must.

- AI and data analytics are key drivers.

- Connectivity advancements are crucial.

- Competitors are always improving.

- R&D investment is vital for G7.

Market Growth Attracts New Competitors

The expanding global IoT fleet management market, expected to be worth billions in the coming years, draws in new competitors and investment. This growth increases rivalry as companies compete for market share. For example, the global fleet management market was valued at $24.52 billion in 2023. The market is projected to reach $53.07 billion by 2029.

- Market growth attracts new entrants.

- Increased competition intensifies rivalry.

- More players fight for market share.

- Investment and innovation are stimulated.

IoT Fleet Management: Navigating the Competitive Landscape

Competitive rivalry in the IoT fleet management market is intense, fueled by numerous players and rapid tech advancements. G7 Networks faces pressure from established firms and tech giants like Tesla, which had a market cap of around $600 billion in early 2024. Price competition and continuous innovation, with the global market valued at $28.7 billion in 2024, are significant challenges for G7.

| Aspect | Details | Impact on G7 |

|---|---|---|

| Competitors | Established telematics firms, tech giants (Tesla, Google). | Increased competition; need for differentiation. |

| Price Competition | Similarity in service offerings leads to price wars; ARPU decreased 3% in telecom in 2024. | Squeezed profit margins. |

| Innovation | Rapid tech shifts; AI, data analytics, connectivity advancements. | High R&D investment is vital to keep up. |