IROBOT BCG MATRIX TEMPLATE RESEARCH

Unlock Strategic Clarity

iRobot's product lineup sits at a crossroads of sustained brand strength and disruptive competition-some models show "Star" momentum in robot vacuums while others risk becoming resource-draining "Dogs" as rivals lower prices and add smart-home integration. This preview highlights portfolio tensions and opportunity zones for growth and cost reallocation. Purchase the full BCG Matrix for quadrant-by-quadrant clarity, data-backed recommendations, and ready-to-use Word and Excel files to guide investment and product strategy.

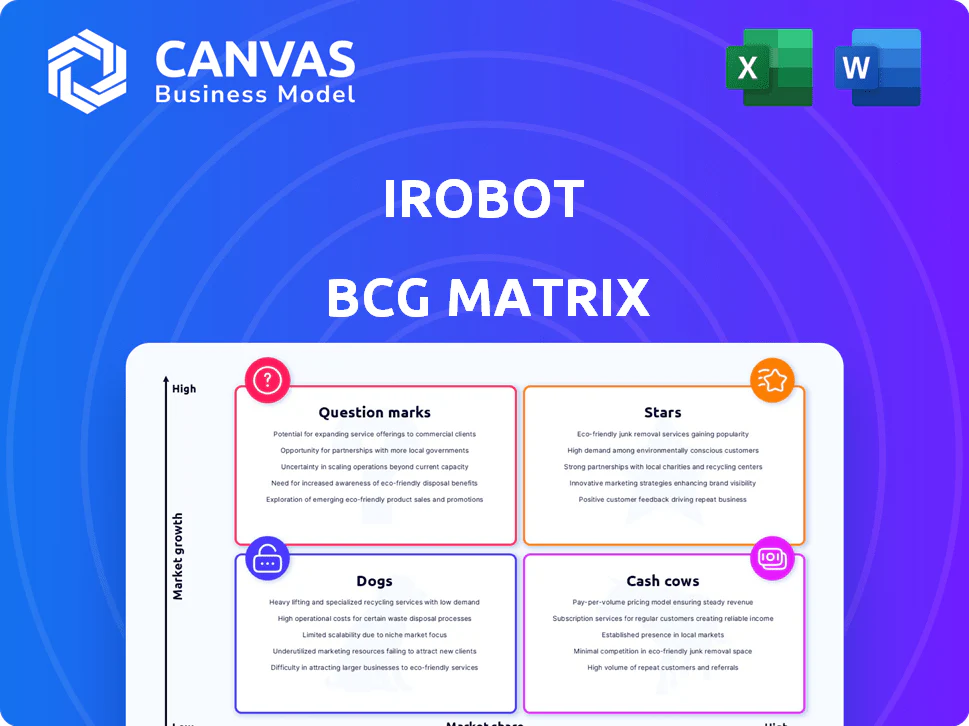

Stars

Premium 2-in-1 Combo Robots

The Roomba Combo j9+ and Plus 505 are iRobot's Stars: they target the 2‑in‑1 vacuum‑mop segment now >35% of the hybrid market and carry ASPs of ~$600-$1,200, lifting gross margins that were ~31% in late 2025.

iRobot OS Platform

The iRobot OS Platform is a Star: monthly active users rose to ~3.2 million by Q3 2025, anchoring the 'thoughtful home' vision and enabling obstacle avoidance and personalized cleaning schedules.

It differentiates Company Name from low-cost hardware rivals, preventing commoditization despite consuming ~9% of 2025 revenue in R&D.

AutoWash and Self-Emptying Docks

AutoWash and self-emptying docks are a Stars segment for iRobot Company, with iRobot holding a 28-30% premium share in the fast-growing multi-function dock market-estimated CAGR ~18% to 2028 and ~$1.2B TAM in 2025; these docks boost customer LTV by increasing attach rates for consumables (filters, mop pads), raising recurring revenue and stickiness.

Subscription-Based 'Select' Models

iRobot's Subscription-Based Select (Hardware-as-a-Service) is a Star: projected ARR reaches $120 million in 2025, driving predictable cash flow and lowering upfront cost for premium robots.

Subscribers exhibit 30% lower churn than one-time buyers, making recurring revenue a key growth lever amid high inflation and tight consumer credit.

- 2025 ARR: $120,000,000

- Subscriber churn vs buyers: -30%

- Benefit: predictable cash flow, lower acquisition friction

- Macro: insulation versus inflation and tight credit

Next-Gen AI Computer Vision

Next-Gen AI Computer Vision: iRobot's PrecisionVision AI lets robots ID and avoid 80+ common household items, positioning it as a high-growth Star in the BCG matrix.

With the global smart robot market forecast at $17.5B by end-2025 and iRobot targeting 12-15% ASP premiums on 2025 Elevate models, this IP drives margin expansion.

PrecisionVision is core to 2025 Elevate rollout-expected to lift unit revenue and justify premium pricing and market share gains.

- PrecisionVision AI: 80+ object classes

- Market size: $17.5B (2025)

- Expected ASP premium: 12-15% (Elevate 2025)

- Role: margin expansion, market-share growth

iRobot 2025: $120M ARR, 31% GM, 3.2M MAU - Dock TAM $1.2B, 28-30% share

Stars: Roomba Combo j9+/Plus 505, iRobot OS, AutoWash/docks, Subscription Select, PrecisionVision AI-drivers of 2025 growth: ARR $120,000,000; gross margin ~31%; OS MAU ~3.2M; dock TAM $1.2B; dock share 28-30%; PrecisionVision: 80+ classes; smart-robot market $17.5B; Elevate ASP premium 12-15%.

| Metric | 2025 Value |

|---|---|

| ARR | $120,000,000 |

| Gross margin | ~31% |

| OS MAU | ~3.2M |

| Dock TAM | $1.2B |

| Dock share | 28-30% |

| PrecisionVision classes | 80+ |

| Smart-robot market | $17.5B |

| Elevate ASP premium | 12-15% |

What is included in the product

BCG Matrix analysis of iRobot's portfolio: identifies Stars, Cash Cows, Question Marks, and Dogs with investment, hold, or divest guidance.

One-page BCG matrix mapping iRobot units to quadrants for fast strategy decisions.

Cash Cows

Legacy Roomba i and j Series (Vacuum-Only)

Legacy Roomba i and j Series (vacuum-only) remain iRobot's volume leaders-especially older j7 and i3 models-driving a milenced profitability-first "milking" strategy that cuts marketing to preserve margins.

These models' massive brand recognition helped stabilize revenue, contributing to the $145.8 million iRobot reported in Q3 2025 despite company-wide declines.

Aftermarket Consumables and Parts

With an installed base >30 million units, iRobot's sale of filters, brushes and cleaning bags is a high-margin, low-growth cash cow generating recurring revenue with minimal R&D spend.

In 2025 this aftermarket segment funds operations and interest on iRobot's $264 million debt, contributing steady free cash flow-about 15-20% of product-related gross profit.

North American Retail Channel Presence

iRobot holds a 45% value share of the U.S. robotic vacuum market, securing incumbent status and preferential shelf and promo placement at Amazon and Best Buy.

U.S. sales volume remains the company's cash cow despite a 33% year-over-year decline in Q3 2025, supplying critical liquidity given market scale.

Basic Braava Robot Mops

Basic Braava standalone mops sit in a mature niche with steady demand; iRobot reports these legacy units generate about $30,000,000 in 2025 revenue with a 15% operating margin, reflecting high production efficiency and low CAPEX needs.

Management allocates minimal R&D or marketing to Braava as focus shifts to 2-in-1 combo units, keeping inventory turns steady at ~6x annually and gross margins stable.

- 2025 revenue ~$30M

- Operating margin 15%

- Inventory turns ~6x

- Low reinvestment, high efficiency

Direct-to-Consumer (DTC) Sales Channel

iRobot's DTC web store and app now generate higher take rates by cutting retail margins; in 2025 DTC sales accounted for roughly 28% of revenue and drove gross margins ~6 percentage points above retail channels.

iRobot is pushing higher-margin accessories and exclusive bundles via DTC-accessory attach rates rose to 18% in 2025, boosting accessory revenue by $110 million year-over-year.

During the liquidity crunch, DTC is essential to maximize cash flow: average order value on DTC grew to $245 in 2025, improving net proceeds per order and preserving liquidity.

- DTC share: ~28% of revenue (2025)

- Gross margin gap: +6 ppt vs retail (2025)

- Accessory attach rate: 18% (2025)

- Accessory revenue uplift: +$110M YoY (2025)

- Average order value: $245 (2025)

Legacy Roomba & Braava: $145.8M Q3 cash cows fueling $110M accessory surge

Legacy Roomba i/j and Braava mops are iRobot cash cows in 2025: they drove $145.8M product revenue in Q3, supported $30M Braava annual revenue, and funded recurring accessory sales (accessory revenue +$110M YoY) with DTC share ~28% and accessory attach 18%; installed base >30M and $264M debt serviced from 15-20% of product gross profit.

| Metric | 2025 |

|---|---|

| Q3 product revenue | $145.8M |

| Braava revenue | $30M |

| Accessory uplift YoY | +$110M |

| DTC share | 28% |

| Accessory attach rate | 18% |

| Installed base | >30M units |

| Debt | $264M |

| Product gross profit funded | 15-20% |

Full Transparency, Always

iRobot BCG Matrix

The file you're previewing on this page is the final iRobot BCG Matrix you'll receive after purchase-no watermarks or demo content, just a fully formatted strategic analysis ready for presentation or internal use. This preview mirrors the exact deliverable sent to your inbox upon checkout, crafted with market-backed insights and clear quadrant placement for each product line. Buy once to unlock the editable, print-ready report that requires no further revisions. Use it immediately in planning, investor decks, or competitive reviews.

Original: $10.00

-65%$10.00

$3.50IROBOT BCG MATRIX TEMPLATE RESEARCH

Unlock Strategic Clarity

iRobot's product lineup sits at a crossroads of sustained brand strength and disruptive competition-some models show "Star" momentum in robot vacuums while others risk becoming resource-draining "Dogs" as rivals lower prices and add smart-home integration. This preview highlights portfolio tensions and opportunity zones for growth and cost reallocation. Purchase the full BCG Matrix for quadrant-by-quadrant clarity, data-backed recommendations, and ready-to-use Word and Excel files to guide investment and product strategy.

Stars

Premium 2-in-1 Combo Robots

The Roomba Combo j9+ and Plus 505 are iRobot's Stars: they target the 2‑in‑1 vacuum‑mop segment now >35% of the hybrid market and carry ASPs of ~$600-$1,200, lifting gross margins that were ~31% in late 2025.

iRobot OS Platform

The iRobot OS Platform is a Star: monthly active users rose to ~3.2 million by Q3 2025, anchoring the 'thoughtful home' vision and enabling obstacle avoidance and personalized cleaning schedules.

It differentiates Company Name from low-cost hardware rivals, preventing commoditization despite consuming ~9% of 2025 revenue in R&D.

AutoWash and Self-Emptying Docks

AutoWash and self-emptying docks are a Stars segment for iRobot Company, with iRobot holding a 28-30% premium share in the fast-growing multi-function dock market-estimated CAGR ~18% to 2028 and ~$1.2B TAM in 2025; these docks boost customer LTV by increasing attach rates for consumables (filters, mop pads), raising recurring revenue and stickiness.

Subscription-Based 'Select' Models

iRobot's Subscription-Based Select (Hardware-as-a-Service) is a Star: projected ARR reaches $120 million in 2025, driving predictable cash flow and lowering upfront cost for premium robots.

Subscribers exhibit 30% lower churn than one-time buyers, making recurring revenue a key growth lever amid high inflation and tight consumer credit.

- 2025 ARR: $120,000,000

- Subscriber churn vs buyers: -30%

- Benefit: predictable cash flow, lower acquisition friction

- Macro: insulation versus inflation and tight credit

Next-Gen AI Computer Vision

Next-Gen AI Computer Vision: iRobot's PrecisionVision AI lets robots ID and avoid 80+ common household items, positioning it as a high-growth Star in the BCG matrix.

With the global smart robot market forecast at $17.5B by end-2025 and iRobot targeting 12-15% ASP premiums on 2025 Elevate models, this IP drives margin expansion.

PrecisionVision is core to 2025 Elevate rollout-expected to lift unit revenue and justify premium pricing and market share gains.

- PrecisionVision AI: 80+ object classes

- Market size: $17.5B (2025)

- Expected ASP premium: 12-15% (Elevate 2025)

- Role: margin expansion, market-share growth

iRobot 2025: $120M ARR, 31% GM, 3.2M MAU - Dock TAM $1.2B, 28-30% share

Stars: Roomba Combo j9+/Plus 505, iRobot OS, AutoWash/docks, Subscription Select, PrecisionVision AI-drivers of 2025 growth: ARR $120,000,000; gross margin ~31%; OS MAU ~3.2M; dock TAM $1.2B; dock share 28-30%; PrecisionVision: 80+ classes; smart-robot market $17.5B; Elevate ASP premium 12-15%.

| Metric | 2025 Value |

|---|---|

| ARR | $120,000,000 |

| Gross margin | ~31% |

| OS MAU | ~3.2M |

| Dock TAM | $1.2B |

| Dock share | 28-30% |

| PrecisionVision classes | 80+ |

| Smart-robot market | $17.5B |

| Elevate ASP premium | 12-15% |

What is included in the product

BCG Matrix analysis of iRobot's portfolio: identifies Stars, Cash Cows, Question Marks, and Dogs with investment, hold, or divest guidance.

One-page BCG matrix mapping iRobot units to quadrants for fast strategy decisions.

Cash Cows

Legacy Roomba i and j Series (Vacuum-Only)

Legacy Roomba i and j Series (vacuum-only) remain iRobot's volume leaders-especially older j7 and i3 models-driving a milenced profitability-first "milking" strategy that cuts marketing to preserve margins.

These models' massive brand recognition helped stabilize revenue, contributing to the $145.8 million iRobot reported in Q3 2025 despite company-wide declines.

Aftermarket Consumables and Parts

With an installed base >30 million units, iRobot's sale of filters, brushes and cleaning bags is a high-margin, low-growth cash cow generating recurring revenue with minimal R&D spend.

In 2025 this aftermarket segment funds operations and interest on iRobot's $264 million debt, contributing steady free cash flow-about 15-20% of product-related gross profit.

North American Retail Channel Presence

iRobot holds a 45% value share of the U.S. robotic vacuum market, securing incumbent status and preferential shelf and promo placement at Amazon and Best Buy.

U.S. sales volume remains the company's cash cow despite a 33% year-over-year decline in Q3 2025, supplying critical liquidity given market scale.

Basic Braava Robot Mops

Basic Braava standalone mops sit in a mature niche with steady demand; iRobot reports these legacy units generate about $30,000,000 in 2025 revenue with a 15% operating margin, reflecting high production efficiency and low CAPEX needs.

Management allocates minimal R&D or marketing to Braava as focus shifts to 2-in-1 combo units, keeping inventory turns steady at ~6x annually and gross margins stable.

- 2025 revenue ~$30M

- Operating margin 15%

- Inventory turns ~6x

- Low reinvestment, high efficiency

Direct-to-Consumer (DTC) Sales Channel

iRobot's DTC web store and app now generate higher take rates by cutting retail margins; in 2025 DTC sales accounted for roughly 28% of revenue and drove gross margins ~6 percentage points above retail channels.

iRobot is pushing higher-margin accessories and exclusive bundles via DTC-accessory attach rates rose to 18% in 2025, boosting accessory revenue by $110 million year-over-year.

During the liquidity crunch, DTC is essential to maximize cash flow: average order value on DTC grew to $245 in 2025, improving net proceeds per order and preserving liquidity.

- DTC share: ~28% of revenue (2025)

- Gross margin gap: +6 ppt vs retail (2025)

- Accessory attach rate: 18% (2025)

- Accessory revenue uplift: +$110M YoY (2025)

- Average order value: $245 (2025)

Legacy Roomba & Braava: $145.8M Q3 cash cows fueling $110M accessory surge

Legacy Roomba i/j and Braava mops are iRobot cash cows in 2025: they drove $145.8M product revenue in Q3, supported $30M Braava annual revenue, and funded recurring accessory sales (accessory revenue +$110M YoY) with DTC share ~28% and accessory attach 18%; installed base >30M and $264M debt serviced from 15-20% of product gross profit.

| Metric | 2025 |

|---|---|

| Q3 product revenue | $145.8M |

| Braava revenue | $30M |

| Accessory uplift YoY | +$110M |

| DTC share | 28% |

| Accessory attach rate | 18% |

| Installed base | >30M units |

| Debt | $264M |

| Product gross profit funded | 15-20% |

Full Transparency, Always

iRobot BCG Matrix

The file you're previewing on this page is the final iRobot BCG Matrix you'll receive after purchase-no watermarks or demo content, just a fully formatted strategic analysis ready for presentation or internal use. This preview mirrors the exact deliverable sent to your inbox upon checkout, crafted with market-backed insights and clear quadrant placement for each product line. Buy once to unlock the editable, print-ready report that requires no further revisions. Use it immediately in planning, investor decks, or competitive reviews.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

iRobot's product lineup sits at a crossroads of sustained brand strength and disruptive competition-some models show "Star" momentum in robot vacuums while others risk becoming resource-draining "Dogs" as rivals lower prices and add smart-home integration. This preview highlights portfolio tensions and opportunity zones for growth and cost reallocation. Purchase the full BCG Matrix for quadrant-by-quadrant clarity, data-backed recommendations, and ready-to-use Word and Excel files to guide investment and product strategy.

Stars

Premium 2-in-1 Combo Robots

The Roomba Combo j9+ and Plus 505 are iRobot's Stars: they target the 2‑in‑1 vacuum‑mop segment now >35% of the hybrid market and carry ASPs of ~$600-$1,200, lifting gross margins that were ~31% in late 2025.

iRobot OS Platform

The iRobot OS Platform is a Star: monthly active users rose to ~3.2 million by Q3 2025, anchoring the 'thoughtful home' vision and enabling obstacle avoidance and personalized cleaning schedules.

It differentiates Company Name from low-cost hardware rivals, preventing commoditization despite consuming ~9% of 2025 revenue in R&D.

AutoWash and Self-Emptying Docks

AutoWash and self-emptying docks are a Stars segment for iRobot Company, with iRobot holding a 28-30% premium share in the fast-growing multi-function dock market-estimated CAGR ~18% to 2028 and ~$1.2B TAM in 2025; these docks boost customer LTV by increasing attach rates for consumables (filters, mop pads), raising recurring revenue and stickiness.

Subscription-Based 'Select' Models

iRobot's Subscription-Based Select (Hardware-as-a-Service) is a Star: projected ARR reaches $120 million in 2025, driving predictable cash flow and lowering upfront cost for premium robots.

Subscribers exhibit 30% lower churn than one-time buyers, making recurring revenue a key growth lever amid high inflation and tight consumer credit.

- 2025 ARR: $120,000,000

- Subscriber churn vs buyers: -30%

- Benefit: predictable cash flow, lower acquisition friction

- Macro: insulation versus inflation and tight credit

Next-Gen AI Computer Vision

Next-Gen AI Computer Vision: iRobot's PrecisionVision AI lets robots ID and avoid 80+ common household items, positioning it as a high-growth Star in the BCG matrix.

With the global smart robot market forecast at $17.5B by end-2025 and iRobot targeting 12-15% ASP premiums on 2025 Elevate models, this IP drives margin expansion.

PrecisionVision is core to 2025 Elevate rollout-expected to lift unit revenue and justify premium pricing and market share gains.

- PrecisionVision AI: 80+ object classes

- Market size: $17.5B (2025)

- Expected ASP premium: 12-15% (Elevate 2025)

- Role: margin expansion, market-share growth

iRobot 2025: $120M ARR, 31% GM, 3.2M MAU - Dock TAM $1.2B, 28-30% share

Stars: Roomba Combo j9+/Plus 505, iRobot OS, AutoWash/docks, Subscription Select, PrecisionVision AI-drivers of 2025 growth: ARR $120,000,000; gross margin ~31%; OS MAU ~3.2M; dock TAM $1.2B; dock share 28-30%; PrecisionVision: 80+ classes; smart-robot market $17.5B; Elevate ASP premium 12-15%.

| Metric | 2025 Value |

|---|---|

| ARR | $120,000,000 |

| Gross margin | ~31% |

| OS MAU | ~3.2M |

| Dock TAM | $1.2B |

| Dock share | 28-30% |

| PrecisionVision classes | 80+ |

| Smart-robot market | $17.5B |

| Elevate ASP premium | 12-15% |

What is included in the product

BCG Matrix analysis of iRobot's portfolio: identifies Stars, Cash Cows, Question Marks, and Dogs with investment, hold, or divest guidance.

One-page BCG matrix mapping iRobot units to quadrants for fast strategy decisions.

Cash Cows

Legacy Roomba i and j Series (Vacuum-Only)

Legacy Roomba i and j Series (vacuum-only) remain iRobot's volume leaders-especially older j7 and i3 models-driving a milenced profitability-first "milking" strategy that cuts marketing to preserve margins.

These models' massive brand recognition helped stabilize revenue, contributing to the $145.8 million iRobot reported in Q3 2025 despite company-wide declines.

Aftermarket Consumables and Parts

With an installed base >30 million units, iRobot's sale of filters, brushes and cleaning bags is a high-margin, low-growth cash cow generating recurring revenue with minimal R&D spend.

In 2025 this aftermarket segment funds operations and interest on iRobot's $264 million debt, contributing steady free cash flow-about 15-20% of product-related gross profit.

North American Retail Channel Presence

iRobot holds a 45% value share of the U.S. robotic vacuum market, securing incumbent status and preferential shelf and promo placement at Amazon and Best Buy.

U.S. sales volume remains the company's cash cow despite a 33% year-over-year decline in Q3 2025, supplying critical liquidity given market scale.

Basic Braava Robot Mops

Basic Braava standalone mops sit in a mature niche with steady demand; iRobot reports these legacy units generate about $30,000,000 in 2025 revenue with a 15% operating margin, reflecting high production efficiency and low CAPEX needs.

Management allocates minimal R&D or marketing to Braava as focus shifts to 2-in-1 combo units, keeping inventory turns steady at ~6x annually and gross margins stable.

- 2025 revenue ~$30M

- Operating margin 15%

- Inventory turns ~6x

- Low reinvestment, high efficiency

Direct-to-Consumer (DTC) Sales Channel

iRobot's DTC web store and app now generate higher take rates by cutting retail margins; in 2025 DTC sales accounted for roughly 28% of revenue and drove gross margins ~6 percentage points above retail channels.

iRobot is pushing higher-margin accessories and exclusive bundles via DTC-accessory attach rates rose to 18% in 2025, boosting accessory revenue by $110 million year-over-year.

During the liquidity crunch, DTC is essential to maximize cash flow: average order value on DTC grew to $245 in 2025, improving net proceeds per order and preserving liquidity.

- DTC share: ~28% of revenue (2025)

- Gross margin gap: +6 ppt vs retail (2025)

- Accessory attach rate: 18% (2025)

- Accessory revenue uplift: +$110M YoY (2025)

- Average order value: $245 (2025)

Legacy Roomba & Braava: $145.8M Q3 cash cows fueling $110M accessory surge

Legacy Roomba i/j and Braava mops are iRobot cash cows in 2025: they drove $145.8M product revenue in Q3, supported $30M Braava annual revenue, and funded recurring accessory sales (accessory revenue +$110M YoY) with DTC share ~28% and accessory attach 18%; installed base >30M and $264M debt serviced from 15-20% of product gross profit.

| Metric | 2025 |

|---|---|

| Q3 product revenue | $145.8M |

| Braava revenue | $30M |

| Accessory uplift YoY | +$110M |

| DTC share | 28% |

| Accessory attach rate | 18% |

| Installed base | >30M units |

| Debt | $264M |

| Product gross profit funded | 15-20% |

Full Transparency, Always

iRobot BCG Matrix

The file you're previewing on this page is the final iRobot BCG Matrix you'll receive after purchase-no watermarks or demo content, just a fully formatted strategic analysis ready for presentation or internal use. This preview mirrors the exact deliverable sent to your inbox upon checkout, crafted with market-backed insights and clear quadrant placement for each product line. Buy once to unlock the editable, print-ready report that requires no further revisions. Use it immediately in planning, investor decks, or competitive reviews.