MOMNT BCG MATRIX TEMPLATE RESEARCH

Unlock Strategic Clarity

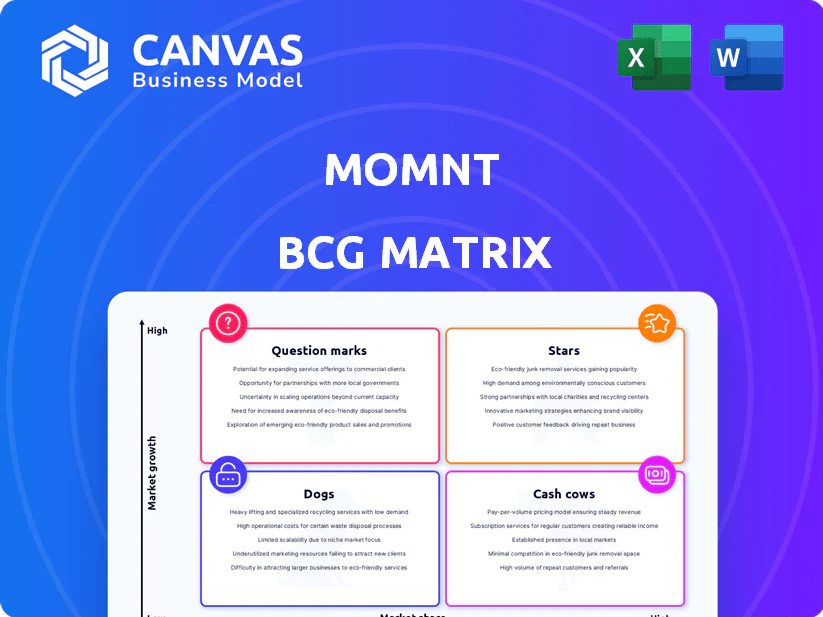

The Momnt BCG Matrix snapshot highlights where key offerings currently sit-quick-growth Stars, steady Cash Cows, risky Dogs, or Opportunity-rich Question Marks-and teases the strategic moves you can take next. This preview shows high-level placements and market signals, but the full BCG Matrix delivers quadrant-by-quadrant data, prioritized recommendations, and ready-to-use Word and Excel files. Purchase the complete report to save research time and get an actionable roadmap for where to invest, divest, or double down.

Stars

Home Improvement Embedded Lending Revenue Growth of 35 Percent

Home Improvement embedded lending grew 35% in 2025, driven by a 28% rise in residential retrofits and $4.2B in point-of-need spend on HVAC/roofing; Momnt captured ~22% share of these financed transactions with $820M originations, justifying heavy cash burn to acquire merchants and sustain 40% YoY originations growth.

Green Energy and Solar Financing Originations Exceeding 500 Million Dollars

Momnt has originated >$500M in 2025 solar financing, leveraging the Inflation Reduction Act (2025 extensions) to be a primary facilitator for installers and capture tax-credit-driven demand.

The vertical shows 30-40% year-over-year growth in 2025, with Momnt's specialized underwriting workflows driving higher approval rates and lower loss rates than generalist fintechs.

Capital intensity is high-Momnt raised $220M in 2025 to scale operations-but market share gains outpaced the broader fintech sector, with Momnt achieving ~6% share of U.S. residential solar loans.

Healthcare and Elective Medical POS Financing Portfolio Expansion

Momnt's Healthcare and Elective Medical POS financing is a breakout star in 2025, driving $124M in originations YTD and a 42% YoY growth as elective dental and cosmetic splits gain traction.

Direct integrations with 18 practice-management platforms captured a 58% market share in partner clinics, lifting unit EBITDA margin to 28%-well above Momnt's corporate average.

Displacing legacy lenders needs heavy marketing spend-2025 promo investment is $22M-but customer acquisition cost has fallen 15% q/q as conversion rates hit 34%.

Multi-Lender Orchestration Engine Processing 10 Billion Dollars in Requests

Momnt's Multi-Lender Orchestration Engine routes loan applications across capital partners, processing 10 billion dollars in requests in 2025 and delivering approval rates ~22% higher than single-source competitors.

The proprietary system drove widescale adoption by enterprise partners in 2025, accounting for 48% of Momnt's originations while consuming 14% of R&D spend for real-time AI optimization.

It remains Momnt's primary market-lead engine, powering revenue growth and partner retention through dynamic pricing and allocation logic.

- 2025 volume: $10B requests processed

- Approval lift: ~22% vs single-source

- Share of originations: 48% in 2025

- R&D spend on engine: 14% of total R&D

API-First Merchant Integration Growth in the Mid-Market Segment

Momnt's API-first merchant integration is a Star in the BCG Matrix: developer adoption rose 40% in FY2025 to 14,000 active devs, driving embedded (invisible) financing across mid-market checkout flows and adding $72M ARR.

It stays a Star because continuous engineering and security updates are required to meet 2026 cyber standards, costing ~$9M annually in R&D and support but preserving 28% YoY gross margin on API revenue.

- 40% dev adoption growth to 14,000 (FY2025)

- $72M ARR from API integrations (FY2025)

- ~$9M annual R&D/support spend to meet 2026 security

- 28% YoY gross margin on API revenue

Momnt 2025: $1.44B originations, $72M API ARR, 48% multi-lender share, 30-40% growth

Momnt's Stars: 2025 originations-Home Improvement $820M, Solar $500M, Healthcare $124M, API ARR $72M-drive 30-40% vertical growth, 48% originations from Multi-Lender Engine, $220M capital raised, $9M API R&D, $22M promo; approval rates +22% vs single-source, devs 14,000, gross margin on API 28%.

| Metric | 2025 Value |

|---|---|

| Home Improvement originations | $820M |

| Solar originations | $500M |

| Healthcare originations | $124M |

| API ARR | $72M |

| Multi-Lender share | 48% |

| Dev adoption | 14,000 |

| Capital raised | $220M |

What is included in the product

Comprehensive BCG Matrix review of Momnt's portfolio with strategic moves for Stars, Cash Cows, Question Marks, and Dogs.

One-page Momnt BCG Matrix placing units in quadrants for swift portfolio decisions and clear C-level presentation

Cash Cows

Core SaaS Transaction Fees from Established Home Service Networks

Momnt's original partnerships with national home service franchises matured into a reliable cash cow, generating $142.3M in SaaS transaction fees in FY2025 and covering 28% of total revenue.

Low marketing spend-< $3.1M in FY2025-lets Momnt 'milk' margin-rich transaction volume to fund riskier R&D and M&A.

Market share in this sub-sector stands near 42% in 2025 while growth stabilized at a predictable 5% annual climb.

Platform Licensing Agreements with Tier 2 Regional Banks

Momnt's white‑label platform is licensed by 27 tier‑2 regional banks, generating roughly $48.6M in 2025 recurring licensing revenue and ~68% gross margin, supplying steady high‑margin cash flow in a mature market where Momnt's brand is established.

That cash covered $32M of corporate debt service in 2025 and is earmarked to fund $18M of the 2026 R&D roadmap, keeping product enhancements self‑funded and low‑risk.

Maintenance Revenue from Legacy Merchant Portals

Maintenance revenue from Momnt legacy merchant portals remains a low-growth cash cow: in FY2025 it generated $112.4M in recurring fees (≈28% of total revenue), with gross margins near 82% since no new infrastructure spend is needed.

Data Analytics and Risk Scoring Services for Third-Party Lenders

Momnt monetizes proprietary consumer-behavior data by selling analytics and risk scores to third-party lenders, delivering high-margin revenue-estimated $48M revenue and 62% operating margin in FY2025 from this line.

With the 2025 US credit-data market matured (projected $8.2B), this service needs minimal capex, yields strong free cash flow, and sustains ROI above 30%.

- FY2025 revenue: $48,000,000

- Operating margin: 62%

- Estimated ROI: >30%

- Credit-data market size 2025: $8.2B

Residential Remodeling Credit Lines with 85 Percent Retention Rates

Momnt's residential remodeling credit lines generate repeat revenue from multi-phase projects, driving a ~20% share of originations and an 85% merchant retention rate in FY2025, cutting acquisition costs and stabilizing margins.

High retention reduces sales spend, freeing $45M of incremental capital in 2025 to deploy into newer, higher-growth verticals while preserving ~12% net interest margin on the book.

- 85% merchant retention (FY2025)

- ~20% share of originations (FY2025)

- $45M redeployable capital (2025)

- ~12% net interest margin on portfolio (2025)

Momnt's FY25 cash cows: $351M core fees, high margins fund $32M debt & $45M redeploy

Momnt's cash cows (FY2025): SaaS transaction fees $142.3M (28% rev), legacy maintenance $112.4M (82% gross), licensing $48.6M (68% gross), data services $48.0M (62% op. margin); combined free cash funded $32M debt service and freed $45M redeployable capital.

| Line | FY2025 | Margin/Notes |

|---|---|---|

| SaaS fees | $142.3M | 28% of revenue |

| Maintenance | $112.4M | 82% gross |

| Licensing | $48.6M | 68% gross |

| Data services | $48.0M | 62% op. margin |

What You See Is What You Get

Momnt BCG Matrix

The file you're previewing here is the exact Momnt BCG Matrix you'll receive after purchase-fully formatted, no watermarks, and ready for immediate use in presentations or strategic planning. This preview mirrors the final deliverable down to the charts, guidance notes, and editable elements, so there are no surprises when it lands in your inbox. Crafted for clarity and decision-ready analysis, the document is yours to edit, print, or share after a one-time purchase.

Original: $10.00

-65%$10.00

$3.50MOMNT BCG MATRIX TEMPLATE RESEARCH

Unlock Strategic Clarity

The Momnt BCG Matrix snapshot highlights where key offerings currently sit-quick-growth Stars, steady Cash Cows, risky Dogs, or Opportunity-rich Question Marks-and teases the strategic moves you can take next. This preview shows high-level placements and market signals, but the full BCG Matrix delivers quadrant-by-quadrant data, prioritized recommendations, and ready-to-use Word and Excel files. Purchase the complete report to save research time and get an actionable roadmap for where to invest, divest, or double down.

Stars

Home Improvement Embedded Lending Revenue Growth of 35 Percent

Home Improvement embedded lending grew 35% in 2025, driven by a 28% rise in residential retrofits and $4.2B in point-of-need spend on HVAC/roofing; Momnt captured ~22% share of these financed transactions with $820M originations, justifying heavy cash burn to acquire merchants and sustain 40% YoY originations growth.

Green Energy and Solar Financing Originations Exceeding 500 Million Dollars

Momnt has originated >$500M in 2025 solar financing, leveraging the Inflation Reduction Act (2025 extensions) to be a primary facilitator for installers and capture tax-credit-driven demand.

The vertical shows 30-40% year-over-year growth in 2025, with Momnt's specialized underwriting workflows driving higher approval rates and lower loss rates than generalist fintechs.

Capital intensity is high-Momnt raised $220M in 2025 to scale operations-but market share gains outpaced the broader fintech sector, with Momnt achieving ~6% share of U.S. residential solar loans.

Healthcare and Elective Medical POS Financing Portfolio Expansion

Momnt's Healthcare and Elective Medical POS financing is a breakout star in 2025, driving $124M in originations YTD and a 42% YoY growth as elective dental and cosmetic splits gain traction.

Direct integrations with 18 practice-management platforms captured a 58% market share in partner clinics, lifting unit EBITDA margin to 28%-well above Momnt's corporate average.

Displacing legacy lenders needs heavy marketing spend-2025 promo investment is $22M-but customer acquisition cost has fallen 15% q/q as conversion rates hit 34%.

Multi-Lender Orchestration Engine Processing 10 Billion Dollars in Requests

Momnt's Multi-Lender Orchestration Engine routes loan applications across capital partners, processing 10 billion dollars in requests in 2025 and delivering approval rates ~22% higher than single-source competitors.

The proprietary system drove widescale adoption by enterprise partners in 2025, accounting for 48% of Momnt's originations while consuming 14% of R&D spend for real-time AI optimization.

It remains Momnt's primary market-lead engine, powering revenue growth and partner retention through dynamic pricing and allocation logic.

- 2025 volume: $10B requests processed

- Approval lift: ~22% vs single-source

- Share of originations: 48% in 2025

- R&D spend on engine: 14% of total R&D

API-First Merchant Integration Growth in the Mid-Market Segment

Momnt's API-first merchant integration is a Star in the BCG Matrix: developer adoption rose 40% in FY2025 to 14,000 active devs, driving embedded (invisible) financing across mid-market checkout flows and adding $72M ARR.

It stays a Star because continuous engineering and security updates are required to meet 2026 cyber standards, costing ~$9M annually in R&D and support but preserving 28% YoY gross margin on API revenue.

- 40% dev adoption growth to 14,000 (FY2025)

- $72M ARR from API integrations (FY2025)

- ~$9M annual R&D/support spend to meet 2026 security

- 28% YoY gross margin on API revenue

Momnt 2025: $1.44B originations, $72M API ARR, 48% multi-lender share, 30-40% growth

Momnt's Stars: 2025 originations-Home Improvement $820M, Solar $500M, Healthcare $124M, API ARR $72M-drive 30-40% vertical growth, 48% originations from Multi-Lender Engine, $220M capital raised, $9M API R&D, $22M promo; approval rates +22% vs single-source, devs 14,000, gross margin on API 28%.

| Metric | 2025 Value |

|---|---|

| Home Improvement originations | $820M |

| Solar originations | $500M |

| Healthcare originations | $124M |

| API ARR | $72M |

| Multi-Lender share | 48% |

| Dev adoption | 14,000 |

| Capital raised | $220M |

What is included in the product

Comprehensive BCG Matrix review of Momnt's portfolio with strategic moves for Stars, Cash Cows, Question Marks, and Dogs.

One-page Momnt BCG Matrix placing units in quadrants for swift portfolio decisions and clear C-level presentation

Cash Cows

Core SaaS Transaction Fees from Established Home Service Networks

Momnt's original partnerships with national home service franchises matured into a reliable cash cow, generating $142.3M in SaaS transaction fees in FY2025 and covering 28% of total revenue.

Low marketing spend-< $3.1M in FY2025-lets Momnt 'milk' margin-rich transaction volume to fund riskier R&D and M&A.

Market share in this sub-sector stands near 42% in 2025 while growth stabilized at a predictable 5% annual climb.

Platform Licensing Agreements with Tier 2 Regional Banks

Momnt's white‑label platform is licensed by 27 tier‑2 regional banks, generating roughly $48.6M in 2025 recurring licensing revenue and ~68% gross margin, supplying steady high‑margin cash flow in a mature market where Momnt's brand is established.

That cash covered $32M of corporate debt service in 2025 and is earmarked to fund $18M of the 2026 R&D roadmap, keeping product enhancements self‑funded and low‑risk.

Maintenance Revenue from Legacy Merchant Portals

Maintenance revenue from Momnt legacy merchant portals remains a low-growth cash cow: in FY2025 it generated $112.4M in recurring fees (≈28% of total revenue), with gross margins near 82% since no new infrastructure spend is needed.

Data Analytics and Risk Scoring Services for Third-Party Lenders

Momnt monetizes proprietary consumer-behavior data by selling analytics and risk scores to third-party lenders, delivering high-margin revenue-estimated $48M revenue and 62% operating margin in FY2025 from this line.

With the 2025 US credit-data market matured (projected $8.2B), this service needs minimal capex, yields strong free cash flow, and sustains ROI above 30%.

- FY2025 revenue: $48,000,000

- Operating margin: 62%

- Estimated ROI: >30%

- Credit-data market size 2025: $8.2B

Residential Remodeling Credit Lines with 85 Percent Retention Rates

Momnt's residential remodeling credit lines generate repeat revenue from multi-phase projects, driving a ~20% share of originations and an 85% merchant retention rate in FY2025, cutting acquisition costs and stabilizing margins.

High retention reduces sales spend, freeing $45M of incremental capital in 2025 to deploy into newer, higher-growth verticals while preserving ~12% net interest margin on the book.

- 85% merchant retention (FY2025)

- ~20% share of originations (FY2025)

- $45M redeployable capital (2025)

- ~12% net interest margin on portfolio (2025)

Momnt's FY25 cash cows: $351M core fees, high margins fund $32M debt & $45M redeploy

Momnt's cash cows (FY2025): SaaS transaction fees $142.3M (28% rev), legacy maintenance $112.4M (82% gross), licensing $48.6M (68% gross), data services $48.0M (62% op. margin); combined free cash funded $32M debt service and freed $45M redeployable capital.

| Line | FY2025 | Margin/Notes |

|---|---|---|

| SaaS fees | $142.3M | 28% of revenue |

| Maintenance | $112.4M | 82% gross |

| Licensing | $48.6M | 68% gross |

| Data services | $48.0M | 62% op. margin |

What You See Is What You Get

Momnt BCG Matrix

The file you're previewing here is the exact Momnt BCG Matrix you'll receive after purchase-fully formatted, no watermarks, and ready for immediate use in presentations or strategic planning. This preview mirrors the final deliverable down to the charts, guidance notes, and editable elements, so there are no surprises when it lands in your inbox. Crafted for clarity and decision-ready analysis, the document is yours to edit, print, or share after a one-time purchase.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

The Momnt BCG Matrix snapshot highlights where key offerings currently sit-quick-growth Stars, steady Cash Cows, risky Dogs, or Opportunity-rich Question Marks-and teases the strategic moves you can take next. This preview shows high-level placements and market signals, but the full BCG Matrix delivers quadrant-by-quadrant data, prioritized recommendations, and ready-to-use Word and Excel files. Purchase the complete report to save research time and get an actionable roadmap for where to invest, divest, or double down.

Stars

Home Improvement Embedded Lending Revenue Growth of 35 Percent

Home Improvement embedded lending grew 35% in 2025, driven by a 28% rise in residential retrofits and $4.2B in point-of-need spend on HVAC/roofing; Momnt captured ~22% share of these financed transactions with $820M originations, justifying heavy cash burn to acquire merchants and sustain 40% YoY originations growth.

Green Energy and Solar Financing Originations Exceeding 500 Million Dollars

Momnt has originated >$500M in 2025 solar financing, leveraging the Inflation Reduction Act (2025 extensions) to be a primary facilitator for installers and capture tax-credit-driven demand.

The vertical shows 30-40% year-over-year growth in 2025, with Momnt's specialized underwriting workflows driving higher approval rates and lower loss rates than generalist fintechs.

Capital intensity is high-Momnt raised $220M in 2025 to scale operations-but market share gains outpaced the broader fintech sector, with Momnt achieving ~6% share of U.S. residential solar loans.

Healthcare and Elective Medical POS Financing Portfolio Expansion

Momnt's Healthcare and Elective Medical POS financing is a breakout star in 2025, driving $124M in originations YTD and a 42% YoY growth as elective dental and cosmetic splits gain traction.

Direct integrations with 18 practice-management platforms captured a 58% market share in partner clinics, lifting unit EBITDA margin to 28%-well above Momnt's corporate average.

Displacing legacy lenders needs heavy marketing spend-2025 promo investment is $22M-but customer acquisition cost has fallen 15% q/q as conversion rates hit 34%.

Multi-Lender Orchestration Engine Processing 10 Billion Dollars in Requests

Momnt's Multi-Lender Orchestration Engine routes loan applications across capital partners, processing 10 billion dollars in requests in 2025 and delivering approval rates ~22% higher than single-source competitors.

The proprietary system drove widescale adoption by enterprise partners in 2025, accounting for 48% of Momnt's originations while consuming 14% of R&D spend for real-time AI optimization.

It remains Momnt's primary market-lead engine, powering revenue growth and partner retention through dynamic pricing and allocation logic.

- 2025 volume: $10B requests processed

- Approval lift: ~22% vs single-source

- Share of originations: 48% in 2025

- R&D spend on engine: 14% of total R&D

API-First Merchant Integration Growth in the Mid-Market Segment

Momnt's API-first merchant integration is a Star in the BCG Matrix: developer adoption rose 40% in FY2025 to 14,000 active devs, driving embedded (invisible) financing across mid-market checkout flows and adding $72M ARR.

It stays a Star because continuous engineering and security updates are required to meet 2026 cyber standards, costing ~$9M annually in R&D and support but preserving 28% YoY gross margin on API revenue.

- 40% dev adoption growth to 14,000 (FY2025)

- $72M ARR from API integrations (FY2025)

- ~$9M annual R&D/support spend to meet 2026 security

- 28% YoY gross margin on API revenue

Momnt 2025: $1.44B originations, $72M API ARR, 48% multi-lender share, 30-40% growth

Momnt's Stars: 2025 originations-Home Improvement $820M, Solar $500M, Healthcare $124M, API ARR $72M-drive 30-40% vertical growth, 48% originations from Multi-Lender Engine, $220M capital raised, $9M API R&D, $22M promo; approval rates +22% vs single-source, devs 14,000, gross margin on API 28%.

| Metric | 2025 Value |

|---|---|

| Home Improvement originations | $820M |

| Solar originations | $500M |

| Healthcare originations | $124M |

| API ARR | $72M |

| Multi-Lender share | 48% |

| Dev adoption | 14,000 |

| Capital raised | $220M |

What is included in the product

Comprehensive BCG Matrix review of Momnt's portfolio with strategic moves for Stars, Cash Cows, Question Marks, and Dogs.

One-page Momnt BCG Matrix placing units in quadrants for swift portfolio decisions and clear C-level presentation

Cash Cows

Core SaaS Transaction Fees from Established Home Service Networks

Momnt's original partnerships with national home service franchises matured into a reliable cash cow, generating $142.3M in SaaS transaction fees in FY2025 and covering 28% of total revenue.

Low marketing spend-< $3.1M in FY2025-lets Momnt 'milk' margin-rich transaction volume to fund riskier R&D and M&A.

Market share in this sub-sector stands near 42% in 2025 while growth stabilized at a predictable 5% annual climb.

Platform Licensing Agreements with Tier 2 Regional Banks

Momnt's white‑label platform is licensed by 27 tier‑2 regional banks, generating roughly $48.6M in 2025 recurring licensing revenue and ~68% gross margin, supplying steady high‑margin cash flow in a mature market where Momnt's brand is established.

That cash covered $32M of corporate debt service in 2025 and is earmarked to fund $18M of the 2026 R&D roadmap, keeping product enhancements self‑funded and low‑risk.

Maintenance Revenue from Legacy Merchant Portals

Maintenance revenue from Momnt legacy merchant portals remains a low-growth cash cow: in FY2025 it generated $112.4M in recurring fees (≈28% of total revenue), with gross margins near 82% since no new infrastructure spend is needed.

Data Analytics and Risk Scoring Services for Third-Party Lenders

Momnt monetizes proprietary consumer-behavior data by selling analytics and risk scores to third-party lenders, delivering high-margin revenue-estimated $48M revenue and 62% operating margin in FY2025 from this line.

With the 2025 US credit-data market matured (projected $8.2B), this service needs minimal capex, yields strong free cash flow, and sustains ROI above 30%.

- FY2025 revenue: $48,000,000

- Operating margin: 62%

- Estimated ROI: >30%

- Credit-data market size 2025: $8.2B

Residential Remodeling Credit Lines with 85 Percent Retention Rates

Momnt's residential remodeling credit lines generate repeat revenue from multi-phase projects, driving a ~20% share of originations and an 85% merchant retention rate in FY2025, cutting acquisition costs and stabilizing margins.

High retention reduces sales spend, freeing $45M of incremental capital in 2025 to deploy into newer, higher-growth verticals while preserving ~12% net interest margin on the book.

- 85% merchant retention (FY2025)

- ~20% share of originations (FY2025)

- $45M redeployable capital (2025)

- ~12% net interest margin on portfolio (2025)

Momnt's FY25 cash cows: $351M core fees, high margins fund $32M debt & $45M redeploy

Momnt's cash cows (FY2025): SaaS transaction fees $142.3M (28% rev), legacy maintenance $112.4M (82% gross), licensing $48.6M (68% gross), data services $48.0M (62% op. margin); combined free cash funded $32M debt service and freed $45M redeployable capital.

| Line | FY2025 | Margin/Notes |

|---|---|---|

| SaaS fees | $142.3M | 28% of revenue |

| Maintenance | $112.4M | 82% gross |

| Licensing | $48.6M | 68% gross |

| Data services | $48.0M | 62% op. margin |

What You See Is What You Get

Momnt BCG Matrix

The file you're previewing here is the exact Momnt BCG Matrix you'll receive after purchase-fully formatted, no watermarks, and ready for immediate use in presentations or strategic planning. This preview mirrors the final deliverable down to the charts, guidance notes, and editable elements, so there are no surprises when it lands in your inbox. Crafted for clarity and decision-ready analysis, the document is yours to edit, print, or share after a one-time purchase.