LETSGETCHECKED PORTER'S FIVE FORCES TEMPLATE RESEARCH

A Must-Have Tool for Decision-Makers

LetsGetChecked faces intense buyer power and evolving substitute threats as telehealth and at-home testing converge, while supplier leverage and regulatory shifts add complexity to margins and scale-up plans.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore LetsGetChecked's competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Diagnostic Equipment Providers

LetsGetChecked relies on specialized diagnostic machinery from few dominant suppliers like Danaher and Thermo Fisher Scientific, creating high dependency; Danaher and Thermo Fisher reported combined 2025 revenue of about $84.5 billion, underscoring their market heft.

Although LetsGetChecked runs its own labs, instrument switching costs and mandatory maintenance contracts raise total cost of ownership by an estimated 15-25%, locking procurement choices.

Supplier concentration lets manufacturers keep firm pricing: model price increases averaged 3-6% annually through 2024-25 despite rising at‑home test volumes.

Medical Component and Kit Manufacturers

The supply of medical-grade swabs, collection tubes, and lancets for LetsGetChecked faced global disruptions in 2024-25; FDA-quality validation raised switching costs, with supplier lead times up 35% and spot prices up ~18% in FY2025, giving established manufacturers moderate pricing and delivery leverage.

Logistics and Cold Chain Carriers

LetsGetChecked relies on UPS and FedEx for temperature-controlled, time-sensitive sample transport; in 2025 these carriers handle ~80-90% of US next-day medical shipments, giving them outsized leverage.

Few national alternatives meet diagnostic cold-chain specs, so carriers' pricing shifts-fuel surcharges rose ~18% in 2024-25-directly compress LetsGetChecked's margins with limited negotiation room.

Specialized Medical and Lab Personnel

Scarcity of licensed clinical laboratory scientists and board-certified physicians creates a talent-driven supply constraint for LetsGetChecked, with US vacancy rates for clinical lab roles near 12% in 2025 and median MLS wages up 8% y/y to $76,000.

Ongoing healthcare labor shortages through 2025 keep retention costs high; physician review stipends and benefits raised provider costs ~10-15% versus 2023 benchmarks.

This human capital underpins service quality, giving suppliers bargaining power manifested in rising wages, signing bonuses, and demand for flexible schedules.

- 12% vacancy rate for clinical lab roles (2025)

- Median MLS wage $76,000 (2025, +8% y/y)

- Provider cost pressure +10-15% vs 2023

- Higher signing bonuses and benefits required

Cloud Infrastructure and Cybersecurity Vendors

Managing sensitive patient data forces LetsGetChecked to use HIPAA-compliant cloud services like Amazon Web Services or Microsoft Azure, which together held ~66% of global cloud IaaS/PaaS market in 2025, limiting bargaining power.

Their standardized pricing and limited discounting for mid-sized health techs, plus switching costs-data egress fees up to $0.09/GB and migration projects often >$1M-create vendor lock-in favoring providers.

Bullets:

- AWS+Azure ~66% IaaS/PaaS share (2025)

- Data egress up to $0.09/GB

- Typical migration >$1M

- HIPAA compliance required, few alternative vendors

Concentrated suppliers drive costs up: instruments, carriers, cloud, and talent shortages

Suppliers exert moderate‑high power: concentrated instrument vendors (Danaher/Thermo Fisher combined revenue $84.5B in 2025), logistics carriers (UPS/FedEx ~80-90% US medical next‑day), cloud providers (AWS+Azure ~66% IaaS/PaaS) and talent shortages (12% lab vacancy; median MLS $76,000) raise costs and switching barriers.

| Category | 2025 Metric |

|---|---|

| Instrument vendors | $84.5B combined revenue |

| Carriers | 80-90% US medical next‑day |

| Cloud | 66% IaaS/PaaS |

| Lab talent | 12% vacancy; $76,000 median |

What is included in the product

Tailored exclusively for LetsGetChecked, this Porter's Five Forces overview uncovers competitive pressures, customer and supplier influence, threats from substitutes and new entrants, and highlights disruptive forces shaping pricing, margins, and market positioning.

Clear, one-sheet Porter's Five Forces for LetsGetChecked-fast-strategic insights to spot competitive threats and relief points for product, pricing, and partnership decisions.

Customers Bargaining Power

Low Switching Costs for Individual Consumers

In LetsGetChecked's direct-to-consumer segment, switching costs are minimal-patients face virtually no fees to move to Everlywell or Thirty-Two Labs, so price and convenience dominate purchase decisions.

Most diagnostic tests are one-off buys, not subscriptions, so brand loyalty is limited; 2024 market surveys show 68% of consumers prioritize price when selecting at-home tests.

That dynamic forced LetsGetChecked to spend an estimated $72M on marketing in FY2025 to maintain share and improve UX, since customers can compare prices and reviews instantly online.

Bargaining Leverage of Large Employer Groups

Large employer groups drive ~40% of LetsGetChecked's 2025 revenue and exert strong bargaining power, securing volume discounts and bespoke dashboards; a single lost enterprise (often thousands of users) can swing quarterly revenue by an estimated $25-40M, so buyers can push pricing and SLA concessions that shift negotiating leverage toward employers.

Transparency in Market Pricing

The digital at-home testing market lets consumers compare prices instantly, driving price transparency; LetsGetChecked reported average revenue per test of $58 in FY2025, aligning with market medians and constraining unilateral price hikes.

Influence of Health Insurance Providers

As LetsGetChecked pursues deeper ties with insurers, payers like UnitedHealth (2025 revenue $356B) and CVS Health/Aetna ($322B) control reimbursement rates and membership access, making their approval pivotal for growth.

If insurers deny coverage, typical out-of-pocket fees-$49-$199 per at-home test-drive patients back to covered clinic labs.

- Insurer gatekeeping: controls millions-UnitedHealth 2025 members ~31M

- Reimbursement sets price: limits margin on $49-$199 tests

- Coverage denial increases out-of-pocket churn

Demand for Integrated Digital Health Ecosystems

Modern consumers expect portable, integrated health data, forcing LetsGetChecked to build high-quality APIs and interoperability-costs that weighed on tech and R&D spending as the company expanded in 2025.

In 2025, 68% of US telehealth users cited data portability as a key feature; failing to meet this norm risks churn and lower lifetime value.

Customers treat seamless integration as standard, not premium, raising bargaining power and pressuring LetsGetChecked's margins as it funds integrations with EHRs and third-party apps.

- 68% of US telehealth users want data portability (2025)

- Integration increases R&D/API costs, pressuring margins in 2025

- Seamless data seen as standard-raises customer bargaining power

Pricing constrained: high customer bargaining, enterprise swings & insurer caps

Customers hold high bargaining power: low switching costs and price sensitivity (68% favor price) limit LetsGetChecked's pricing; FY2025 ARPT $58, marketing spend $72M, enterprise buyers (~40% revenue) can swing $25-40M per quarter, and insurer gatekeepers (UnitedHealth ~31M members) set reimbursement that caps margins.

| Metric | Value (FY2025) |

|---|---|

| ARPT | $58 |

| Marketing spend | $72M |

| Enterprise revenue share | ~40% |

| Enterprise swing/quarter | $25-40M |

| Price sensitivity | 68% |

| UnitedHealth members | ~31M |

Full Version Awaits

LetsGetChecked Porter's Five Forces Analysis

This preview shows the exact LetsGetChecked Porter's Five Forces analysis you'll receive immediately after purchase-no placeholders or mockups, fully formatted and ready for use.

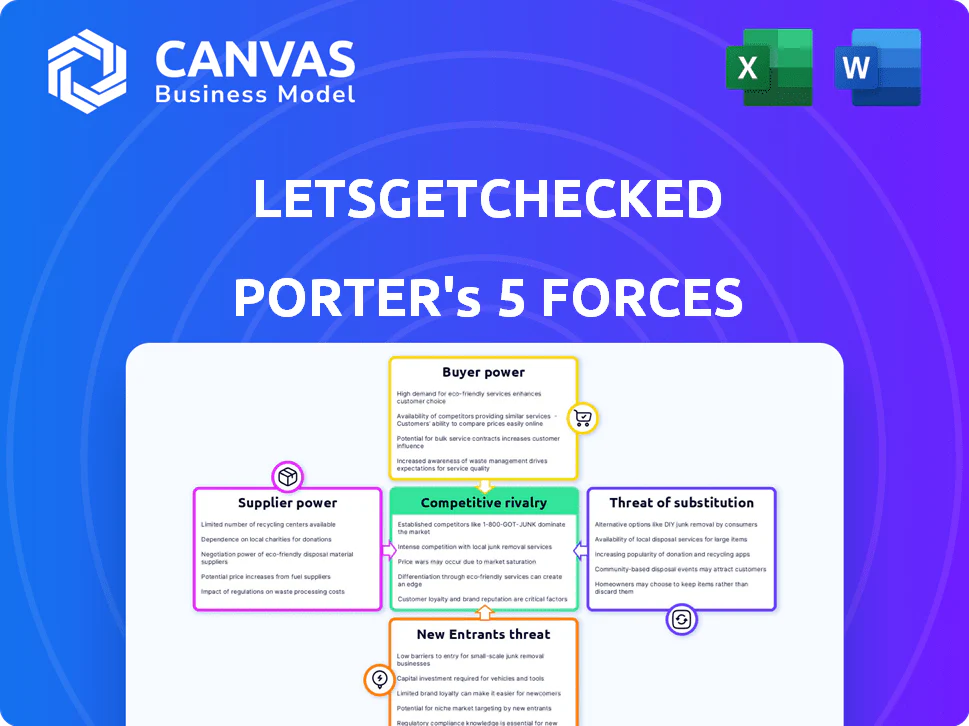

The document covers supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry with clear implications and action points tailored for investors and strategists.

LETSGETCHECKED PORTER'S FIVE FORCES TEMPLATE RESEARCH

A Must-Have Tool for Decision-Makers

LetsGetChecked faces intense buyer power and evolving substitute threats as telehealth and at-home testing converge, while supplier leverage and regulatory shifts add complexity to margins and scale-up plans.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore LetsGetChecked's competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Diagnostic Equipment Providers

LetsGetChecked relies on specialized diagnostic machinery from few dominant suppliers like Danaher and Thermo Fisher Scientific, creating high dependency; Danaher and Thermo Fisher reported combined 2025 revenue of about $84.5 billion, underscoring their market heft.

Although LetsGetChecked runs its own labs, instrument switching costs and mandatory maintenance contracts raise total cost of ownership by an estimated 15-25%, locking procurement choices.

Supplier concentration lets manufacturers keep firm pricing: model price increases averaged 3-6% annually through 2024-25 despite rising at‑home test volumes.

Medical Component and Kit Manufacturers

The supply of medical-grade swabs, collection tubes, and lancets for LetsGetChecked faced global disruptions in 2024-25; FDA-quality validation raised switching costs, with supplier lead times up 35% and spot prices up ~18% in FY2025, giving established manufacturers moderate pricing and delivery leverage.

Logistics and Cold Chain Carriers

LetsGetChecked relies on UPS and FedEx for temperature-controlled, time-sensitive sample transport; in 2025 these carriers handle ~80-90% of US next-day medical shipments, giving them outsized leverage.

Few national alternatives meet diagnostic cold-chain specs, so carriers' pricing shifts-fuel surcharges rose ~18% in 2024-25-directly compress LetsGetChecked's margins with limited negotiation room.

Specialized Medical and Lab Personnel

Scarcity of licensed clinical laboratory scientists and board-certified physicians creates a talent-driven supply constraint for LetsGetChecked, with US vacancy rates for clinical lab roles near 12% in 2025 and median MLS wages up 8% y/y to $76,000.

Ongoing healthcare labor shortages through 2025 keep retention costs high; physician review stipends and benefits raised provider costs ~10-15% versus 2023 benchmarks.

This human capital underpins service quality, giving suppliers bargaining power manifested in rising wages, signing bonuses, and demand for flexible schedules.

- 12% vacancy rate for clinical lab roles (2025)

- Median MLS wage $76,000 (2025, +8% y/y)

- Provider cost pressure +10-15% vs 2023

- Higher signing bonuses and benefits required

Cloud Infrastructure and Cybersecurity Vendors

Managing sensitive patient data forces LetsGetChecked to use HIPAA-compliant cloud services like Amazon Web Services or Microsoft Azure, which together held ~66% of global cloud IaaS/PaaS market in 2025, limiting bargaining power.

Their standardized pricing and limited discounting for mid-sized health techs, plus switching costs-data egress fees up to $0.09/GB and migration projects often >$1M-create vendor lock-in favoring providers.

Bullets:

- AWS+Azure ~66% IaaS/PaaS share (2025)

- Data egress up to $0.09/GB

- Typical migration >$1M

- HIPAA compliance required, few alternative vendors

Concentrated suppliers drive costs up: instruments, carriers, cloud, and talent shortages

Suppliers exert moderate‑high power: concentrated instrument vendors (Danaher/Thermo Fisher combined revenue $84.5B in 2025), logistics carriers (UPS/FedEx ~80-90% US medical next‑day), cloud providers (AWS+Azure ~66% IaaS/PaaS) and talent shortages (12% lab vacancy; median MLS $76,000) raise costs and switching barriers.

| Category | 2025 Metric |

|---|---|

| Instrument vendors | $84.5B combined revenue |

| Carriers | 80-90% US medical next‑day |

| Cloud | 66% IaaS/PaaS |

| Lab talent | 12% vacancy; $76,000 median |

What is included in the product

Tailored exclusively for LetsGetChecked, this Porter's Five Forces overview uncovers competitive pressures, customer and supplier influence, threats from substitutes and new entrants, and highlights disruptive forces shaping pricing, margins, and market positioning.

Clear, one-sheet Porter's Five Forces for LetsGetChecked-fast-strategic insights to spot competitive threats and relief points for product, pricing, and partnership decisions.

Customers Bargaining Power

Low Switching Costs for Individual Consumers

In LetsGetChecked's direct-to-consumer segment, switching costs are minimal-patients face virtually no fees to move to Everlywell or Thirty-Two Labs, so price and convenience dominate purchase decisions.

Most diagnostic tests are one-off buys, not subscriptions, so brand loyalty is limited; 2024 market surveys show 68% of consumers prioritize price when selecting at-home tests.

That dynamic forced LetsGetChecked to spend an estimated $72M on marketing in FY2025 to maintain share and improve UX, since customers can compare prices and reviews instantly online.

Bargaining Leverage of Large Employer Groups

Large employer groups drive ~40% of LetsGetChecked's 2025 revenue and exert strong bargaining power, securing volume discounts and bespoke dashboards; a single lost enterprise (often thousands of users) can swing quarterly revenue by an estimated $25-40M, so buyers can push pricing and SLA concessions that shift negotiating leverage toward employers.

Transparency in Market Pricing

The digital at-home testing market lets consumers compare prices instantly, driving price transparency; LetsGetChecked reported average revenue per test of $58 in FY2025, aligning with market medians and constraining unilateral price hikes.

Influence of Health Insurance Providers

As LetsGetChecked pursues deeper ties with insurers, payers like UnitedHealth (2025 revenue $356B) and CVS Health/Aetna ($322B) control reimbursement rates and membership access, making their approval pivotal for growth.

If insurers deny coverage, typical out-of-pocket fees-$49-$199 per at-home test-drive patients back to covered clinic labs.

- Insurer gatekeeping: controls millions-UnitedHealth 2025 members ~31M

- Reimbursement sets price: limits margin on $49-$199 tests

- Coverage denial increases out-of-pocket churn

Demand for Integrated Digital Health Ecosystems

Modern consumers expect portable, integrated health data, forcing LetsGetChecked to build high-quality APIs and interoperability-costs that weighed on tech and R&D spending as the company expanded in 2025.

In 2025, 68% of US telehealth users cited data portability as a key feature; failing to meet this norm risks churn and lower lifetime value.

Customers treat seamless integration as standard, not premium, raising bargaining power and pressuring LetsGetChecked's margins as it funds integrations with EHRs and third-party apps.

- 68% of US telehealth users want data portability (2025)

- Integration increases R&D/API costs, pressuring margins in 2025

- Seamless data seen as standard-raises customer bargaining power

Pricing constrained: high customer bargaining, enterprise swings & insurer caps

Customers hold high bargaining power: low switching costs and price sensitivity (68% favor price) limit LetsGetChecked's pricing; FY2025 ARPT $58, marketing spend $72M, enterprise buyers (~40% revenue) can swing $25-40M per quarter, and insurer gatekeepers (UnitedHealth ~31M members) set reimbursement that caps margins.

| Metric | Value (FY2025) |

|---|---|

| ARPT | $58 |

| Marketing spend | $72M |

| Enterprise revenue share | ~40% |

| Enterprise swing/quarter | $25-40M |

| Price sensitivity | 68% |

| UnitedHealth members | ~31M |

Full Version Awaits

LetsGetChecked Porter's Five Forces Analysis

This preview shows the exact LetsGetChecked Porter's Five Forces analysis you'll receive immediately after purchase-no placeholders or mockups, fully formatted and ready for use.

The document covers supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry with clear implications and action points tailored for investors and strategists.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

LetsGetChecked faces intense buyer power and evolving substitute threats as telehealth and at-home testing converge, while supplier leverage and regulatory shifts add complexity to margins and scale-up plans.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore LetsGetChecked's competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Diagnostic Equipment Providers

LetsGetChecked relies on specialized diagnostic machinery from few dominant suppliers like Danaher and Thermo Fisher Scientific, creating high dependency; Danaher and Thermo Fisher reported combined 2025 revenue of about $84.5 billion, underscoring their market heft.

Although LetsGetChecked runs its own labs, instrument switching costs and mandatory maintenance contracts raise total cost of ownership by an estimated 15-25%, locking procurement choices.

Supplier concentration lets manufacturers keep firm pricing: model price increases averaged 3-6% annually through 2024-25 despite rising at‑home test volumes.

Medical Component and Kit Manufacturers

The supply of medical-grade swabs, collection tubes, and lancets for LetsGetChecked faced global disruptions in 2024-25; FDA-quality validation raised switching costs, with supplier lead times up 35% and spot prices up ~18% in FY2025, giving established manufacturers moderate pricing and delivery leverage.

Logistics and Cold Chain Carriers

LetsGetChecked relies on UPS and FedEx for temperature-controlled, time-sensitive sample transport; in 2025 these carriers handle ~80-90% of US next-day medical shipments, giving them outsized leverage.

Few national alternatives meet diagnostic cold-chain specs, so carriers' pricing shifts-fuel surcharges rose ~18% in 2024-25-directly compress LetsGetChecked's margins with limited negotiation room.

Specialized Medical and Lab Personnel

Scarcity of licensed clinical laboratory scientists and board-certified physicians creates a talent-driven supply constraint for LetsGetChecked, with US vacancy rates for clinical lab roles near 12% in 2025 and median MLS wages up 8% y/y to $76,000.

Ongoing healthcare labor shortages through 2025 keep retention costs high; physician review stipends and benefits raised provider costs ~10-15% versus 2023 benchmarks.

This human capital underpins service quality, giving suppliers bargaining power manifested in rising wages, signing bonuses, and demand for flexible schedules.

- 12% vacancy rate for clinical lab roles (2025)

- Median MLS wage $76,000 (2025, +8% y/y)

- Provider cost pressure +10-15% vs 2023

- Higher signing bonuses and benefits required

Cloud Infrastructure and Cybersecurity Vendors

Managing sensitive patient data forces LetsGetChecked to use HIPAA-compliant cloud services like Amazon Web Services or Microsoft Azure, which together held ~66% of global cloud IaaS/PaaS market in 2025, limiting bargaining power.

Their standardized pricing and limited discounting for mid-sized health techs, plus switching costs-data egress fees up to $0.09/GB and migration projects often >$1M-create vendor lock-in favoring providers.

Bullets:

- AWS+Azure ~66% IaaS/PaaS share (2025)

- Data egress up to $0.09/GB

- Typical migration >$1M

- HIPAA compliance required, few alternative vendors

Concentrated suppliers drive costs up: instruments, carriers, cloud, and talent shortages

Suppliers exert moderate‑high power: concentrated instrument vendors (Danaher/Thermo Fisher combined revenue $84.5B in 2025), logistics carriers (UPS/FedEx ~80-90% US medical next‑day), cloud providers (AWS+Azure ~66% IaaS/PaaS) and talent shortages (12% lab vacancy; median MLS $76,000) raise costs and switching barriers.

| Category | 2025 Metric |

|---|---|

| Instrument vendors | $84.5B combined revenue |

| Carriers | 80-90% US medical next‑day |

| Cloud | 66% IaaS/PaaS |

| Lab talent | 12% vacancy; $76,000 median |

What is included in the product

Tailored exclusively for LetsGetChecked, this Porter's Five Forces overview uncovers competitive pressures, customer and supplier influence, threats from substitutes and new entrants, and highlights disruptive forces shaping pricing, margins, and market positioning.

Clear, one-sheet Porter's Five Forces for LetsGetChecked-fast-strategic insights to spot competitive threats and relief points for product, pricing, and partnership decisions.

Customers Bargaining Power

Low Switching Costs for Individual Consumers

In LetsGetChecked's direct-to-consumer segment, switching costs are minimal-patients face virtually no fees to move to Everlywell or Thirty-Two Labs, so price and convenience dominate purchase decisions.

Most diagnostic tests are one-off buys, not subscriptions, so brand loyalty is limited; 2024 market surveys show 68% of consumers prioritize price when selecting at-home tests.

That dynamic forced LetsGetChecked to spend an estimated $72M on marketing in FY2025 to maintain share and improve UX, since customers can compare prices and reviews instantly online.

Bargaining Leverage of Large Employer Groups

Large employer groups drive ~40% of LetsGetChecked's 2025 revenue and exert strong bargaining power, securing volume discounts and bespoke dashboards; a single lost enterprise (often thousands of users) can swing quarterly revenue by an estimated $25-40M, so buyers can push pricing and SLA concessions that shift negotiating leverage toward employers.

Transparency in Market Pricing

The digital at-home testing market lets consumers compare prices instantly, driving price transparency; LetsGetChecked reported average revenue per test of $58 in FY2025, aligning with market medians and constraining unilateral price hikes.

Influence of Health Insurance Providers

As LetsGetChecked pursues deeper ties with insurers, payers like UnitedHealth (2025 revenue $356B) and CVS Health/Aetna ($322B) control reimbursement rates and membership access, making their approval pivotal for growth.

If insurers deny coverage, typical out-of-pocket fees-$49-$199 per at-home test-drive patients back to covered clinic labs.

- Insurer gatekeeping: controls millions-UnitedHealth 2025 members ~31M

- Reimbursement sets price: limits margin on $49-$199 tests

- Coverage denial increases out-of-pocket churn

Demand for Integrated Digital Health Ecosystems

Modern consumers expect portable, integrated health data, forcing LetsGetChecked to build high-quality APIs and interoperability-costs that weighed on tech and R&D spending as the company expanded in 2025.

In 2025, 68% of US telehealth users cited data portability as a key feature; failing to meet this norm risks churn and lower lifetime value.

Customers treat seamless integration as standard, not premium, raising bargaining power and pressuring LetsGetChecked's margins as it funds integrations with EHRs and third-party apps.

- 68% of US telehealth users want data portability (2025)

- Integration increases R&D/API costs, pressuring margins in 2025

- Seamless data seen as standard-raises customer bargaining power

Pricing constrained: high customer bargaining, enterprise swings & insurer caps

Customers hold high bargaining power: low switching costs and price sensitivity (68% favor price) limit LetsGetChecked's pricing; FY2025 ARPT $58, marketing spend $72M, enterprise buyers (~40% revenue) can swing $25-40M per quarter, and insurer gatekeepers (UnitedHealth ~31M members) set reimbursement that caps margins.

| Metric | Value (FY2025) |

|---|---|

| ARPT | $58 |

| Marketing spend | $72M |

| Enterprise revenue share | ~40% |

| Enterprise swing/quarter | $25-40M |

| Price sensitivity | 68% |

| UnitedHealth members | ~31M |

Full Version Awaits

LetsGetChecked Porter's Five Forces Analysis

This preview shows the exact LetsGetChecked Porter's Five Forces analysis you'll receive immediately after purchase-no placeholders or mockups, fully formatted and ready for use.

The document covers supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry with clear implications and action points tailored for investors and strategists.