QCELLS PORTER'S FIVE FORCES TEMPLATE RESEARCH

What is included in the product

Detailed analysis of each competitive force, supported by industry data and strategic commentary.

Swap in your own data and labels to reflect current business conditions.

What You See Is What You Get

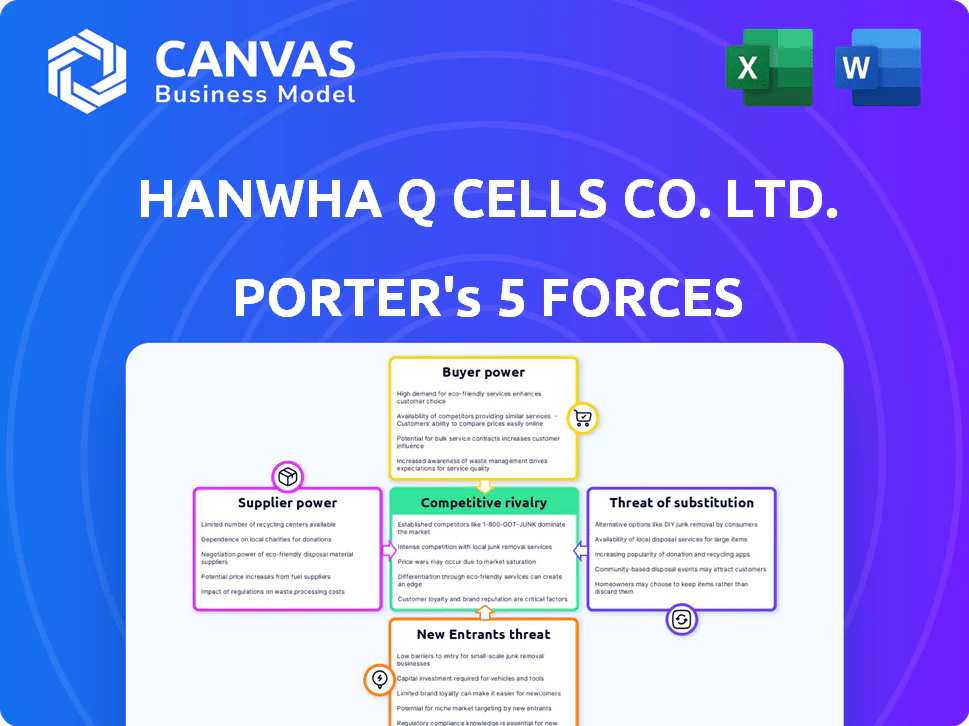

Qcells Porter's Five Forces Analysis

This preview showcases the complete Qcells Porter's Five Forces analysis. The document you see here is identical to the one you'll receive immediately after purchase. It's a fully prepared, ready-to-use analysis. There are no differences; it's the same file. Get instant access after your purchase.

Porter's Five Forces Analysis Template

Don't Miss the Bigger Picture

Qcells faces intense competition, particularly from established solar manufacturers and emerging players. Buyer power is moderate, influenced by project size and government incentives. Supplier power is significant, tied to raw material costs and supply chain dynamics. The threat of new entrants is notable, given the industry's growth and technological advancements. Substitute products, primarily conventional energy sources, present a moderate threat.

Ready to move beyond the basics? Get a full strategic breakdown of Qcells’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Limited Raw Material Suppliers

Qcells' supplier power is notably influenced by limited raw material suppliers. The solar industry depends on silicon, silver, and rare earth metals. A few firms dominate silicon production, boosting their leverage over manufacturers. In 2024, silicon prices fluctuated, impacting solar panel costs significantly. This concentration of suppliers allows them to dictate terms.

High Switching Costs for Suppliers

Switching suppliers is costly for solar manufacturers. Requalifying materials from a new supplier can take months. This hesitancy to change suppliers allows existing suppliers to exert more power. For example, the cost of requalification can reach hundreds of thousands of dollars. This was especially evident in 2024 with supply chain disruptions.

Supplier Specialization in Advanced Technologies

As solar tech evolves, specialized suppliers gain power. They offer unique, high-efficiency components. For Qcells, few alternatives exist for these advanced parts. For example, in 2024, the cost of polysilicon, a key solar material, has fluctuated significantly, impacting supplier bargaining power.

Impact of Vertical Integration

Vertical integration, where companies control multiple steps in the supply chain, significantly impacts supplier bargaining power. By manufacturing components like ingots and wafers internally, Qcells reduces reliance on external suppliers. This strategic move allows for better negotiation of prices and terms, enhancing cost control.

- Qcells has invested heavily in vertically integrated manufacturing, including polysilicon production.

- In 2024, Qcells' expansion plans include increasing in-house wafer production capacity.

- This vertical integration strategy aims to reduce external supplier costs by 10-15%.

Geopolitical Factors and Supply Chain Concentration

The solar supply chain's concentration in China grants suppliers substantial bargaining power. Geopolitical factors and trade policies, like those impacting solar panel imports, amplify this influence. For instance, in 2024, China controlled over 80% of global polysilicon production, a key solar panel component, affecting pricing. This concentration creates vulnerabilities.

- China's dominance in polysilicon: Over 80% of global production.

- Trade policies: Tariffs and import regulations affect material costs.

- Geopolitical tensions: Can disrupt supply and increase prices.

- Supplier control: Gives suppliers significant price-setting power.

Supplier Power Dynamics in Solar Manufacturing

Qcells faces supplier power challenges due to concentrated raw material sources and high switching costs. Vertical integration, like in-house wafer production, helps mitigate supplier influence. However, geopolitical factors, particularly China's dominance in polysilicon, amplify supplier bargaining power.

| Aspect | Details | Impact |

|---|---|---|

| Polysilicon Supply | China controls over 80% of global production. | High supplier bargaining power, price volatility. |

| Vertical Integration | Qcells' in-house wafer production expansion. | Reduces external supplier costs by 10-15%. |

| Switching Costs | Requalification of new materials can take months. | High switching costs, supplier leverage. |

Customers Bargaining Power

Increasing Awareness and Demand for Renewable Energy

The rising global awareness of climate change and the advantages of renewable energy is fueling demand for solar solutions. This shift broadens the market, providing customers with more choices. For example, in 2024, solar energy capacity additions globally reached record levels. This increasing demand potentially gives customers more bargaining power.

Availability of Online Comparison Platforms

Online platforms create price transparency, enabling customers to easily compare solar panel quotes. This heightened visibility empowers customers, bolstering their negotiation leverage. In 2024, the use of online comparison tools grew by 15%, driving down prices in the solar market. Increased price awareness directly impacts a company's ability to set prices.

Potential for Bulk Purchasing Discounts

Large-scale solar projects, like utility-scale installations, involve substantial purchase volumes. Customers, such as large energy firms, often negotiate bulk discounts, wielding significant bargaining power. For example, in 2024, the average price of solar panels decreased, providing more leverage for these buyers. This trend allows them to influence pricing and terms. These customers can also switch between suppliers, further increasing their power.

Customer Seeking Cost-Effective Solutions

Customers are increasingly prioritizing cost-effective solar solutions, evaluating initial investments and long-term savings. The falling costs of solar PV systems have significantly empowered customers. This makes solar more accessible and affordable. In 2024, the average cost of a residential solar system decreased.

- The cost of solar PV systems dropped by 10-15% in 2024.

- Residential solar prices are now around $2.80-$3.50 per watt.

- Customers can compare different solar panel brands.

Availability of Different Solar Products and Solutions

Qcells' diverse offerings, from modules to energy storage, impact customer bargaining power. This variety caters to different needs, influencing customer choices. Integrated solutions, like those for residential or commercial use, further shape customer decisions. However, intense competition and readily available alternatives can strengthen customer bargaining power. In 2024, the solar market saw a 10% increase in product options.

- Diverse product range caters to various customer needs.

- Integrated solutions influence customer choices.

- Competition and alternatives impact bargaining power.

- 2024 saw a 10% increase in product options.

Solar Power: Buyer Power Surges!

Customer bargaining power in the solar market is rising due to increased choice and price transparency. Online tools and bulk purchases enhance negotiation leverage for buyers. In 2024, cost-conscious customers benefited from falling solar PV system costs.

| Factor | Impact | 2024 Data |

|---|---|---|

| Price Transparency | Easier price comparison | Online comparison tool use grew by 15% |

| Bulk Purchases | Negotiated discounts | Average solar panel prices decreased |

| Cost Focus | Prioritize cost-effectiveness | Residential solar system cost decreased |

Rivalry Among Competitors

Intense Competition in the Global Solar Market

The global solar market is fiercely competitive. Qcells faces rivals like international manufacturers and regional players. In 2024, the top 10 solar module suppliers controlled about 80% of the market. This intense competition can squeeze profit margins. The market is constantly evolving, with new technologies and entrants.

Price Wars and Impact on Profit Margins

Aggressive price competition is a reality in the solar market, potentially squeezing Qcells' profit margins. The falling costs of solar modules fuel this price-based rivalry. For instance, in 2024, global solar module prices decreased, intensifying the competition. This can lead to reduced profitability for all players. The impact is felt across the industry.

Technological Advancements and Innovation

Competition in the solar industry is fierce, fueled by rapid technological advancements. Qcells, for instance, competes by investing in R&D. In 2024, the solar panel market saw a 10% increase in efficiency. This drive innovation, with companies constantly seeking better performance. Qcells' Q.ANTUM tech is an example of this.

Market Share and Leading Positions

The solar market is competitive, yet certain firms have substantial market shares in particular areas. Qcells has been a prominent player in the U.S. residential and commercial solar module markets. This shows its strong competitive position amidst the rivalry. In 2024, Qcells held over 30% of the U.S. residential market. This underscores its significant competitive presence.

- Qcells held over 30% of the U.S. residential market in 2024.

- Competitive rivalry is high due to the presence of numerous competitors.

- Market share varies across different segments.

- Leading positions indicate the ability to compete effectively.

Government Policies and Trade Measures

Government policies and trade measures heavily affect competition within the solar industry. Tariffs and import duties, like those seen in the U.S. on imported solar panels, can increase costs for some companies. These policies can favor domestic manufacturers, intensifying rivalry among firms. Government incentives, such as tax credits, also shape the competitive environment.

- In 2024, the U.S. extended tariffs on imported solar panels, influencing market dynamics.

- Tax credits, such as those under the Inflation Reduction Act, boosted domestic solar manufacturing.

- Trade disputes and policy changes constantly reshape competitive advantages.

- China's dominance in solar manufacturing faces challenges from these measures.

Solar Market's Fierce Battle: Qcells' Position

Competitive rivalry in the solar market is intense, with many players vying for market share. Qcells competes in a market where top 10 suppliers controlled ~80% of the market in 2024. Price competition is fierce, affecting profitability across the industry.

| Aspect | Details | 2024 Data |

|---|---|---|

| Market Share Control | Top 10 Solar Module Suppliers | ~80% of the market |

| Price Decline | Global Solar Module Prices | Decreased |

| U.S. Residential Market Share | Qcells | Over 30% |

Original: $10.00

-65%$10.00

$3.50QCELLS PORTER'S FIVE FORCES TEMPLATE RESEARCH

What is included in the product

Detailed analysis of each competitive force, supported by industry data and strategic commentary.

Swap in your own data and labels to reflect current business conditions.

What You See Is What You Get

Qcells Porter's Five Forces Analysis

This preview showcases the complete Qcells Porter's Five Forces analysis. The document you see here is identical to the one you'll receive immediately after purchase. It's a fully prepared, ready-to-use analysis. There are no differences; it's the same file. Get instant access after your purchase.

Porter's Five Forces Analysis Template

Don't Miss the Bigger Picture

Qcells faces intense competition, particularly from established solar manufacturers and emerging players. Buyer power is moderate, influenced by project size and government incentives. Supplier power is significant, tied to raw material costs and supply chain dynamics. The threat of new entrants is notable, given the industry's growth and technological advancements. Substitute products, primarily conventional energy sources, present a moderate threat.

Ready to move beyond the basics? Get a full strategic breakdown of Qcells’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Limited Raw Material Suppliers

Qcells' supplier power is notably influenced by limited raw material suppliers. The solar industry depends on silicon, silver, and rare earth metals. A few firms dominate silicon production, boosting their leverage over manufacturers. In 2024, silicon prices fluctuated, impacting solar panel costs significantly. This concentration of suppliers allows them to dictate terms.

High Switching Costs for Suppliers

Switching suppliers is costly for solar manufacturers. Requalifying materials from a new supplier can take months. This hesitancy to change suppliers allows existing suppliers to exert more power. For example, the cost of requalification can reach hundreds of thousands of dollars. This was especially evident in 2024 with supply chain disruptions.

Supplier Specialization in Advanced Technologies

As solar tech evolves, specialized suppliers gain power. They offer unique, high-efficiency components. For Qcells, few alternatives exist for these advanced parts. For example, in 2024, the cost of polysilicon, a key solar material, has fluctuated significantly, impacting supplier bargaining power.

Impact of Vertical Integration

Vertical integration, where companies control multiple steps in the supply chain, significantly impacts supplier bargaining power. By manufacturing components like ingots and wafers internally, Qcells reduces reliance on external suppliers. This strategic move allows for better negotiation of prices and terms, enhancing cost control.

- Qcells has invested heavily in vertically integrated manufacturing, including polysilicon production.

- In 2024, Qcells' expansion plans include increasing in-house wafer production capacity.

- This vertical integration strategy aims to reduce external supplier costs by 10-15%.

Geopolitical Factors and Supply Chain Concentration

The solar supply chain's concentration in China grants suppliers substantial bargaining power. Geopolitical factors and trade policies, like those impacting solar panel imports, amplify this influence. For instance, in 2024, China controlled over 80% of global polysilicon production, a key solar panel component, affecting pricing. This concentration creates vulnerabilities.

- China's dominance in polysilicon: Over 80% of global production.

- Trade policies: Tariffs and import regulations affect material costs.

- Geopolitical tensions: Can disrupt supply and increase prices.

- Supplier control: Gives suppliers significant price-setting power.

Supplier Power Dynamics in Solar Manufacturing

Qcells faces supplier power challenges due to concentrated raw material sources and high switching costs. Vertical integration, like in-house wafer production, helps mitigate supplier influence. However, geopolitical factors, particularly China's dominance in polysilicon, amplify supplier bargaining power.

| Aspect | Details | Impact |

|---|---|---|

| Polysilicon Supply | China controls over 80% of global production. | High supplier bargaining power, price volatility. |

| Vertical Integration | Qcells' in-house wafer production expansion. | Reduces external supplier costs by 10-15%. |

| Switching Costs | Requalification of new materials can take months. | High switching costs, supplier leverage. |

Customers Bargaining Power

Increasing Awareness and Demand for Renewable Energy

The rising global awareness of climate change and the advantages of renewable energy is fueling demand for solar solutions. This shift broadens the market, providing customers with more choices. For example, in 2024, solar energy capacity additions globally reached record levels. This increasing demand potentially gives customers more bargaining power.

Availability of Online Comparison Platforms

Online platforms create price transparency, enabling customers to easily compare solar panel quotes. This heightened visibility empowers customers, bolstering their negotiation leverage. In 2024, the use of online comparison tools grew by 15%, driving down prices in the solar market. Increased price awareness directly impacts a company's ability to set prices.

Potential for Bulk Purchasing Discounts

Large-scale solar projects, like utility-scale installations, involve substantial purchase volumes. Customers, such as large energy firms, often negotiate bulk discounts, wielding significant bargaining power. For example, in 2024, the average price of solar panels decreased, providing more leverage for these buyers. This trend allows them to influence pricing and terms. These customers can also switch between suppliers, further increasing their power.

Customer Seeking Cost-Effective Solutions

Customers are increasingly prioritizing cost-effective solar solutions, evaluating initial investments and long-term savings. The falling costs of solar PV systems have significantly empowered customers. This makes solar more accessible and affordable. In 2024, the average cost of a residential solar system decreased.

- The cost of solar PV systems dropped by 10-15% in 2024.

- Residential solar prices are now around $2.80-$3.50 per watt.

- Customers can compare different solar panel brands.

Availability of Different Solar Products and Solutions

Qcells' diverse offerings, from modules to energy storage, impact customer bargaining power. This variety caters to different needs, influencing customer choices. Integrated solutions, like those for residential or commercial use, further shape customer decisions. However, intense competition and readily available alternatives can strengthen customer bargaining power. In 2024, the solar market saw a 10% increase in product options.

- Diverse product range caters to various customer needs.

- Integrated solutions influence customer choices.

- Competition and alternatives impact bargaining power.

- 2024 saw a 10% increase in product options.

Solar Power: Buyer Power Surges!

Customer bargaining power in the solar market is rising due to increased choice and price transparency. Online tools and bulk purchases enhance negotiation leverage for buyers. In 2024, cost-conscious customers benefited from falling solar PV system costs.

| Factor | Impact | 2024 Data |

|---|---|---|

| Price Transparency | Easier price comparison | Online comparison tool use grew by 15% |

| Bulk Purchases | Negotiated discounts | Average solar panel prices decreased |

| Cost Focus | Prioritize cost-effectiveness | Residential solar system cost decreased |

Rivalry Among Competitors

Intense Competition in the Global Solar Market

The global solar market is fiercely competitive. Qcells faces rivals like international manufacturers and regional players. In 2024, the top 10 solar module suppliers controlled about 80% of the market. This intense competition can squeeze profit margins. The market is constantly evolving, with new technologies and entrants.

Price Wars and Impact on Profit Margins

Aggressive price competition is a reality in the solar market, potentially squeezing Qcells' profit margins. The falling costs of solar modules fuel this price-based rivalry. For instance, in 2024, global solar module prices decreased, intensifying the competition. This can lead to reduced profitability for all players. The impact is felt across the industry.

Technological Advancements and Innovation

Competition in the solar industry is fierce, fueled by rapid technological advancements. Qcells, for instance, competes by investing in R&D. In 2024, the solar panel market saw a 10% increase in efficiency. This drive innovation, with companies constantly seeking better performance. Qcells' Q.ANTUM tech is an example of this.

Market Share and Leading Positions

The solar market is competitive, yet certain firms have substantial market shares in particular areas. Qcells has been a prominent player in the U.S. residential and commercial solar module markets. This shows its strong competitive position amidst the rivalry. In 2024, Qcells held over 30% of the U.S. residential market. This underscores its significant competitive presence.

- Qcells held over 30% of the U.S. residential market in 2024.

- Competitive rivalry is high due to the presence of numerous competitors.

- Market share varies across different segments.

- Leading positions indicate the ability to compete effectively.

Government Policies and Trade Measures

Government policies and trade measures heavily affect competition within the solar industry. Tariffs and import duties, like those seen in the U.S. on imported solar panels, can increase costs for some companies. These policies can favor domestic manufacturers, intensifying rivalry among firms. Government incentives, such as tax credits, also shape the competitive environment.

- In 2024, the U.S. extended tariffs on imported solar panels, influencing market dynamics.

- Tax credits, such as those under the Inflation Reduction Act, boosted domestic solar manufacturing.

- Trade disputes and policy changes constantly reshape competitive advantages.

- China's dominance in solar manufacturing faces challenges from these measures.

Solar Market's Fierce Battle: Qcells' Position

Competitive rivalry in the solar market is intense, with many players vying for market share. Qcells competes in a market where top 10 suppliers controlled ~80% of the market in 2024. Price competition is fierce, affecting profitability across the industry.

| Aspect | Details | 2024 Data |

|---|---|---|

| Market Share Control | Top 10 Solar Module Suppliers | ~80% of the market |

| Price Decline | Global Solar Module Prices | Decreased |

| U.S. Residential Market Share | Qcells | Over 30% |

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

What is included in the product

Detailed analysis of each competitive force, supported by industry data and strategic commentary.

Swap in your own data and labels to reflect current business conditions.

What You See Is What You Get

Qcells Porter's Five Forces Analysis

This preview showcases the complete Qcells Porter's Five Forces analysis. The document you see here is identical to the one you'll receive immediately after purchase. It's a fully prepared, ready-to-use analysis. There are no differences; it's the same file. Get instant access after your purchase.

Porter's Five Forces Analysis Template

Don't Miss the Bigger Picture

Qcells faces intense competition, particularly from established solar manufacturers and emerging players. Buyer power is moderate, influenced by project size and government incentives. Supplier power is significant, tied to raw material costs and supply chain dynamics. The threat of new entrants is notable, given the industry's growth and technological advancements. Substitute products, primarily conventional energy sources, present a moderate threat.

Ready to move beyond the basics? Get a full strategic breakdown of Qcells’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Limited Raw Material Suppliers

Qcells' supplier power is notably influenced by limited raw material suppliers. The solar industry depends on silicon, silver, and rare earth metals. A few firms dominate silicon production, boosting their leverage over manufacturers. In 2024, silicon prices fluctuated, impacting solar panel costs significantly. This concentration of suppliers allows them to dictate terms.

High Switching Costs for Suppliers

Switching suppliers is costly for solar manufacturers. Requalifying materials from a new supplier can take months. This hesitancy to change suppliers allows existing suppliers to exert more power. For example, the cost of requalification can reach hundreds of thousands of dollars. This was especially evident in 2024 with supply chain disruptions.

Supplier Specialization in Advanced Technologies

As solar tech evolves, specialized suppliers gain power. They offer unique, high-efficiency components. For Qcells, few alternatives exist for these advanced parts. For example, in 2024, the cost of polysilicon, a key solar material, has fluctuated significantly, impacting supplier bargaining power.

Impact of Vertical Integration

Vertical integration, where companies control multiple steps in the supply chain, significantly impacts supplier bargaining power. By manufacturing components like ingots and wafers internally, Qcells reduces reliance on external suppliers. This strategic move allows for better negotiation of prices and terms, enhancing cost control.

- Qcells has invested heavily in vertically integrated manufacturing, including polysilicon production.

- In 2024, Qcells' expansion plans include increasing in-house wafer production capacity.

- This vertical integration strategy aims to reduce external supplier costs by 10-15%.

Geopolitical Factors and Supply Chain Concentration

The solar supply chain's concentration in China grants suppliers substantial bargaining power. Geopolitical factors and trade policies, like those impacting solar panel imports, amplify this influence. For instance, in 2024, China controlled over 80% of global polysilicon production, a key solar panel component, affecting pricing. This concentration creates vulnerabilities.

- China's dominance in polysilicon: Over 80% of global production.

- Trade policies: Tariffs and import regulations affect material costs.

- Geopolitical tensions: Can disrupt supply and increase prices.

- Supplier control: Gives suppliers significant price-setting power.

Supplier Power Dynamics in Solar Manufacturing

Qcells faces supplier power challenges due to concentrated raw material sources and high switching costs. Vertical integration, like in-house wafer production, helps mitigate supplier influence. However, geopolitical factors, particularly China's dominance in polysilicon, amplify supplier bargaining power.

| Aspect | Details | Impact |

|---|---|---|

| Polysilicon Supply | China controls over 80% of global production. | High supplier bargaining power, price volatility. |

| Vertical Integration | Qcells' in-house wafer production expansion. | Reduces external supplier costs by 10-15%. |

| Switching Costs | Requalification of new materials can take months. | High switching costs, supplier leverage. |

Customers Bargaining Power

Increasing Awareness and Demand for Renewable Energy

The rising global awareness of climate change and the advantages of renewable energy is fueling demand for solar solutions. This shift broadens the market, providing customers with more choices. For example, in 2024, solar energy capacity additions globally reached record levels. This increasing demand potentially gives customers more bargaining power.

Availability of Online Comparison Platforms

Online platforms create price transparency, enabling customers to easily compare solar panel quotes. This heightened visibility empowers customers, bolstering their negotiation leverage. In 2024, the use of online comparison tools grew by 15%, driving down prices in the solar market. Increased price awareness directly impacts a company's ability to set prices.

Potential for Bulk Purchasing Discounts

Large-scale solar projects, like utility-scale installations, involve substantial purchase volumes. Customers, such as large energy firms, often negotiate bulk discounts, wielding significant bargaining power. For example, in 2024, the average price of solar panels decreased, providing more leverage for these buyers. This trend allows them to influence pricing and terms. These customers can also switch between suppliers, further increasing their power.

Customer Seeking Cost-Effective Solutions

Customers are increasingly prioritizing cost-effective solar solutions, evaluating initial investments and long-term savings. The falling costs of solar PV systems have significantly empowered customers. This makes solar more accessible and affordable. In 2024, the average cost of a residential solar system decreased.

- The cost of solar PV systems dropped by 10-15% in 2024.

- Residential solar prices are now around $2.80-$3.50 per watt.

- Customers can compare different solar panel brands.

Availability of Different Solar Products and Solutions

Qcells' diverse offerings, from modules to energy storage, impact customer bargaining power. This variety caters to different needs, influencing customer choices. Integrated solutions, like those for residential or commercial use, further shape customer decisions. However, intense competition and readily available alternatives can strengthen customer bargaining power. In 2024, the solar market saw a 10% increase in product options.

- Diverse product range caters to various customer needs.

- Integrated solutions influence customer choices.

- Competition and alternatives impact bargaining power.

- 2024 saw a 10% increase in product options.

Solar Power: Buyer Power Surges!

Customer bargaining power in the solar market is rising due to increased choice and price transparency. Online tools and bulk purchases enhance negotiation leverage for buyers. In 2024, cost-conscious customers benefited from falling solar PV system costs.

| Factor | Impact | 2024 Data |

|---|---|---|

| Price Transparency | Easier price comparison | Online comparison tool use grew by 15% |

| Bulk Purchases | Negotiated discounts | Average solar panel prices decreased |

| Cost Focus | Prioritize cost-effectiveness | Residential solar system cost decreased |

Rivalry Among Competitors

Intense Competition in the Global Solar Market

The global solar market is fiercely competitive. Qcells faces rivals like international manufacturers and regional players. In 2024, the top 10 solar module suppliers controlled about 80% of the market. This intense competition can squeeze profit margins. The market is constantly evolving, with new technologies and entrants.

Price Wars and Impact on Profit Margins

Aggressive price competition is a reality in the solar market, potentially squeezing Qcells' profit margins. The falling costs of solar modules fuel this price-based rivalry. For instance, in 2024, global solar module prices decreased, intensifying the competition. This can lead to reduced profitability for all players. The impact is felt across the industry.

Technological Advancements and Innovation

Competition in the solar industry is fierce, fueled by rapid technological advancements. Qcells, for instance, competes by investing in R&D. In 2024, the solar panel market saw a 10% increase in efficiency. This drive innovation, with companies constantly seeking better performance. Qcells' Q.ANTUM tech is an example of this.

Market Share and Leading Positions

The solar market is competitive, yet certain firms have substantial market shares in particular areas. Qcells has been a prominent player in the U.S. residential and commercial solar module markets. This shows its strong competitive position amidst the rivalry. In 2024, Qcells held over 30% of the U.S. residential market. This underscores its significant competitive presence.

- Qcells held over 30% of the U.S. residential market in 2024.

- Competitive rivalry is high due to the presence of numerous competitors.

- Market share varies across different segments.

- Leading positions indicate the ability to compete effectively.

Government Policies and Trade Measures

Government policies and trade measures heavily affect competition within the solar industry. Tariffs and import duties, like those seen in the U.S. on imported solar panels, can increase costs for some companies. These policies can favor domestic manufacturers, intensifying rivalry among firms. Government incentives, such as tax credits, also shape the competitive environment.

- In 2024, the U.S. extended tariffs on imported solar panels, influencing market dynamics.

- Tax credits, such as those under the Inflation Reduction Act, boosted domestic solar manufacturing.

- Trade disputes and policy changes constantly reshape competitive advantages.

- China's dominance in solar manufacturing faces challenges from these measures.

Solar Market's Fierce Battle: Qcells' Position

Competitive rivalry in the solar market is intense, with many players vying for market share. Qcells competes in a market where top 10 suppliers controlled ~80% of the market in 2024. Price competition is fierce, affecting profitability across the industry.

| Aspect | Details | 2024 Data |

|---|---|---|

| Market Share Control | Top 10 Solar Module Suppliers | ~80% of the market |

| Price Decline | Global Solar Module Prices | Decreased |

| U.S. Residential Market Share | Qcells | Over 30% |