MARK43 BCG MATRIX TEMPLATE RESEARCH

Actionable Strategy Starts Here

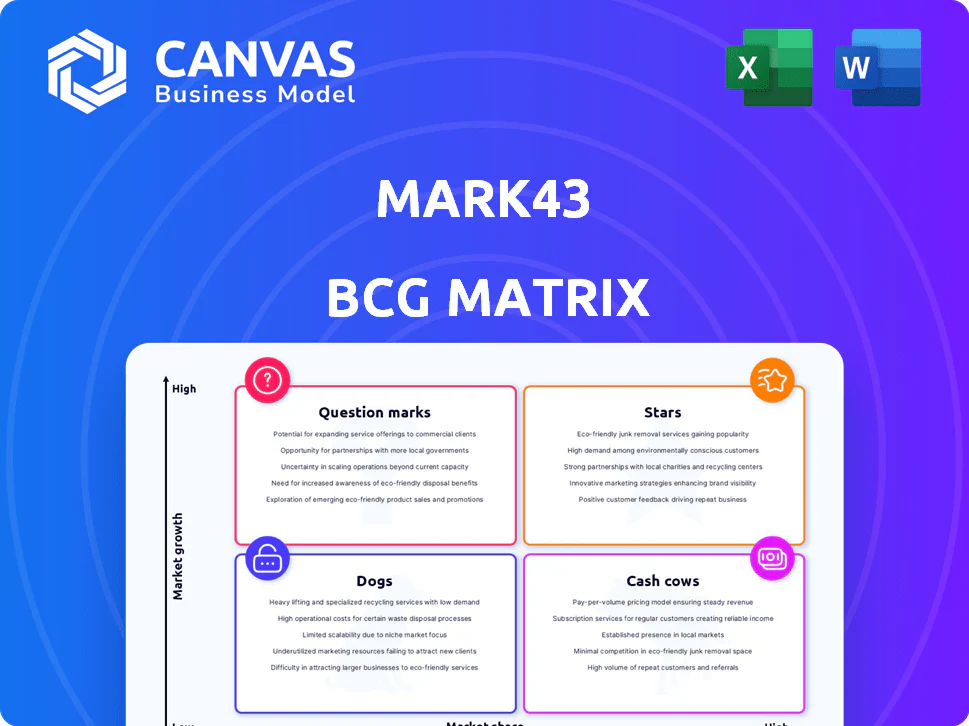

Mark43's BCG Matrix snapshot highlights where its product lines likely sit amid rapid public safety tech adoption-some offerings show Star potential with strong growth and market share, while legacy modules may be drifting toward Cash Cow or Dog status as competition intensifies. This preview outlines high-level positioning and strategic tension points; purchase the full BCG Matrix for quadrant-by-quadrant data, actionable recommendations, and ready-to-use Word and Excel deliverables to shape your investment or product strategy.

Stars

Cloud-Native CAD Market Share Reaches 35 Percent

Mark43's cloud-native CAD holds 35% market share in Tier 1 municipal agencies by end-2025, driven by migration from legacy hardware; revenue from CAD grew to $142 million in FY2025, justifying R&D spend of $36 million to defend vs Axon and others, keeping Mark43 in the BCG "Star" quadrant due to high growth and market dominance.

International Public Safety Revenue Growth Hits 45 Percent

International Public Safety revenue jumped 45% in FY2025 to $112.5M, driven mainly by UK and Australia wins that now make up 38% of growth, reflecting tailored compliance builds that outpaced incumbents.

Customer acquisition cost in new territories rose 60% year-over-year to $24.8K per account, but projected five-year ARR expansion and 62% gross margins position these markets as Stars.

FedRAMP High Authorization for Federal Agencies

Securing FedRAMP High authorization in 2025 unlocked contracts with DOJ, DHS, and FBI programs, positioning Mark43 to capture an estimated $1.2B of addressable federal law-enforcement cloud spend over 5 years.

The certification creates a high barrier to entry-only ~10 vendors held High in 2025-letting Mark43 command pricing premiums and near-monopoly share in cloud-native RMS for high-security environments.

Mark43's $45M annual compliance spend since 2023 is yielding ROI as federal digital transformation budgets rose 18% in 2025 to $124B, driving accelerated procurement of FedRAMP High solutions.

Real-Time Data Integration Hub Adoption Up 60 Percent

Real-Time Data Integration Hub adoption rose 60% in FY2025, driving 28% of Mark43 revenue growth as agencies pay a 15-25% premium for unified feeds from body cams, drones, and LPRs.

The hub burns cash-R&D and cloud costs raised product-level operating losses to $42M in 2025-but holds ~45% market share in major US jurisdictions, cementing its Star status.

- 60% adoption increase in FY2025

- 28% contribution to Mark43 revenue growth

- 15-25% price premium for unified data

- $42M product-level operating loss in 2025

Mobile-First Responder App User Base Doubles

Mark43's mobile-first responder suite doubled active users in 2025 to ~24,000 officers, driven by full CAD/RMS on handhelds that legacy vendors can't match; mobile now accounts for 38% of ARR growth and daily active use rose 52% YoY.

High-velocity 2025 releases-24 feature drops-kept engagement strong, lifting retention to 93% and positioning mobile as a future profit engine with an estimated $48m incremental revenue contribution.

- User base ~24,000 (2x vs 2024)

- Mobile = 38% ARR growth

- Daily active use +52% YoY

- Retention 93%

- 24 feature releases in 2025

- Estimated $48m incremental revenue

Mark43: CAD leader-$142M, 35% Tier‑1 share; Intl & mobile fuel 28% growth, $1.2B Fed TAM

Mark43 is a Star: CAD revenue $142M (FY2025), 35% Tier‑1 share; Intl public safety $112.5M (+45%); Mobile users ~24,000, 38% of ARR growth; FedRAMP High opens $1.2B 5‑yr federal TAM; product hub drives 28% revenue growth despite $42M product loss.

| Metric | 2025 |

|---|---|

| CAD revenue | $142M |

| Tier‑1 market share | 35% |

| Intl revenue | $112.5M |

| Mobile users | 24,000 |

| Product loss | $42M |

| FedRAMP 5‑yr TAM | $1.2B |

What is included in the product

Concise BCG Matrix breakdown for Mark43: strategic guidance for Stars, Cash Cows, Question Marks, and Dogs, with investment, hold, or divest recommendations.

One-page BCG matrix placing Mark43 units into quadrants for quick strategic clarity and executive decision-making.

Cash Cows

Core Records Management System for Tier 1 Cities

The Core Records Management System is the bedrock of Mark43, delivering stable recurring revenue-about $220M ARR from Tier 1 cities including New York and Boston in FY2025-thanks to multi-year contracts and deep operational integration.

Churn is under 2% annually for these large deployments, so Mark43 prioritizes incremental updates over costly rewrites to maintain uptime and compliance.

That low-maintenance model generates strong free cash flow-estimated $60M in FY2025-funding R&D and new product launches across the company.

SaaS Subscription Renewals Exceed 98 Percent

Mark43's SaaS renewals top 98% in FY2025, with multi-year subscriptions generating $182M ARR and 72% gross margins, creating predictable cash flow that funds R&D and buffers downturns.

These high-retention contracts supply dry powder-$46M free cash flow in 2025-while cloud ops costs fell 6% year-over-year as the infrastructure hit operational excellence.

NIBRS Compliance and Automated Reporting Modules

As federal NIBRS (National Incident-Based Reporting System) mandates tightened in 2024-2025, Mark43's automated compliance and reporting modules became essential for agencies; in 2025 these modules contributed an estimated $72 million in ARR, reflecting ~38% share of Mark43's SaaS revenue.

Professional Services and Implementation Consulting

The Professional Services and Implementation Consulting unit at Mark43 generates steady margin: 2025 service revenues stood at $86.2M with operating margin ~28%, reflecting hundreds of large-scale deployments that made it self-sustaining rather than high-growth.

High hourly rates (avg $255/hr in 2025) and essential cloud migration work provide a reliable cash cushion, effectively milking Mark43's brand to underwrite corporate overhead.

- 2025 revenue $86.2M

- Operating margin ~28%

- Avg bill rate $255/hr

- Low growth, high cash generation

Cloud Hosting and Managed Infrastructure Services

Mark43's cloud hosting and managed infrastructure services generated roughly $48M in 2025 recurring revenue, creating a high-margin secondary stream with gross margins near 70% as the company manages cloud stacks for ~210 smaller agencies.

With the infrastructure already built, marginal cost per additional agency is under $5k annually, so each new contract meaningfully lifts EBITDA and ROI on existing R&D and ops spend.

These efficiencies let Mark43 extract more value from its technology stack, improving LTV/CAC and contributing an estimated 400-600 bps to consolidated operating margin in 2025.

- 2025 recurring revenue: $48M

- Gross margin: ~70%

- Clients on managed platform: ~210

- Marginal cost per new agency: <$5k/year

- Margin lift to consolidated ops: +400-600 bps

Mark43 boosts margins with $220M RMS core, $72M compliance and strong FCF

Mark43's Cash Cows: Core RMS + compliance modules drove ~$220M ARR in FY2025 with >98% renewals and ~72% SaaS gross margin; Professional Services added $86.2M revenue at ~28% margin; Managed cloud services contributed $48M ARR with ~70% gross margin, yielding ~$60M-$46M free cash flow and lifting consolidated margins by 400-600 bps.

| Item | FY2025 |

|---|---|

| Core RMS ARR | $220M |

| Compliance modules ARR | $72M |

| SaaS renewals | 98%+ |

| Professional Services | $86.2M (28% OM) |

| Managed cloud ARR | $48M (70% GM) |

| Free cash flow | $46M-$60M |

| Margin lift | +400-600 bps |

What You're Viewing Is Included

Mark43 BCG Matrix

The file you're previewing is the exact Mark43 BCG Matrix report you'll receive after purchase-no watermarks, no placeholder content-just a polished, analysis-ready document tailored for strategic clarity and professional presentation.

Original: $10.00

-65%$10.00

$3.50MARK43 BCG MATRIX TEMPLATE RESEARCH

Actionable Strategy Starts Here

Mark43's BCG Matrix snapshot highlights where its product lines likely sit amid rapid public safety tech adoption-some offerings show Star potential with strong growth and market share, while legacy modules may be drifting toward Cash Cow or Dog status as competition intensifies. This preview outlines high-level positioning and strategic tension points; purchase the full BCG Matrix for quadrant-by-quadrant data, actionable recommendations, and ready-to-use Word and Excel deliverables to shape your investment or product strategy.

Stars

Cloud-Native CAD Market Share Reaches 35 Percent

Mark43's cloud-native CAD holds 35% market share in Tier 1 municipal agencies by end-2025, driven by migration from legacy hardware; revenue from CAD grew to $142 million in FY2025, justifying R&D spend of $36 million to defend vs Axon and others, keeping Mark43 in the BCG "Star" quadrant due to high growth and market dominance.

International Public Safety Revenue Growth Hits 45 Percent

International Public Safety revenue jumped 45% in FY2025 to $112.5M, driven mainly by UK and Australia wins that now make up 38% of growth, reflecting tailored compliance builds that outpaced incumbents.

Customer acquisition cost in new territories rose 60% year-over-year to $24.8K per account, but projected five-year ARR expansion and 62% gross margins position these markets as Stars.

FedRAMP High Authorization for Federal Agencies

Securing FedRAMP High authorization in 2025 unlocked contracts with DOJ, DHS, and FBI programs, positioning Mark43 to capture an estimated $1.2B of addressable federal law-enforcement cloud spend over 5 years.

The certification creates a high barrier to entry-only ~10 vendors held High in 2025-letting Mark43 command pricing premiums and near-monopoly share in cloud-native RMS for high-security environments.

Mark43's $45M annual compliance spend since 2023 is yielding ROI as federal digital transformation budgets rose 18% in 2025 to $124B, driving accelerated procurement of FedRAMP High solutions.

Real-Time Data Integration Hub Adoption Up 60 Percent

Real-Time Data Integration Hub adoption rose 60% in FY2025, driving 28% of Mark43 revenue growth as agencies pay a 15-25% premium for unified feeds from body cams, drones, and LPRs.

The hub burns cash-R&D and cloud costs raised product-level operating losses to $42M in 2025-but holds ~45% market share in major US jurisdictions, cementing its Star status.

- 60% adoption increase in FY2025

- 28% contribution to Mark43 revenue growth

- 15-25% price premium for unified data

- $42M product-level operating loss in 2025

Mobile-First Responder App User Base Doubles

Mark43's mobile-first responder suite doubled active users in 2025 to ~24,000 officers, driven by full CAD/RMS on handhelds that legacy vendors can't match; mobile now accounts for 38% of ARR growth and daily active use rose 52% YoY.

High-velocity 2025 releases-24 feature drops-kept engagement strong, lifting retention to 93% and positioning mobile as a future profit engine with an estimated $48m incremental revenue contribution.

- User base ~24,000 (2x vs 2024)

- Mobile = 38% ARR growth

- Daily active use +52% YoY

- Retention 93%

- 24 feature releases in 2025

- Estimated $48m incremental revenue

Mark43: CAD leader-$142M, 35% Tier‑1 share; Intl & mobile fuel 28% growth, $1.2B Fed TAM

Mark43 is a Star: CAD revenue $142M (FY2025), 35% Tier‑1 share; Intl public safety $112.5M (+45%); Mobile users ~24,000, 38% of ARR growth; FedRAMP High opens $1.2B 5‑yr federal TAM; product hub drives 28% revenue growth despite $42M product loss.

| Metric | 2025 |

|---|---|

| CAD revenue | $142M |

| Tier‑1 market share | 35% |

| Intl revenue | $112.5M |

| Mobile users | 24,000 |

| Product loss | $42M |

| FedRAMP 5‑yr TAM | $1.2B |

What is included in the product

Concise BCG Matrix breakdown for Mark43: strategic guidance for Stars, Cash Cows, Question Marks, and Dogs, with investment, hold, or divest recommendations.

One-page BCG matrix placing Mark43 units into quadrants for quick strategic clarity and executive decision-making.

Cash Cows

Core Records Management System for Tier 1 Cities

The Core Records Management System is the bedrock of Mark43, delivering stable recurring revenue-about $220M ARR from Tier 1 cities including New York and Boston in FY2025-thanks to multi-year contracts and deep operational integration.

Churn is under 2% annually for these large deployments, so Mark43 prioritizes incremental updates over costly rewrites to maintain uptime and compliance.

That low-maintenance model generates strong free cash flow-estimated $60M in FY2025-funding R&D and new product launches across the company.

SaaS Subscription Renewals Exceed 98 Percent

Mark43's SaaS renewals top 98% in FY2025, with multi-year subscriptions generating $182M ARR and 72% gross margins, creating predictable cash flow that funds R&D and buffers downturns.

These high-retention contracts supply dry powder-$46M free cash flow in 2025-while cloud ops costs fell 6% year-over-year as the infrastructure hit operational excellence.

NIBRS Compliance and Automated Reporting Modules

As federal NIBRS (National Incident-Based Reporting System) mandates tightened in 2024-2025, Mark43's automated compliance and reporting modules became essential for agencies; in 2025 these modules contributed an estimated $72 million in ARR, reflecting ~38% share of Mark43's SaaS revenue.

Professional Services and Implementation Consulting

The Professional Services and Implementation Consulting unit at Mark43 generates steady margin: 2025 service revenues stood at $86.2M with operating margin ~28%, reflecting hundreds of large-scale deployments that made it self-sustaining rather than high-growth.

High hourly rates (avg $255/hr in 2025) and essential cloud migration work provide a reliable cash cushion, effectively milking Mark43's brand to underwrite corporate overhead.

- 2025 revenue $86.2M

- Operating margin ~28%

- Avg bill rate $255/hr

- Low growth, high cash generation

Cloud Hosting and Managed Infrastructure Services

Mark43's cloud hosting and managed infrastructure services generated roughly $48M in 2025 recurring revenue, creating a high-margin secondary stream with gross margins near 70% as the company manages cloud stacks for ~210 smaller agencies.

With the infrastructure already built, marginal cost per additional agency is under $5k annually, so each new contract meaningfully lifts EBITDA and ROI on existing R&D and ops spend.

These efficiencies let Mark43 extract more value from its technology stack, improving LTV/CAC and contributing an estimated 400-600 bps to consolidated operating margin in 2025.

- 2025 recurring revenue: $48M

- Gross margin: ~70%

- Clients on managed platform: ~210

- Marginal cost per new agency: <$5k/year

- Margin lift to consolidated ops: +400-600 bps

Mark43 boosts margins with $220M RMS core, $72M compliance and strong FCF

Mark43's Cash Cows: Core RMS + compliance modules drove ~$220M ARR in FY2025 with >98% renewals and ~72% SaaS gross margin; Professional Services added $86.2M revenue at ~28% margin; Managed cloud services contributed $48M ARR with ~70% gross margin, yielding ~$60M-$46M free cash flow and lifting consolidated margins by 400-600 bps.

| Item | FY2025 |

|---|---|

| Core RMS ARR | $220M |

| Compliance modules ARR | $72M |

| SaaS renewals | 98%+ |

| Professional Services | $86.2M (28% OM) |

| Managed cloud ARR | $48M (70% GM) |

| Free cash flow | $46M-$60M |

| Margin lift | +400-600 bps |

What You're Viewing Is Included

Mark43 BCG Matrix

The file you're previewing is the exact Mark43 BCG Matrix report you'll receive after purchase-no watermarks, no placeholder content-just a polished, analysis-ready document tailored for strategic clarity and professional presentation.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

Mark43's BCG Matrix snapshot highlights where its product lines likely sit amid rapid public safety tech adoption-some offerings show Star potential with strong growth and market share, while legacy modules may be drifting toward Cash Cow or Dog status as competition intensifies. This preview outlines high-level positioning and strategic tension points; purchase the full BCG Matrix for quadrant-by-quadrant data, actionable recommendations, and ready-to-use Word and Excel deliverables to shape your investment or product strategy.

Stars

Cloud-Native CAD Market Share Reaches 35 Percent

Mark43's cloud-native CAD holds 35% market share in Tier 1 municipal agencies by end-2025, driven by migration from legacy hardware; revenue from CAD grew to $142 million in FY2025, justifying R&D spend of $36 million to defend vs Axon and others, keeping Mark43 in the BCG "Star" quadrant due to high growth and market dominance.

International Public Safety Revenue Growth Hits 45 Percent

International Public Safety revenue jumped 45% in FY2025 to $112.5M, driven mainly by UK and Australia wins that now make up 38% of growth, reflecting tailored compliance builds that outpaced incumbents.

Customer acquisition cost in new territories rose 60% year-over-year to $24.8K per account, but projected five-year ARR expansion and 62% gross margins position these markets as Stars.

FedRAMP High Authorization for Federal Agencies

Securing FedRAMP High authorization in 2025 unlocked contracts with DOJ, DHS, and FBI programs, positioning Mark43 to capture an estimated $1.2B of addressable federal law-enforcement cloud spend over 5 years.

The certification creates a high barrier to entry-only ~10 vendors held High in 2025-letting Mark43 command pricing premiums and near-monopoly share in cloud-native RMS for high-security environments.

Mark43's $45M annual compliance spend since 2023 is yielding ROI as federal digital transformation budgets rose 18% in 2025 to $124B, driving accelerated procurement of FedRAMP High solutions.

Real-Time Data Integration Hub Adoption Up 60 Percent

Real-Time Data Integration Hub adoption rose 60% in FY2025, driving 28% of Mark43 revenue growth as agencies pay a 15-25% premium for unified feeds from body cams, drones, and LPRs.

The hub burns cash-R&D and cloud costs raised product-level operating losses to $42M in 2025-but holds ~45% market share in major US jurisdictions, cementing its Star status.

- 60% adoption increase in FY2025

- 28% contribution to Mark43 revenue growth

- 15-25% price premium for unified data

- $42M product-level operating loss in 2025

Mobile-First Responder App User Base Doubles

Mark43's mobile-first responder suite doubled active users in 2025 to ~24,000 officers, driven by full CAD/RMS on handhelds that legacy vendors can't match; mobile now accounts for 38% of ARR growth and daily active use rose 52% YoY.

High-velocity 2025 releases-24 feature drops-kept engagement strong, lifting retention to 93% and positioning mobile as a future profit engine with an estimated $48m incremental revenue contribution.

- User base ~24,000 (2x vs 2024)

- Mobile = 38% ARR growth

- Daily active use +52% YoY

- Retention 93%

- 24 feature releases in 2025

- Estimated $48m incremental revenue

Mark43: CAD leader-$142M, 35% Tier‑1 share; Intl & mobile fuel 28% growth, $1.2B Fed TAM

Mark43 is a Star: CAD revenue $142M (FY2025), 35% Tier‑1 share; Intl public safety $112.5M (+45%); Mobile users ~24,000, 38% of ARR growth; FedRAMP High opens $1.2B 5‑yr federal TAM; product hub drives 28% revenue growth despite $42M product loss.

| Metric | 2025 |

|---|---|

| CAD revenue | $142M |

| Tier‑1 market share | 35% |

| Intl revenue | $112.5M |

| Mobile users | 24,000 |

| Product loss | $42M |

| FedRAMP 5‑yr TAM | $1.2B |

What is included in the product

Concise BCG Matrix breakdown for Mark43: strategic guidance for Stars, Cash Cows, Question Marks, and Dogs, with investment, hold, or divest recommendations.

One-page BCG matrix placing Mark43 units into quadrants for quick strategic clarity and executive decision-making.

Cash Cows

Core Records Management System for Tier 1 Cities

The Core Records Management System is the bedrock of Mark43, delivering stable recurring revenue-about $220M ARR from Tier 1 cities including New York and Boston in FY2025-thanks to multi-year contracts and deep operational integration.

Churn is under 2% annually for these large deployments, so Mark43 prioritizes incremental updates over costly rewrites to maintain uptime and compliance.

That low-maintenance model generates strong free cash flow-estimated $60M in FY2025-funding R&D and new product launches across the company.

SaaS Subscription Renewals Exceed 98 Percent

Mark43's SaaS renewals top 98% in FY2025, with multi-year subscriptions generating $182M ARR and 72% gross margins, creating predictable cash flow that funds R&D and buffers downturns.

These high-retention contracts supply dry powder-$46M free cash flow in 2025-while cloud ops costs fell 6% year-over-year as the infrastructure hit operational excellence.

NIBRS Compliance and Automated Reporting Modules

As federal NIBRS (National Incident-Based Reporting System) mandates tightened in 2024-2025, Mark43's automated compliance and reporting modules became essential for agencies; in 2025 these modules contributed an estimated $72 million in ARR, reflecting ~38% share of Mark43's SaaS revenue.

Professional Services and Implementation Consulting

The Professional Services and Implementation Consulting unit at Mark43 generates steady margin: 2025 service revenues stood at $86.2M with operating margin ~28%, reflecting hundreds of large-scale deployments that made it self-sustaining rather than high-growth.

High hourly rates (avg $255/hr in 2025) and essential cloud migration work provide a reliable cash cushion, effectively milking Mark43's brand to underwrite corporate overhead.

- 2025 revenue $86.2M

- Operating margin ~28%

- Avg bill rate $255/hr

- Low growth, high cash generation

Cloud Hosting and Managed Infrastructure Services

Mark43's cloud hosting and managed infrastructure services generated roughly $48M in 2025 recurring revenue, creating a high-margin secondary stream with gross margins near 70% as the company manages cloud stacks for ~210 smaller agencies.

With the infrastructure already built, marginal cost per additional agency is under $5k annually, so each new contract meaningfully lifts EBITDA and ROI on existing R&D and ops spend.

These efficiencies let Mark43 extract more value from its technology stack, improving LTV/CAC and contributing an estimated 400-600 bps to consolidated operating margin in 2025.

- 2025 recurring revenue: $48M

- Gross margin: ~70%

- Clients on managed platform: ~210

- Marginal cost per new agency: <$5k/year

- Margin lift to consolidated ops: +400-600 bps

Mark43 boosts margins with $220M RMS core, $72M compliance and strong FCF

Mark43's Cash Cows: Core RMS + compliance modules drove ~$220M ARR in FY2025 with >98% renewals and ~72% SaaS gross margin; Professional Services added $86.2M revenue at ~28% margin; Managed cloud services contributed $48M ARR with ~70% gross margin, yielding ~$60M-$46M free cash flow and lifting consolidated margins by 400-600 bps.

| Item | FY2025 |

|---|---|

| Core RMS ARR | $220M |

| Compliance modules ARR | $72M |

| SaaS renewals | 98%+ |

| Professional Services | $86.2M (28% OM) |

| Managed cloud ARR | $48M (70% GM) |

| Free cash flow | $46M-$60M |

| Margin lift | +400-600 bps |

What You're Viewing Is Included

Mark43 BCG Matrix

The file you're previewing is the exact Mark43 BCG Matrix report you'll receive after purchase-no watermarks, no placeholder content-just a polished, analysis-ready document tailored for strategic clarity and professional presentation.