NORFOLK SOUTHERN CORPORATION PORTER'S FIVE FORCES TEMPLATE RESEARCH

What is included in the product

Tailored exclusively for Norfolk Southern, analyzing its position within its competitive landscape.

Instantly highlight Porter's Five Forces' strategic impact on Norfolk Southern with a clear visualization.

What You See Is What You Get

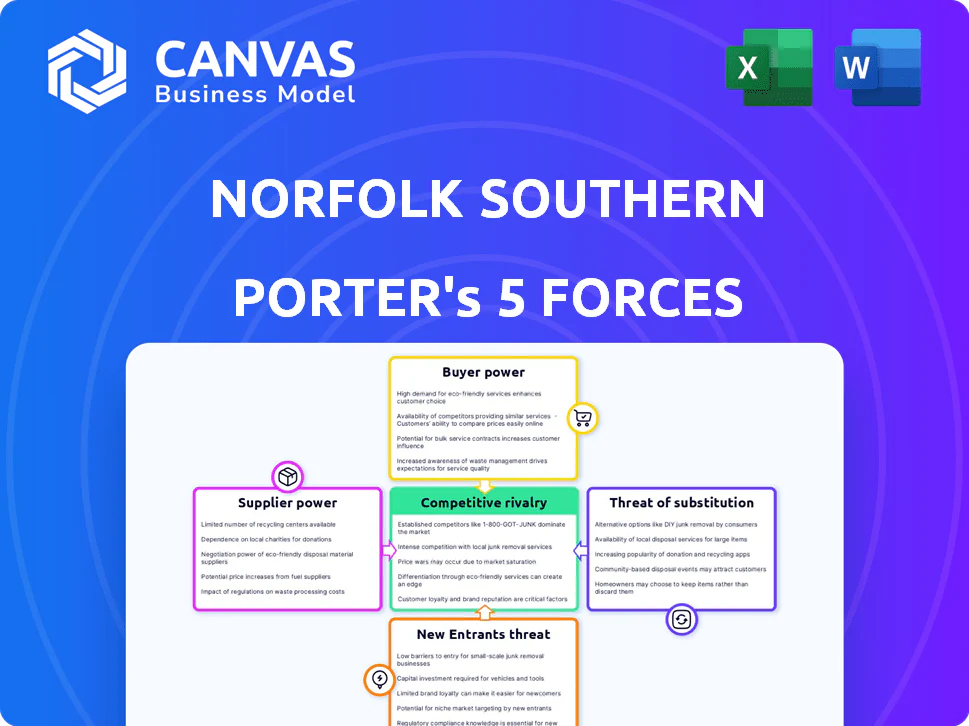

Norfolk Southern Corporation Porter's Five Forces Analysis

This preview is the complete analysis. It's the exact Porter's Five Forces document you'll receive. It comprehensively analyzes Norfolk Southern. The content and formatting are identical in the purchased file.

Porter's Five Forces Analysis Template

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Norfolk Southern's industry faces moderate rivalry, influenced by a few major players and high capital investments. Buyer power is considerable, with large shippers able to negotiate rates. Supplier power is generally low, with readily available inputs. The threat of new entrants is limited due to high barriers. The threat of substitutes like trucking exists, but rail offers advantages.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Norfolk Southern Corporation’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Limited number of key suppliers

Norfolk Southern's dependence on a few suppliers, like locomotive manufacturers, boosts their bargaining power. This concentration lets suppliers dictate prices and terms more effectively. In 2024, about 70% of new locomotives came from just two companies. This gives suppliers significant pricing leverage, impacting Norfolk Southern's costs.

High switching costs for alternative suppliers

Norfolk Southern faces high switching costs, especially with specialized rail infrastructure. Changing suppliers for critical components and equipment, such as locomotives and signaling systems, is expensive. These costs include integration, testing, and logistics, increasing supplier bargaining power. For example, in 2024, the company spent $1.8 billion on capital expenditures, a portion of which went to specialized equipment where switching costs are high.

Increased demand for raw materials impacting supplier leverage

Norfolk Southern's supplier bargaining power is influenced by raw material demand. The need for steel and coal, essential for rail operations, gives suppliers leverage. In 2024, steel prices saw fluctuations, impacting operating costs. These cost shifts can affect profitability.

Potential for vertical integration by suppliers

If Norfolk Southern's suppliers integrated vertically, offering competitive services, their leverage would spike. This would challenge Norfolk Southern's control over costs and service terms. Such integration could reshape the supply landscape, impacting profitability. The possibility compels Norfolk Southern to strategize supplier relations proactively.

- In 2024, Norfolk Southern spent billions on materials and services, highlighting supplier importance.

- Vertical integration could lead to suppliers directly serving customers, bypassing Norfolk Southern.

- This risk necessitates robust supply chain management and strategic partnerships.

Quality and reliability impact operational efficiency

Norfolk Southern's operational success hinges on the quality and dependability of its suppliers. Poor-quality materials or unreliable equipment can cause significant disruptions, leading to increased expenses and potential safety issues. This dependence grants suppliers, especially those offering superior products, increased leverage in negotiations. For instance, a 2024 report showed that equipment failures caused a 10% increase in maintenance costs for the rail industry, highlighting the impact of supplier reliability.

- Supplier quality directly affects operational efficiency and safety.

- Unreliable suppliers can lead to disruptions and higher costs.

- Superior product suppliers gain more bargaining power.

- In 2024, equipment failures raised maintenance costs by 10%.

Supplier Power Dynamics: A Look at Key Factors

Norfolk Southern's supplier power stems from its reliance on few providers, like locomotive makers. High switching costs for specialized rail tech boost supplier leverage. Raw material needs, like steel, also give suppliers bargaining power.

| Factor | Impact | 2024 Data |

|---|---|---|

| Supplier Concentration | Higher prices | 70% of new locomotives from 2 firms |

| Switching Costs | Expensive changes | $1.8B CapEx on specialized gear |

| Raw Materials | Cost fluctuations | Steel price volatility |

Customers Bargaining Power

Diverse customer base with varying transportation needs

Norfolk Southern's customer base spans agriculture, automotive, and coal, among other sectors. Customer power varies by freight type and volume. In 2024, the company moved approximately 1.3 million carloads of merchandise. This diversity lessens the impact of any single customer's bargaining power.

Large shippers have more negotiating power

Major customers, like Amazon and UPS, wield considerable bargaining power due to the substantial volumes of goods they ship. These large shippers often secure long-term contracts, which allows them to negotiate favorable rates and service agreements. In 2024, Norfolk Southern's top ten customers accounted for approximately 25% of its revenue, highlighting the impact of these key accounts. The ability of these customers to shift to other transportation modes further strengthens their negotiating position.

Price sensitivity among smaller customers

Smaller customers, potentially less powerful individually, are often highly price-sensitive. Yet, their combined demand significantly impacts pricing decisions. For example, a 2024 study showed that even a 1% price increase can cause a 2-3% drop in volume for some customer segments. This sensitivity forces Norfolk Southern to balance price with volume to maintain profitability. This is a crucial aspect of the company's strategy.

Increased demand for intermodal services enhances customer choice

The rise of intermodal services gives customers more choices, potentially boosting their bargaining power. This increased competition can lead to lower prices and better service terms for shippers. Norfolk Southern faces this pressure as customers can now easily switch between various transportation methods. For example, in 2024, intermodal traffic accounted for a significant portion of overall freight volume.

- Intermodal growth offers shippers more alternatives.

- Customers can negotiate better rates and service levels.

- Competition among carriers intensifies.

- Norfolk Southern's pricing strategies are affected.

Long-term contracts can stabilize pricing

While large customers might wield significant influence, Norfolk Southern's long-term contracts offer a buffer. These contracts ensure price stability for both the company and its clients. For instance, in 2023, approximately 60% of Norfolk Southern's revenue came from contracted business, showcasing the importance of these agreements. This strategy reduces immediate pressure from fluctuating market conditions.

- Contracted revenue provides predictability.

- Long-term agreements reduce price volatility.

- Stability benefits both Norfolk Southern and customers.

- Approximately 60% of revenue from contracts in 2023.

Customer Power & Revenue Dynamics

Customer bargaining power varies based on shipment size and mode choice. Large customers like Amazon and UPS can negotiate favorable terms, influencing pricing. In 2024, the top 10 customers generated about 25% of Norfolk Southern's revenue. Long-term contracts provide some stability, with 60% of revenue from contracts in 2023.

| Aspect | Impact | 2024 Data |

|---|---|---|

| Customer Size | Influences Pricing | Top 10 Customers: ~25% Revenue |

| Contractual Agreements | Provides Stability | ~60% Revenue (2023) |

| Intermodal Growth | Increases Options | Significant Freight Volume |

Rivalry Among Competitors

Presence of multiple major railroads increases competition

Norfolk Southern faces intense competition because the railroad industry is dominated by a few major players. Key competitors include CSX, Union Pacific, and BNSF. This concentration means each railroad fights hard for market share. In 2024, these competitors collectively handled billions of dollars worth of freight, highlighting the stakes.

Competitive network capabilities

Rival railroads vie on network reach and efficiency. Norfolk Southern (NSC) boasts a strong network, a competitive edge. In Q3 2023, NSC's operating ratio was 62.3%, reflecting operational efficiency. This network supports diverse freight, critical for customer service.

Infrastructure and technology investment

Norfolk Southern (NSC) and its rivals heavily invest in infrastructure and technology. NSC's capital expenditures in 2023 were around $1.6 billion. These investments enhance operational efficiency and safety.

Price competition for freight traffic

Price competition is fierce in the freight industry, heavily influencing Norfolk Southern Corporation's (NSC) competitive environment. Railroads frequently adjust rates to secure business, particularly for bulk commodities where trucking or other transport methods are viable alternatives. This pricing pressure can affect profitability, as NSC and its rivals vie to offer the most attractive rates while managing operational costs. The ability to offer competitive pricing, while maintaining service quality, is crucial for retaining and gaining market share.

- In 2024, the average revenue per carload for U.S. Class I railroads was approximately $2,500.

- Trucking's market share for freight is around 70%, indicating the significant competitive pressure from this mode.

- Norfolk Southern's operating ratio (operating expenses as a percentage of revenue) was about 63% in 2024, showing the efficiency needed to manage costs.

- Fuel costs and labor expenses significantly impact pricing strategies.

Service quality and reliability

Railroads fiercely compete on service quality and reliability, key for customer satisfaction. This includes crucial aspects like on-time delivery and ensuring safety standards. Superior service is critical for securing and maintaining customer loyalty, influencing market share. Norfolk Southern's ability to provide dependable, high-quality service is directly tied to its competitive standing.

- In 2024, Norfolk Southern's operating ratio was around 64%, indicating efficiency.

- On-time performance data shows fluctuations, emphasizing the need for continuous improvement.

- Safety metrics, such as accident rates, are constantly monitored to enhance service quality.

- Customer satisfaction surveys provide insights into service strengths and weaknesses.

Railroad Rivals: A High-Stakes Game

Competitive rivalry in the railroad industry is intense, primarily due to a few major players like Norfolk Southern, CSX, and Union Pacific. These companies compete on network reach, operational efficiency, and service quality. In 2024, the average revenue per carload for U.S. Class I railroads was about $2,500, reflecting the economic stakes. Price competition and trucking's 70% market share add further pressure.

| Aspect | Details |

|---|---|

| Key Competitors | CSX, Union Pacific, BNSF |

| 2024 Avg. Revenue/Carload | ~$2,500 |

| Trucking Market Share | ~70% |

Original: $10.00

-65%$10.00

$3.50NORFOLK SOUTHERN CORPORATION PORTER'S FIVE FORCES TEMPLATE RESEARCH

What is included in the product

Tailored exclusively for Norfolk Southern, analyzing its position within its competitive landscape.

Instantly highlight Porter's Five Forces' strategic impact on Norfolk Southern with a clear visualization.

What You See Is What You Get

Norfolk Southern Corporation Porter's Five Forces Analysis

This preview is the complete analysis. It's the exact Porter's Five Forces document you'll receive. It comprehensively analyzes Norfolk Southern. The content and formatting are identical in the purchased file.

Porter's Five Forces Analysis Template

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Norfolk Southern's industry faces moderate rivalry, influenced by a few major players and high capital investments. Buyer power is considerable, with large shippers able to negotiate rates. Supplier power is generally low, with readily available inputs. The threat of new entrants is limited due to high barriers. The threat of substitutes like trucking exists, but rail offers advantages.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Norfolk Southern Corporation’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Limited number of key suppliers

Norfolk Southern's dependence on a few suppliers, like locomotive manufacturers, boosts their bargaining power. This concentration lets suppliers dictate prices and terms more effectively. In 2024, about 70% of new locomotives came from just two companies. This gives suppliers significant pricing leverage, impacting Norfolk Southern's costs.

High switching costs for alternative suppliers

Norfolk Southern faces high switching costs, especially with specialized rail infrastructure. Changing suppliers for critical components and equipment, such as locomotives and signaling systems, is expensive. These costs include integration, testing, and logistics, increasing supplier bargaining power. For example, in 2024, the company spent $1.8 billion on capital expenditures, a portion of which went to specialized equipment where switching costs are high.

Increased demand for raw materials impacting supplier leverage

Norfolk Southern's supplier bargaining power is influenced by raw material demand. The need for steel and coal, essential for rail operations, gives suppliers leverage. In 2024, steel prices saw fluctuations, impacting operating costs. These cost shifts can affect profitability.

Potential for vertical integration by suppliers

If Norfolk Southern's suppliers integrated vertically, offering competitive services, their leverage would spike. This would challenge Norfolk Southern's control over costs and service terms. Such integration could reshape the supply landscape, impacting profitability. The possibility compels Norfolk Southern to strategize supplier relations proactively.

- In 2024, Norfolk Southern spent billions on materials and services, highlighting supplier importance.

- Vertical integration could lead to suppliers directly serving customers, bypassing Norfolk Southern.

- This risk necessitates robust supply chain management and strategic partnerships.

Quality and reliability impact operational efficiency

Norfolk Southern's operational success hinges on the quality and dependability of its suppliers. Poor-quality materials or unreliable equipment can cause significant disruptions, leading to increased expenses and potential safety issues. This dependence grants suppliers, especially those offering superior products, increased leverage in negotiations. For instance, a 2024 report showed that equipment failures caused a 10% increase in maintenance costs for the rail industry, highlighting the impact of supplier reliability.

- Supplier quality directly affects operational efficiency and safety.

- Unreliable suppliers can lead to disruptions and higher costs.

- Superior product suppliers gain more bargaining power.

- In 2024, equipment failures raised maintenance costs by 10%.

Supplier Power Dynamics: A Look at Key Factors

Norfolk Southern's supplier power stems from its reliance on few providers, like locomotive makers. High switching costs for specialized rail tech boost supplier leverage. Raw material needs, like steel, also give suppliers bargaining power.

| Factor | Impact | 2024 Data |

|---|---|---|

| Supplier Concentration | Higher prices | 70% of new locomotives from 2 firms |

| Switching Costs | Expensive changes | $1.8B CapEx on specialized gear |

| Raw Materials | Cost fluctuations | Steel price volatility |

Customers Bargaining Power

Diverse customer base with varying transportation needs

Norfolk Southern's customer base spans agriculture, automotive, and coal, among other sectors. Customer power varies by freight type and volume. In 2024, the company moved approximately 1.3 million carloads of merchandise. This diversity lessens the impact of any single customer's bargaining power.

Large shippers have more negotiating power

Major customers, like Amazon and UPS, wield considerable bargaining power due to the substantial volumes of goods they ship. These large shippers often secure long-term contracts, which allows them to negotiate favorable rates and service agreements. In 2024, Norfolk Southern's top ten customers accounted for approximately 25% of its revenue, highlighting the impact of these key accounts. The ability of these customers to shift to other transportation modes further strengthens their negotiating position.

Price sensitivity among smaller customers

Smaller customers, potentially less powerful individually, are often highly price-sensitive. Yet, their combined demand significantly impacts pricing decisions. For example, a 2024 study showed that even a 1% price increase can cause a 2-3% drop in volume for some customer segments. This sensitivity forces Norfolk Southern to balance price with volume to maintain profitability. This is a crucial aspect of the company's strategy.

Increased demand for intermodal services enhances customer choice

The rise of intermodal services gives customers more choices, potentially boosting their bargaining power. This increased competition can lead to lower prices and better service terms for shippers. Norfolk Southern faces this pressure as customers can now easily switch between various transportation methods. For example, in 2024, intermodal traffic accounted for a significant portion of overall freight volume.

- Intermodal growth offers shippers more alternatives.

- Customers can negotiate better rates and service levels.

- Competition among carriers intensifies.

- Norfolk Southern's pricing strategies are affected.

Long-term contracts can stabilize pricing

While large customers might wield significant influence, Norfolk Southern's long-term contracts offer a buffer. These contracts ensure price stability for both the company and its clients. For instance, in 2023, approximately 60% of Norfolk Southern's revenue came from contracted business, showcasing the importance of these agreements. This strategy reduces immediate pressure from fluctuating market conditions.

- Contracted revenue provides predictability.

- Long-term agreements reduce price volatility.

- Stability benefits both Norfolk Southern and customers.

- Approximately 60% of revenue from contracts in 2023.

Customer Power & Revenue Dynamics

Customer bargaining power varies based on shipment size and mode choice. Large customers like Amazon and UPS can negotiate favorable terms, influencing pricing. In 2024, the top 10 customers generated about 25% of Norfolk Southern's revenue. Long-term contracts provide some stability, with 60% of revenue from contracts in 2023.

| Aspect | Impact | 2024 Data |

|---|---|---|

| Customer Size | Influences Pricing | Top 10 Customers: ~25% Revenue |

| Contractual Agreements | Provides Stability | ~60% Revenue (2023) |

| Intermodal Growth | Increases Options | Significant Freight Volume |

Rivalry Among Competitors

Presence of multiple major railroads increases competition

Norfolk Southern faces intense competition because the railroad industry is dominated by a few major players. Key competitors include CSX, Union Pacific, and BNSF. This concentration means each railroad fights hard for market share. In 2024, these competitors collectively handled billions of dollars worth of freight, highlighting the stakes.

Competitive network capabilities

Rival railroads vie on network reach and efficiency. Norfolk Southern (NSC) boasts a strong network, a competitive edge. In Q3 2023, NSC's operating ratio was 62.3%, reflecting operational efficiency. This network supports diverse freight, critical for customer service.

Infrastructure and technology investment

Norfolk Southern (NSC) and its rivals heavily invest in infrastructure and technology. NSC's capital expenditures in 2023 were around $1.6 billion. These investments enhance operational efficiency and safety.

Price competition for freight traffic

Price competition is fierce in the freight industry, heavily influencing Norfolk Southern Corporation's (NSC) competitive environment. Railroads frequently adjust rates to secure business, particularly for bulk commodities where trucking or other transport methods are viable alternatives. This pricing pressure can affect profitability, as NSC and its rivals vie to offer the most attractive rates while managing operational costs. The ability to offer competitive pricing, while maintaining service quality, is crucial for retaining and gaining market share.

- In 2024, the average revenue per carload for U.S. Class I railroads was approximately $2,500.

- Trucking's market share for freight is around 70%, indicating the significant competitive pressure from this mode.

- Norfolk Southern's operating ratio (operating expenses as a percentage of revenue) was about 63% in 2024, showing the efficiency needed to manage costs.

- Fuel costs and labor expenses significantly impact pricing strategies.

Service quality and reliability

Railroads fiercely compete on service quality and reliability, key for customer satisfaction. This includes crucial aspects like on-time delivery and ensuring safety standards. Superior service is critical for securing and maintaining customer loyalty, influencing market share. Norfolk Southern's ability to provide dependable, high-quality service is directly tied to its competitive standing.

- In 2024, Norfolk Southern's operating ratio was around 64%, indicating efficiency.

- On-time performance data shows fluctuations, emphasizing the need for continuous improvement.

- Safety metrics, such as accident rates, are constantly monitored to enhance service quality.

- Customer satisfaction surveys provide insights into service strengths and weaknesses.

Railroad Rivals: A High-Stakes Game

Competitive rivalry in the railroad industry is intense, primarily due to a few major players like Norfolk Southern, CSX, and Union Pacific. These companies compete on network reach, operational efficiency, and service quality. In 2024, the average revenue per carload for U.S. Class I railroads was about $2,500, reflecting the economic stakes. Price competition and trucking's 70% market share add further pressure.

| Aspect | Details |

|---|---|

| Key Competitors | CSX, Union Pacific, BNSF |

| 2024 Avg. Revenue/Carload | ~$2,500 |

| Trucking Market Share | ~70% |

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

What is included in the product

Tailored exclusively for Norfolk Southern, analyzing its position within its competitive landscape.

Instantly highlight Porter's Five Forces' strategic impact on Norfolk Southern with a clear visualization.

What You See Is What You Get

Norfolk Southern Corporation Porter's Five Forces Analysis

This preview is the complete analysis. It's the exact Porter's Five Forces document you'll receive. It comprehensively analyzes Norfolk Southern. The content and formatting are identical in the purchased file.

Porter's Five Forces Analysis Template

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Norfolk Southern's industry faces moderate rivalry, influenced by a few major players and high capital investments. Buyer power is considerable, with large shippers able to negotiate rates. Supplier power is generally low, with readily available inputs. The threat of new entrants is limited due to high barriers. The threat of substitutes like trucking exists, but rail offers advantages.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Norfolk Southern Corporation’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Limited number of key suppliers

Norfolk Southern's dependence on a few suppliers, like locomotive manufacturers, boosts their bargaining power. This concentration lets suppliers dictate prices and terms more effectively. In 2024, about 70% of new locomotives came from just two companies. This gives suppliers significant pricing leverage, impacting Norfolk Southern's costs.

High switching costs for alternative suppliers

Norfolk Southern faces high switching costs, especially with specialized rail infrastructure. Changing suppliers for critical components and equipment, such as locomotives and signaling systems, is expensive. These costs include integration, testing, and logistics, increasing supplier bargaining power. For example, in 2024, the company spent $1.8 billion on capital expenditures, a portion of which went to specialized equipment where switching costs are high.

Increased demand for raw materials impacting supplier leverage

Norfolk Southern's supplier bargaining power is influenced by raw material demand. The need for steel and coal, essential for rail operations, gives suppliers leverage. In 2024, steel prices saw fluctuations, impacting operating costs. These cost shifts can affect profitability.

Potential for vertical integration by suppliers

If Norfolk Southern's suppliers integrated vertically, offering competitive services, their leverage would spike. This would challenge Norfolk Southern's control over costs and service terms. Such integration could reshape the supply landscape, impacting profitability. The possibility compels Norfolk Southern to strategize supplier relations proactively.

- In 2024, Norfolk Southern spent billions on materials and services, highlighting supplier importance.

- Vertical integration could lead to suppliers directly serving customers, bypassing Norfolk Southern.

- This risk necessitates robust supply chain management and strategic partnerships.

Quality and reliability impact operational efficiency

Norfolk Southern's operational success hinges on the quality and dependability of its suppliers. Poor-quality materials or unreliable equipment can cause significant disruptions, leading to increased expenses and potential safety issues. This dependence grants suppliers, especially those offering superior products, increased leverage in negotiations. For instance, a 2024 report showed that equipment failures caused a 10% increase in maintenance costs for the rail industry, highlighting the impact of supplier reliability.

- Supplier quality directly affects operational efficiency and safety.

- Unreliable suppliers can lead to disruptions and higher costs.

- Superior product suppliers gain more bargaining power.

- In 2024, equipment failures raised maintenance costs by 10%.

Supplier Power Dynamics: A Look at Key Factors

Norfolk Southern's supplier power stems from its reliance on few providers, like locomotive makers. High switching costs for specialized rail tech boost supplier leverage. Raw material needs, like steel, also give suppliers bargaining power.

| Factor | Impact | 2024 Data |

|---|---|---|

| Supplier Concentration | Higher prices | 70% of new locomotives from 2 firms |

| Switching Costs | Expensive changes | $1.8B CapEx on specialized gear |

| Raw Materials | Cost fluctuations | Steel price volatility |

Customers Bargaining Power

Diverse customer base with varying transportation needs

Norfolk Southern's customer base spans agriculture, automotive, and coal, among other sectors. Customer power varies by freight type and volume. In 2024, the company moved approximately 1.3 million carloads of merchandise. This diversity lessens the impact of any single customer's bargaining power.

Large shippers have more negotiating power

Major customers, like Amazon and UPS, wield considerable bargaining power due to the substantial volumes of goods they ship. These large shippers often secure long-term contracts, which allows them to negotiate favorable rates and service agreements. In 2024, Norfolk Southern's top ten customers accounted for approximately 25% of its revenue, highlighting the impact of these key accounts. The ability of these customers to shift to other transportation modes further strengthens their negotiating position.

Price sensitivity among smaller customers

Smaller customers, potentially less powerful individually, are often highly price-sensitive. Yet, their combined demand significantly impacts pricing decisions. For example, a 2024 study showed that even a 1% price increase can cause a 2-3% drop in volume for some customer segments. This sensitivity forces Norfolk Southern to balance price with volume to maintain profitability. This is a crucial aspect of the company's strategy.

Increased demand for intermodal services enhances customer choice

The rise of intermodal services gives customers more choices, potentially boosting their bargaining power. This increased competition can lead to lower prices and better service terms for shippers. Norfolk Southern faces this pressure as customers can now easily switch between various transportation methods. For example, in 2024, intermodal traffic accounted for a significant portion of overall freight volume.

- Intermodal growth offers shippers more alternatives.

- Customers can negotiate better rates and service levels.

- Competition among carriers intensifies.

- Norfolk Southern's pricing strategies are affected.

Long-term contracts can stabilize pricing

While large customers might wield significant influence, Norfolk Southern's long-term contracts offer a buffer. These contracts ensure price stability for both the company and its clients. For instance, in 2023, approximately 60% of Norfolk Southern's revenue came from contracted business, showcasing the importance of these agreements. This strategy reduces immediate pressure from fluctuating market conditions.

- Contracted revenue provides predictability.

- Long-term agreements reduce price volatility.

- Stability benefits both Norfolk Southern and customers.

- Approximately 60% of revenue from contracts in 2023.

Customer Power & Revenue Dynamics

Customer bargaining power varies based on shipment size and mode choice. Large customers like Amazon and UPS can negotiate favorable terms, influencing pricing. In 2024, the top 10 customers generated about 25% of Norfolk Southern's revenue. Long-term contracts provide some stability, with 60% of revenue from contracts in 2023.

| Aspect | Impact | 2024 Data |

|---|---|---|

| Customer Size | Influences Pricing | Top 10 Customers: ~25% Revenue |

| Contractual Agreements | Provides Stability | ~60% Revenue (2023) |

| Intermodal Growth | Increases Options | Significant Freight Volume |

Rivalry Among Competitors

Presence of multiple major railroads increases competition

Norfolk Southern faces intense competition because the railroad industry is dominated by a few major players. Key competitors include CSX, Union Pacific, and BNSF. This concentration means each railroad fights hard for market share. In 2024, these competitors collectively handled billions of dollars worth of freight, highlighting the stakes.

Competitive network capabilities

Rival railroads vie on network reach and efficiency. Norfolk Southern (NSC) boasts a strong network, a competitive edge. In Q3 2023, NSC's operating ratio was 62.3%, reflecting operational efficiency. This network supports diverse freight, critical for customer service.

Infrastructure and technology investment

Norfolk Southern (NSC) and its rivals heavily invest in infrastructure and technology. NSC's capital expenditures in 2023 were around $1.6 billion. These investments enhance operational efficiency and safety.

Price competition for freight traffic

Price competition is fierce in the freight industry, heavily influencing Norfolk Southern Corporation's (NSC) competitive environment. Railroads frequently adjust rates to secure business, particularly for bulk commodities where trucking or other transport methods are viable alternatives. This pricing pressure can affect profitability, as NSC and its rivals vie to offer the most attractive rates while managing operational costs. The ability to offer competitive pricing, while maintaining service quality, is crucial for retaining and gaining market share.

- In 2024, the average revenue per carload for U.S. Class I railroads was approximately $2,500.

- Trucking's market share for freight is around 70%, indicating the significant competitive pressure from this mode.

- Norfolk Southern's operating ratio (operating expenses as a percentage of revenue) was about 63% in 2024, showing the efficiency needed to manage costs.

- Fuel costs and labor expenses significantly impact pricing strategies.

Service quality and reliability

Railroads fiercely compete on service quality and reliability, key for customer satisfaction. This includes crucial aspects like on-time delivery and ensuring safety standards. Superior service is critical for securing and maintaining customer loyalty, influencing market share. Norfolk Southern's ability to provide dependable, high-quality service is directly tied to its competitive standing.

- In 2024, Norfolk Southern's operating ratio was around 64%, indicating efficiency.

- On-time performance data shows fluctuations, emphasizing the need for continuous improvement.

- Safety metrics, such as accident rates, are constantly monitored to enhance service quality.

- Customer satisfaction surveys provide insights into service strengths and weaknesses.

Railroad Rivals: A High-Stakes Game

Competitive rivalry in the railroad industry is intense, primarily due to a few major players like Norfolk Southern, CSX, and Union Pacific. These companies compete on network reach, operational efficiency, and service quality. In 2024, the average revenue per carload for U.S. Class I railroads was about $2,500, reflecting the economic stakes. Price competition and trucking's 70% market share add further pressure.

| Aspect | Details |

|---|---|

| Key Competitors | CSX, Union Pacific, BNSF |

| 2024 Avg. Revenue/Carload | ~$2,500 |

| Trucking Market Share | ~70% |