NEUREALITY PORTER'S FIVE FORCES TEMPLATE RESEARCH

What is included in the product

Analyzes NeuReality's competitive landscape: rivals, buyers, suppliers, new entrants, and substitutes.

Prioritize key threats, identifying high-impact factors for swift decision-making.

Same Document Delivered

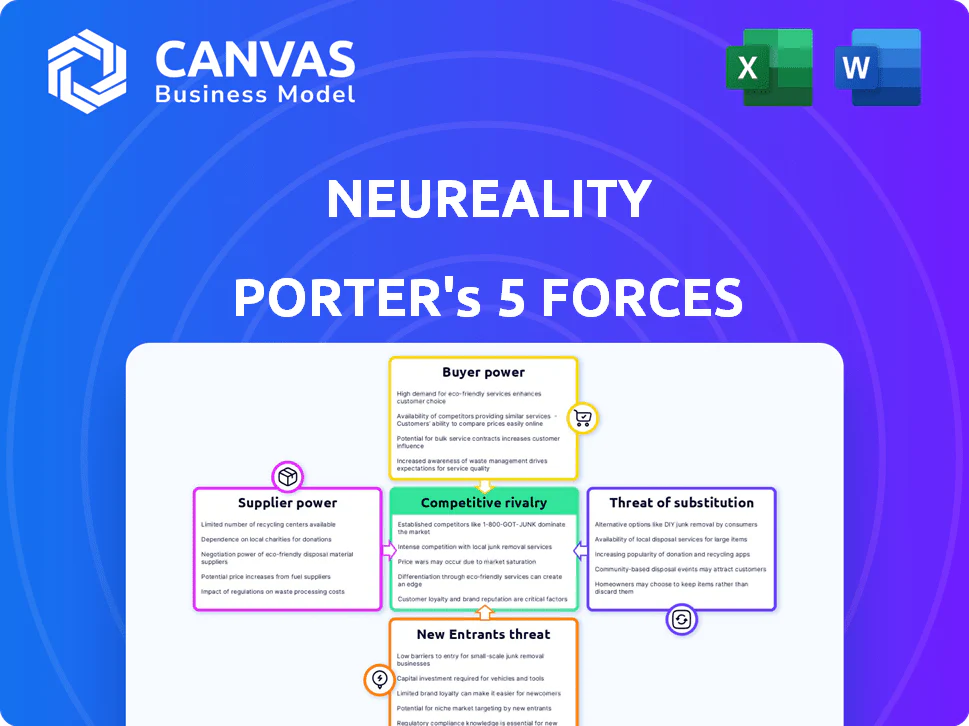

NeuReality Porter's Five Forces Analysis

This is the complete Porter's Five Forces analysis of NeuReality. The displayed document is the exact version you'll receive after purchase, professionally written.

Porter's Five Forces Analysis Template

Go Beyond the Preview—Access the Full Strategic Report

NeuReality's industry is shaped by powerful forces. Supplier power is moderate due to specialized chip manufacturing. Buyer power is high given diverse customer needs. The threat of new entrants is significant, fueled by innovation. Substitute products pose a moderate threat from alternative technologies. Competitive rivalry is intense, with key players vying for market share.

Ready to move beyond the basics? Get a full strategic breakdown of NeuReality’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Limited number of specialized component providers

NeuReality faces a challenging supplier landscape. The AI chip market depends on a few specialized component providers. This includes processors and memory, which gives suppliers pricing power. For example, in 2024, Intel and NVIDIA controlled a large share of the CPU and GPU markets.

High switching costs for key technologies

Switching AI hardware suppliers is tough due to high costs. Redesigning systems and retooling manufacturing processes are expensive. This lack of flexibility increases supplier power, potentially raising costs for NeuReality. In 2024, the average cost to switch suppliers in the tech sector was up to 15% of the contract value.

Supplier technological advancements and roadmaps

Suppliers of advanced semiconductor tech, like Intel and TSMC, drive innovation. NeuReality relies on these roadmaps. Their willingness to collaborate impacts NeuReality's solutions. In 2024, TSMC invested $65 billion in advanced chip manufacturing. This gives suppliers significant leverage.

Potential for supplier vertical integration

Some AI hardware suppliers are expanding into AI solutions, a form of vertical integration. This could intensify competition for NeuReality and affect its access to key components. For example, Nvidia, a major GPU supplier, also offers AI software platforms. This dual role could create biases. The market share of Nvidia in the AI chip market was around 80% in 2024.

- Supplier vertical integration can limit access to components.

- Increased competition from suppliers' own AI offerings.

- Nvidia's dominance in the AI chip market influences the landscape.

- Potential cost increases for NeuReality.

Dependence on foundry relationships

NeuReality, as a fabless semiconductor company, is significantly dependent on third-party foundries for manufacturing its AI processors. The limited number of advanced foundry options, such as TSMC and Samsung, means they possess considerable bargaining power. High demand for cutting-edge foundry services further strengthens their position, potentially impacting NeuReality's manufacturing costs and capacity. This dependence can lead to challenges in negotiating favorable terms and securing production yields.

- TSMC reported a 16.5% revenue increase in 2023, highlighting strong demand.

- Samsung's foundry business is also expanding, but competition remains fierce.

- Foundry costs can represent a significant portion of a fabless company's expenses.

- Capacity allocation is a key concern, especially with emerging AI chip designs.

AI Chip Market: A Competitive Landscape

NeuReality contends with powerful suppliers in the AI chip market, notably Intel and NVIDIA, which controlled a large share of the CPU and GPU markets in 2024. Switching costs for AI hardware are high, potentially raising NeuReality's expenses; the average cost to switch suppliers in the tech sector was up to 15% of the contract value in 2024. Vertical integration by suppliers, like NVIDIA, who had around 80% market share in 2024, intensifies competition and affects component access.

| Aspect | Impact | Data (2024) |

|---|---|---|

| Supplier Concentration | High pricing power | Intel, NVIDIA control major market share |

| Switching Costs | Increased expenses | Up to 15% of contract value |

| Vertical Integration | Competition, access issues | NVIDIA's ~80% AI chip market share |

Customers Bargaining Power

Customers demand cost-effective AI solutions

As AI adoption expands, customers prioritize affordable infrastructure for AI workloads. NeuReality must provide competitive pricing and demonstrate a strong ROI, empowering customers during negotiations. The global AI market is projected to reach $305.9 billion by 2024, indicating a growing demand for cost-effective solutions. This customer demand impacts NeuReality's pricing strategies.

Availability of alternative AI infrastructure options

Customers wield significant bargaining power due to diverse AI infrastructure choices. In 2024, the global AI market is estimated at $327.5 billion. This includes traditional CPU/GPU servers, cloud services, and specialized AI hardware. This variety allows customers to negotiate prices and demand better service, increasing their influence.

Large enterprise clients have significant leverage

NeuReality's focus on large enterprises and hyperscalers puts it in a market where customers wield considerable power. These major clients, deploying AI at scale, can dictate terms. For example, in 2024, hyperscalers like Amazon, Microsoft, and Google accounted for over 60% of global cloud infrastructure spending, highlighting their market dominance.

Customer need for seamless integration and ease of use

Customers increasingly demand AI infrastructure that integrates smoothly and is user-friendly. NeuReality aims to meet this need with comprehensive solutions, software, and APIs. However, customers can still pressure for improved interoperability and easier deployment. In 2024, the demand for user-friendly AI solutions grew by 30%, reflecting customer priorities.

- Interoperability: Customers seek systems that work well with existing infrastructures.

- Ease of Deployment: Simpler installation and setup are crucial.

- User-Friendly Interfaces: Intuitive designs improve usability.

- Ongoing Support: Reliable assistance ensures smooth operation.

Customer sensitivity to performance and efficiency

In the realm of AI workloads, customers are highly attuned to performance and energy efficiency, which directly impacts operational costs and ROI. NeuReality's focus on these aspects positions it to attract customers. However, customer power is amplified by their ability to compare NeuReality's offerings with competing solutions. This comparison hinges on the perceived benefits in performance and efficiency.

- AI chip market is projected to reach $194.9 billion by 2028, growing at a CAGR of 30.2% from 2021.

- Energy efficiency is a key concern, with data centers accounting for about 2% of global energy use.

- Customers will assess NeuReality's performance gains against alternative AI accelerators like GPUs or TPUs.

- The ability to switch vendors easily increases customer bargaining power.

AI Infrastructure: Customer Power Dynamics

Customers hold significant bargaining power in the AI infrastructure market. Their ability to choose from diverse options, including CPUs, GPUs, and cloud services, strengthens their position. In 2024, the AI market is valued at $327.5 billion, offering customers numerous choices. Large enterprises and hyperscalers, representing over 60% of cloud spending, further amplify customer influence.

| Aspect | Impact | 2024 Data |

|---|---|---|

| Market Size | More choices | $327.5B AI market |

| Key Players | Dictate terms | 60%+ cloud spend by hyperscalers |

| Customer Demand | Influence on solutions | 30% growth in user-friendly AI |

Rivalry Among Competitors

Presence of established AI chip and hardware companies

The AI chip market is fiercely competitive. NVIDIA, Intel, and AMD, major players, possess substantial resources and market presence. In 2024, NVIDIA dominated with approximately 80% of the discrete GPU market share. This creates significant challenges for NeuReality.

Increasing number of startups in the AI hardware space

The AI hardware space is heating up. The demand for AI solutions has attracted many startups. This intensifies competition, as new companies compete for market share. NeuReality faces this increased rivalry. In 2024, AI hardware startups saw over $10 billion in funding.

Rapid pace of technological innovation

The AI hardware market is rapidly evolving, with firms constantly innovating. This constant flux demands continuous advancement from NeuReality. Staying competitive requires significant investment in R&D to keep up. In 2024, the AI hardware market was valued at over $30 billion, with growth expected to continue.

Competition from in-house AI chip development by hyperscalers

Major cloud providers, including AWS, Microsoft, and Google, are heavily investing in in-house AI chip development, posing a direct threat. This shift allows them to optimize solutions and potentially reduce reliance on external vendors. Hyperscalers' investment in proprietary AI chips is substantial, with billions allocated annually. This trend intensifies competition for NeuReality, potentially affecting its market share and pricing strategies.

- AWS invested over $100 billion in 2024 in infrastructure, including AI chips.

- Microsoft's AI chip investments are projected to reach $50 billion by 2025.

- Google's TPU development has cost billions, competing with external AI chip providers.

Price and performance as key competitive factors

In the AI infrastructure market, price and performance are crucial competitive factors, as companies vie for the best cost-performance ratio. NeuReality must highlight its price/performance benefits to succeed. The market sees aggressive competition, with firms like NVIDIA constantly improving their offerings. Securing contracts depends on demonstrating significant advantages.

- NVIDIA controls approximately 80% of the AI chip market share as of late 2024.

- AI hardware market is projected to reach $194.9 billion by 2028.

- Energy efficiency is a key selling point with rising electricity costs.

AI Chip Market: A Fierce Battleground

Competitive rivalry in the AI chip market is intense, driven by established giants and innovative startups. NVIDIA's dominance, holding about 80% of the discrete GPU market share in 2024, sets a high bar. Major cloud providers' in-house chip development adds further pressure, increasing competition.

| Factor | Details | Impact on NeuReality |

|---|---|---|

| Market Share | NVIDIA's ~80% market share (2024). | Challenges market entry and growth. |

| R&D Spending | AI hardware market reached over $30B (2024), with continuous innovation. | Requires significant investment to remain competitive. |

| Cloud Providers | AWS invested over $100B in infrastructure (2024), including AI chips. | Increases competition from in-house solutions. |

Original: $10.00

-65%$10.00

$3.50NEUREALITY PORTER'S FIVE FORCES TEMPLATE RESEARCH

What is included in the product

Analyzes NeuReality's competitive landscape: rivals, buyers, suppliers, new entrants, and substitutes.

Prioritize key threats, identifying high-impact factors for swift decision-making.

Same Document Delivered

NeuReality Porter's Five Forces Analysis

This is the complete Porter's Five Forces analysis of NeuReality. The displayed document is the exact version you'll receive after purchase, professionally written.

Porter's Five Forces Analysis Template

Go Beyond the Preview—Access the Full Strategic Report

NeuReality's industry is shaped by powerful forces. Supplier power is moderate due to specialized chip manufacturing. Buyer power is high given diverse customer needs. The threat of new entrants is significant, fueled by innovation. Substitute products pose a moderate threat from alternative technologies. Competitive rivalry is intense, with key players vying for market share.

Ready to move beyond the basics? Get a full strategic breakdown of NeuReality’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Limited number of specialized component providers

NeuReality faces a challenging supplier landscape. The AI chip market depends on a few specialized component providers. This includes processors and memory, which gives suppliers pricing power. For example, in 2024, Intel and NVIDIA controlled a large share of the CPU and GPU markets.

High switching costs for key technologies

Switching AI hardware suppliers is tough due to high costs. Redesigning systems and retooling manufacturing processes are expensive. This lack of flexibility increases supplier power, potentially raising costs for NeuReality. In 2024, the average cost to switch suppliers in the tech sector was up to 15% of the contract value.

Supplier technological advancements and roadmaps

Suppliers of advanced semiconductor tech, like Intel and TSMC, drive innovation. NeuReality relies on these roadmaps. Their willingness to collaborate impacts NeuReality's solutions. In 2024, TSMC invested $65 billion in advanced chip manufacturing. This gives suppliers significant leverage.

Potential for supplier vertical integration

Some AI hardware suppliers are expanding into AI solutions, a form of vertical integration. This could intensify competition for NeuReality and affect its access to key components. For example, Nvidia, a major GPU supplier, also offers AI software platforms. This dual role could create biases. The market share of Nvidia in the AI chip market was around 80% in 2024.

- Supplier vertical integration can limit access to components.

- Increased competition from suppliers' own AI offerings.

- Nvidia's dominance in the AI chip market influences the landscape.

- Potential cost increases for NeuReality.

Dependence on foundry relationships

NeuReality, as a fabless semiconductor company, is significantly dependent on third-party foundries for manufacturing its AI processors. The limited number of advanced foundry options, such as TSMC and Samsung, means they possess considerable bargaining power. High demand for cutting-edge foundry services further strengthens their position, potentially impacting NeuReality's manufacturing costs and capacity. This dependence can lead to challenges in negotiating favorable terms and securing production yields.

- TSMC reported a 16.5% revenue increase in 2023, highlighting strong demand.

- Samsung's foundry business is also expanding, but competition remains fierce.

- Foundry costs can represent a significant portion of a fabless company's expenses.

- Capacity allocation is a key concern, especially with emerging AI chip designs.

AI Chip Market: A Competitive Landscape

NeuReality contends with powerful suppliers in the AI chip market, notably Intel and NVIDIA, which controlled a large share of the CPU and GPU markets in 2024. Switching costs for AI hardware are high, potentially raising NeuReality's expenses; the average cost to switch suppliers in the tech sector was up to 15% of the contract value in 2024. Vertical integration by suppliers, like NVIDIA, who had around 80% market share in 2024, intensifies competition and affects component access.

| Aspect | Impact | Data (2024) |

|---|---|---|

| Supplier Concentration | High pricing power | Intel, NVIDIA control major market share |

| Switching Costs | Increased expenses | Up to 15% of contract value |

| Vertical Integration | Competition, access issues | NVIDIA's ~80% AI chip market share |

Customers Bargaining Power

Customers demand cost-effective AI solutions

As AI adoption expands, customers prioritize affordable infrastructure for AI workloads. NeuReality must provide competitive pricing and demonstrate a strong ROI, empowering customers during negotiations. The global AI market is projected to reach $305.9 billion by 2024, indicating a growing demand for cost-effective solutions. This customer demand impacts NeuReality's pricing strategies.

Availability of alternative AI infrastructure options

Customers wield significant bargaining power due to diverse AI infrastructure choices. In 2024, the global AI market is estimated at $327.5 billion. This includes traditional CPU/GPU servers, cloud services, and specialized AI hardware. This variety allows customers to negotiate prices and demand better service, increasing their influence.

Large enterprise clients have significant leverage

NeuReality's focus on large enterprises and hyperscalers puts it in a market where customers wield considerable power. These major clients, deploying AI at scale, can dictate terms. For example, in 2024, hyperscalers like Amazon, Microsoft, and Google accounted for over 60% of global cloud infrastructure spending, highlighting their market dominance.

Customer need for seamless integration and ease of use

Customers increasingly demand AI infrastructure that integrates smoothly and is user-friendly. NeuReality aims to meet this need with comprehensive solutions, software, and APIs. However, customers can still pressure for improved interoperability and easier deployment. In 2024, the demand for user-friendly AI solutions grew by 30%, reflecting customer priorities.

- Interoperability: Customers seek systems that work well with existing infrastructures.

- Ease of Deployment: Simpler installation and setup are crucial.

- User-Friendly Interfaces: Intuitive designs improve usability.

- Ongoing Support: Reliable assistance ensures smooth operation.

Customer sensitivity to performance and efficiency

In the realm of AI workloads, customers are highly attuned to performance and energy efficiency, which directly impacts operational costs and ROI. NeuReality's focus on these aspects positions it to attract customers. However, customer power is amplified by their ability to compare NeuReality's offerings with competing solutions. This comparison hinges on the perceived benefits in performance and efficiency.

- AI chip market is projected to reach $194.9 billion by 2028, growing at a CAGR of 30.2% from 2021.

- Energy efficiency is a key concern, with data centers accounting for about 2% of global energy use.

- Customers will assess NeuReality's performance gains against alternative AI accelerators like GPUs or TPUs.

- The ability to switch vendors easily increases customer bargaining power.

AI Infrastructure: Customer Power Dynamics

Customers hold significant bargaining power in the AI infrastructure market. Their ability to choose from diverse options, including CPUs, GPUs, and cloud services, strengthens their position. In 2024, the AI market is valued at $327.5 billion, offering customers numerous choices. Large enterprises and hyperscalers, representing over 60% of cloud spending, further amplify customer influence.

| Aspect | Impact | 2024 Data |

|---|---|---|

| Market Size | More choices | $327.5B AI market |

| Key Players | Dictate terms | 60%+ cloud spend by hyperscalers |

| Customer Demand | Influence on solutions | 30% growth in user-friendly AI |

Rivalry Among Competitors

Presence of established AI chip and hardware companies

The AI chip market is fiercely competitive. NVIDIA, Intel, and AMD, major players, possess substantial resources and market presence. In 2024, NVIDIA dominated with approximately 80% of the discrete GPU market share. This creates significant challenges for NeuReality.

Increasing number of startups in the AI hardware space

The AI hardware space is heating up. The demand for AI solutions has attracted many startups. This intensifies competition, as new companies compete for market share. NeuReality faces this increased rivalry. In 2024, AI hardware startups saw over $10 billion in funding.

Rapid pace of technological innovation

The AI hardware market is rapidly evolving, with firms constantly innovating. This constant flux demands continuous advancement from NeuReality. Staying competitive requires significant investment in R&D to keep up. In 2024, the AI hardware market was valued at over $30 billion, with growth expected to continue.

Competition from in-house AI chip development by hyperscalers

Major cloud providers, including AWS, Microsoft, and Google, are heavily investing in in-house AI chip development, posing a direct threat. This shift allows them to optimize solutions and potentially reduce reliance on external vendors. Hyperscalers' investment in proprietary AI chips is substantial, with billions allocated annually. This trend intensifies competition for NeuReality, potentially affecting its market share and pricing strategies.

- AWS invested over $100 billion in 2024 in infrastructure, including AI chips.

- Microsoft's AI chip investments are projected to reach $50 billion by 2025.

- Google's TPU development has cost billions, competing with external AI chip providers.

Price and performance as key competitive factors

In the AI infrastructure market, price and performance are crucial competitive factors, as companies vie for the best cost-performance ratio. NeuReality must highlight its price/performance benefits to succeed. The market sees aggressive competition, with firms like NVIDIA constantly improving their offerings. Securing contracts depends on demonstrating significant advantages.

- NVIDIA controls approximately 80% of the AI chip market share as of late 2024.

- AI hardware market is projected to reach $194.9 billion by 2028.

- Energy efficiency is a key selling point with rising electricity costs.

AI Chip Market: A Fierce Battleground

Competitive rivalry in the AI chip market is intense, driven by established giants and innovative startups. NVIDIA's dominance, holding about 80% of the discrete GPU market share in 2024, sets a high bar. Major cloud providers' in-house chip development adds further pressure, increasing competition.

| Factor | Details | Impact on NeuReality |

|---|---|---|

| Market Share | NVIDIA's ~80% market share (2024). | Challenges market entry and growth. |

| R&D Spending | AI hardware market reached over $30B (2024), with continuous innovation. | Requires significant investment to remain competitive. |

| Cloud Providers | AWS invested over $100B in infrastructure (2024), including AI chips. | Increases competition from in-house solutions. |

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

What is included in the product

Analyzes NeuReality's competitive landscape: rivals, buyers, suppliers, new entrants, and substitutes.

Prioritize key threats, identifying high-impact factors for swift decision-making.

Same Document Delivered

NeuReality Porter's Five Forces Analysis

This is the complete Porter's Five Forces analysis of NeuReality. The displayed document is the exact version you'll receive after purchase, professionally written.

Porter's Five Forces Analysis Template

Go Beyond the Preview—Access the Full Strategic Report

NeuReality's industry is shaped by powerful forces. Supplier power is moderate due to specialized chip manufacturing. Buyer power is high given diverse customer needs. The threat of new entrants is significant, fueled by innovation. Substitute products pose a moderate threat from alternative technologies. Competitive rivalry is intense, with key players vying for market share.

Ready to move beyond the basics? Get a full strategic breakdown of NeuReality’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Limited number of specialized component providers

NeuReality faces a challenging supplier landscape. The AI chip market depends on a few specialized component providers. This includes processors and memory, which gives suppliers pricing power. For example, in 2024, Intel and NVIDIA controlled a large share of the CPU and GPU markets.

High switching costs for key technologies

Switching AI hardware suppliers is tough due to high costs. Redesigning systems and retooling manufacturing processes are expensive. This lack of flexibility increases supplier power, potentially raising costs for NeuReality. In 2024, the average cost to switch suppliers in the tech sector was up to 15% of the contract value.

Supplier technological advancements and roadmaps

Suppliers of advanced semiconductor tech, like Intel and TSMC, drive innovation. NeuReality relies on these roadmaps. Their willingness to collaborate impacts NeuReality's solutions. In 2024, TSMC invested $65 billion in advanced chip manufacturing. This gives suppliers significant leverage.

Potential for supplier vertical integration

Some AI hardware suppliers are expanding into AI solutions, a form of vertical integration. This could intensify competition for NeuReality and affect its access to key components. For example, Nvidia, a major GPU supplier, also offers AI software platforms. This dual role could create biases. The market share of Nvidia in the AI chip market was around 80% in 2024.

- Supplier vertical integration can limit access to components.

- Increased competition from suppliers' own AI offerings.

- Nvidia's dominance in the AI chip market influences the landscape.

- Potential cost increases for NeuReality.

Dependence on foundry relationships

NeuReality, as a fabless semiconductor company, is significantly dependent on third-party foundries for manufacturing its AI processors. The limited number of advanced foundry options, such as TSMC and Samsung, means they possess considerable bargaining power. High demand for cutting-edge foundry services further strengthens their position, potentially impacting NeuReality's manufacturing costs and capacity. This dependence can lead to challenges in negotiating favorable terms and securing production yields.

- TSMC reported a 16.5% revenue increase in 2023, highlighting strong demand.

- Samsung's foundry business is also expanding, but competition remains fierce.

- Foundry costs can represent a significant portion of a fabless company's expenses.

- Capacity allocation is a key concern, especially with emerging AI chip designs.

AI Chip Market: A Competitive Landscape

NeuReality contends with powerful suppliers in the AI chip market, notably Intel and NVIDIA, which controlled a large share of the CPU and GPU markets in 2024. Switching costs for AI hardware are high, potentially raising NeuReality's expenses; the average cost to switch suppliers in the tech sector was up to 15% of the contract value in 2024. Vertical integration by suppliers, like NVIDIA, who had around 80% market share in 2024, intensifies competition and affects component access.

| Aspect | Impact | Data (2024) |

|---|---|---|

| Supplier Concentration | High pricing power | Intel, NVIDIA control major market share |

| Switching Costs | Increased expenses | Up to 15% of contract value |

| Vertical Integration | Competition, access issues | NVIDIA's ~80% AI chip market share |

Customers Bargaining Power

Customers demand cost-effective AI solutions

As AI adoption expands, customers prioritize affordable infrastructure for AI workloads. NeuReality must provide competitive pricing and demonstrate a strong ROI, empowering customers during negotiations. The global AI market is projected to reach $305.9 billion by 2024, indicating a growing demand for cost-effective solutions. This customer demand impacts NeuReality's pricing strategies.

Availability of alternative AI infrastructure options

Customers wield significant bargaining power due to diverse AI infrastructure choices. In 2024, the global AI market is estimated at $327.5 billion. This includes traditional CPU/GPU servers, cloud services, and specialized AI hardware. This variety allows customers to negotiate prices and demand better service, increasing their influence.

Large enterprise clients have significant leverage

NeuReality's focus on large enterprises and hyperscalers puts it in a market where customers wield considerable power. These major clients, deploying AI at scale, can dictate terms. For example, in 2024, hyperscalers like Amazon, Microsoft, and Google accounted for over 60% of global cloud infrastructure spending, highlighting their market dominance.

Customer need for seamless integration and ease of use

Customers increasingly demand AI infrastructure that integrates smoothly and is user-friendly. NeuReality aims to meet this need with comprehensive solutions, software, and APIs. However, customers can still pressure for improved interoperability and easier deployment. In 2024, the demand for user-friendly AI solutions grew by 30%, reflecting customer priorities.

- Interoperability: Customers seek systems that work well with existing infrastructures.

- Ease of Deployment: Simpler installation and setup are crucial.

- User-Friendly Interfaces: Intuitive designs improve usability.

- Ongoing Support: Reliable assistance ensures smooth operation.

Customer sensitivity to performance and efficiency

In the realm of AI workloads, customers are highly attuned to performance and energy efficiency, which directly impacts operational costs and ROI. NeuReality's focus on these aspects positions it to attract customers. However, customer power is amplified by their ability to compare NeuReality's offerings with competing solutions. This comparison hinges on the perceived benefits in performance and efficiency.

- AI chip market is projected to reach $194.9 billion by 2028, growing at a CAGR of 30.2% from 2021.

- Energy efficiency is a key concern, with data centers accounting for about 2% of global energy use.

- Customers will assess NeuReality's performance gains against alternative AI accelerators like GPUs or TPUs.

- The ability to switch vendors easily increases customer bargaining power.

AI Infrastructure: Customer Power Dynamics

Customers hold significant bargaining power in the AI infrastructure market. Their ability to choose from diverse options, including CPUs, GPUs, and cloud services, strengthens their position. In 2024, the AI market is valued at $327.5 billion, offering customers numerous choices. Large enterprises and hyperscalers, representing over 60% of cloud spending, further amplify customer influence.

| Aspect | Impact | 2024 Data |

|---|---|---|

| Market Size | More choices | $327.5B AI market |

| Key Players | Dictate terms | 60%+ cloud spend by hyperscalers |

| Customer Demand | Influence on solutions | 30% growth in user-friendly AI |

Rivalry Among Competitors

Presence of established AI chip and hardware companies

The AI chip market is fiercely competitive. NVIDIA, Intel, and AMD, major players, possess substantial resources and market presence. In 2024, NVIDIA dominated with approximately 80% of the discrete GPU market share. This creates significant challenges for NeuReality.

Increasing number of startups in the AI hardware space

The AI hardware space is heating up. The demand for AI solutions has attracted many startups. This intensifies competition, as new companies compete for market share. NeuReality faces this increased rivalry. In 2024, AI hardware startups saw over $10 billion in funding.

Rapid pace of technological innovation

The AI hardware market is rapidly evolving, with firms constantly innovating. This constant flux demands continuous advancement from NeuReality. Staying competitive requires significant investment in R&D to keep up. In 2024, the AI hardware market was valued at over $30 billion, with growth expected to continue.

Competition from in-house AI chip development by hyperscalers

Major cloud providers, including AWS, Microsoft, and Google, are heavily investing in in-house AI chip development, posing a direct threat. This shift allows them to optimize solutions and potentially reduce reliance on external vendors. Hyperscalers' investment in proprietary AI chips is substantial, with billions allocated annually. This trend intensifies competition for NeuReality, potentially affecting its market share and pricing strategies.

- AWS invested over $100 billion in 2024 in infrastructure, including AI chips.

- Microsoft's AI chip investments are projected to reach $50 billion by 2025.

- Google's TPU development has cost billions, competing with external AI chip providers.

Price and performance as key competitive factors

In the AI infrastructure market, price and performance are crucial competitive factors, as companies vie for the best cost-performance ratio. NeuReality must highlight its price/performance benefits to succeed. The market sees aggressive competition, with firms like NVIDIA constantly improving their offerings. Securing contracts depends on demonstrating significant advantages.

- NVIDIA controls approximately 80% of the AI chip market share as of late 2024.

- AI hardware market is projected to reach $194.9 billion by 2028.

- Energy efficiency is a key selling point with rising electricity costs.

AI Chip Market: A Fierce Battleground

Competitive rivalry in the AI chip market is intense, driven by established giants and innovative startups. NVIDIA's dominance, holding about 80% of the discrete GPU market share in 2024, sets a high bar. Major cloud providers' in-house chip development adds further pressure, increasing competition.

| Factor | Details | Impact on NeuReality |

|---|---|---|

| Market Share | NVIDIA's ~80% market share (2024). | Challenges market entry and growth. |

| R&D Spending | AI hardware market reached over $30B (2024), with continuous innovation. | Requires significant investment to remain competitive. |

| Cloud Providers | AWS invested over $100B in infrastructure (2024), including AI chips. | Increases competition from in-house solutions. |