THRIVE EARLIER DETECTION PORTER'S FIVE FORCES TEMPLATE RESEARCH

What is included in the product

Tailored exclusively for Thrive Earlier Detection, analyzing its position within its competitive landscape.

Instantly assess market pressure with a color-coded dashboard.

Full Version Awaits

Thrive Earlier Detection Porter's Five Forces Analysis

This preview provides the complete Porter's Five Forces analysis of Thrive Earlier Detection. You're viewing the exact, ready-to-use document you will receive instantly after purchase.

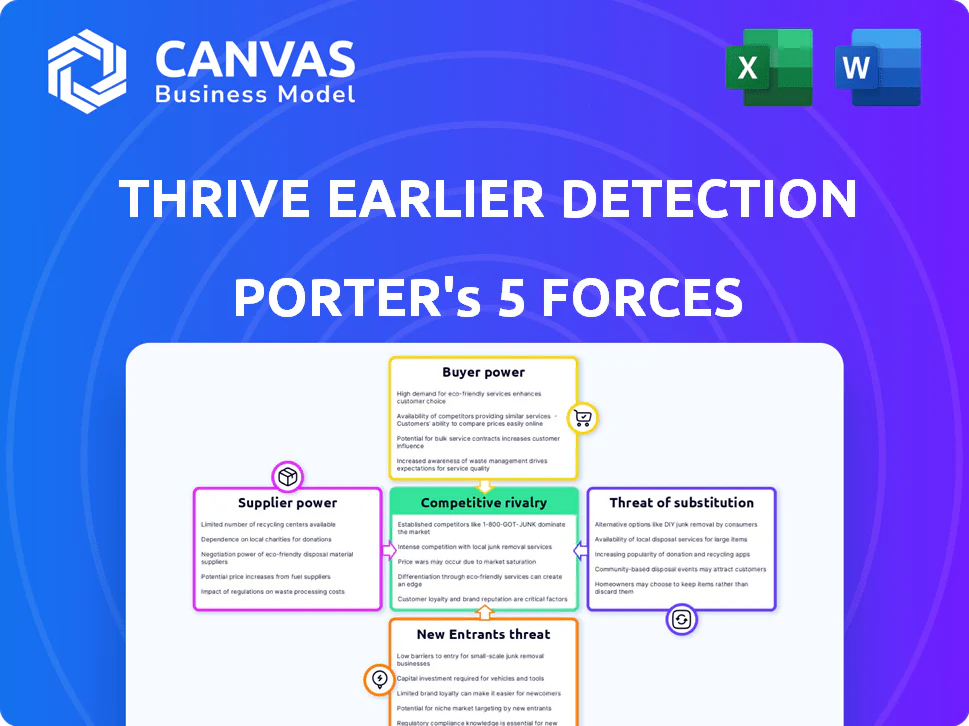

Porter's Five Forces Analysis Template

From Overview to Strategy Blueprint

Thrive Earlier Detection operates in a competitive market, influenced by factors such as buyer power from healthcare providers and patient choice. The threat of new entrants remains moderate, given the high regulatory hurdles and capital investments needed. Supplier power, particularly from technology providers, is a key dynamic. Substitute products, such as alternative cancer screening methods, pose a moderate threat. Competitive rivalry is intense, with several companies vying for market share.

Ready to move beyond the basics? Get a full strategic breakdown of Thrive Earlier Detection’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Reliance on Specialized Technology and Reagents

Thrive Earlier Detection, focusing on liquid biopsies, depends on specialized tech and reagents, like NGS. Suppliers of these, holding proprietary tech, wield considerable power. For example, in 2024, Illumina's NGS market share was over 80%. This dominance gives suppliers pricing leverage. Limited options increase this bargaining power.

Availability of Alternative Suppliers

Thrive Earlier Detection's ability to switch suppliers significantly influences supplier power. Having numerous reagent and equipment vendors strengthens Thrive's position. For example, the global in-vitro diagnostics market, which includes reagents, was valued at $87.2 billion in 2023. This provides Thrive with alternative options.

Uniqueness of Licensed Technology

Thrive's CancerSEEK tech, licensed from Johns Hopkins, gives the university initial supplier power. The exclusive agreement terms define Johns Hopkins' ongoing influence. In 2024, exclusive tech licenses often involve royalties, impacting Thrive's costs. Johns Hopkins' research budget in 2023 was roughly $3.2 billion.

Potential for Vertical Integration by Suppliers

If key suppliers, like those providing reagents or sequencing technology, could create their own cancer tests, Thrive would face a major threat. This vertical integration would transform suppliers into direct rivals, boosting their leverage. Such a move is a real concern in the health tech sector, where competition is always intense. The potential shift could significantly alter the market dynamics.

- In 2024, the global in-vitro diagnostics market was valued at over $90 billion, highlighting the scale of potential supplier moves.

- Companies like Roche and Illumina already have significant vertical integration, showing the feasibility and impact of such strategies.

- A supplier’s entry could erode Thrive’s market share and pricing power, affecting profitability.

- The rise of liquid biopsy tests, valued at $6.2 billion in 2024, makes supplier-led innovation a tangible threat.

Regulatory Landscape for Suppliers

Suppliers of diagnostic components face regulatory scrutiny, impacting their operations and costs. Regulations can significantly affect their bargaining power within the healthcare sector. For instance, the FDA's premarket approval process for medical devices can be costly and time-consuming. These regulatory hurdles can limit the number of qualified suppliers.

- FDA clearance can cost suppliers up to $100 million.

- Regulatory changes in 2024 increased compliance costs by 15%.

- Only 30% of suppliers meet all regulatory requirements.

- Compliance failures led to $50 million in penalties in 2024.

Thrive's Supplier Dynamics: Navigating Market Power

Thrive faces supplier power from tech and reagent providers, like Illumina, with over 80% NGS market share in 2024. Their leverage is offset by Thrive's ability to switch vendors and access to a $90B+ in-vitro diagnostics market. The CancerSEEK tech license from Johns Hopkins gives the university initial influence.

| Factor | Impact | Data (2024) |

|---|---|---|

| Supplier Concentration | High | Illumina's NGS share >80% |

| Switching Costs | Moderate | IVD market at $90B+ |

| License Agreements | Significant | Johns Hopkins' research budget $3.2B |

Customers Bargaining Power

Customer Base for Early Detection Tests

Thrive's customers include healthcare providers and patients. The bargaining power of these groups hinges on test volume and alternative options. In 2024, the early cancer detection market was valued at $3.5 billion. Competition from firms like Grail could influence pricing and adoption rates.

Impact of Reimbursement and Insurance Coverage

The willingness of payers to cover Thrive's tests is crucial. Insurance coverage directly impacts adoption and pricing. Payers, like UnitedHealthcare and Humana, wield power in reimbursement rate negotiations. Reimbursement rates directly affect revenue. In 2024, about 70% of cancer tests are covered by insurance.

Availability of Alternative Screening Methods

Customers can opt for established cancer screening methods, influencing their test adoption. These methods include mammograms and colonoscopies, with varying efficacy and patient acceptance. The American Cancer Society recommends regular screenings, impacting demand. In 2024, adoption rates for these tests will influence Thrive's market penetration and pricing strategies.

Influence of Healthcare Providers

Physicians and healthcare providers significantly influence test adoption. Their decisions directly impact Thrive's success. Provider acceptance and test integration are vital for revenue. Consider the role of medical societies and their guidelines.

- In 2024, approximately 80% of healthcare decisions are influenced by physicians.

- The American Medical Association (AMA) has over 270,000 members, potentially impacting test adoption.

- Clinical trial results and peer-reviewed publications heavily influence provider choices.

Patient Awareness and Demand

Patient awareness regarding early cancer detection is rising, potentially increasing demand for specific tests like those offered by Thrive Earlier Detection. As patients become more informed, they may actively seek out or request these tests from their healthcare providers. This shift can empower customers, though the actual impact depends on test accessibility and proven clinical benefits. The liquid biopsy market is projected to reach $14.5 billion by 2028, indicating significant customer influence.

- Growing patient knowledge fuels demand for early detection methods.

- Customer influence hinges on test availability and established value.

- The liquid biopsy market is forecasted to be worth $14.5B by 2028.

Thrive's Market Dynamics: Key Influencers

Customer bargaining power at Thrive is influenced by test availability and payer coverage. Strong competition from Grail and others impacts pricing and adoption. Physicians and patient awareness also play a key role in test utilization.

| Factor | Impact | 2024 Data |

|---|---|---|

| Payer Coverage | Influences Adoption | 70% of cancer tests covered by insurance |

| Competition | Affects Pricing | Early detection market: $3.5B |

| Patient Awareness | Drives Demand | Liquid biopsy market forecast: $14.5B by 2028 |

Rivalry Among Competitors

Number and Size of Competitors

The early cancer detection market is intensifying, with numerous competitors of varied sizes. GRAIL, Guardant Health, and Freenome are significant players. In 2024, the market saw over $1 billion in investments, indicating strong rivalry. This competition drives innovation and could lower prices.

Technological Innovation and Differentiation

Competition in early cancer detection is fierce, fueled by rapid technological advancements. Companies continuously innovate in liquid biopsy, exploring new biomarkers. Key competitive factors include test sensitivity, specificity, and the range of detectable cancers. For example, in 2024, Grail's Galleri test aims to detect over 50 cancers. The market is projected to reach $10.5 billion by 2030.

Market Growth Rate

The liquid biopsy and multi-cancer early detection markets are expanding quickly. This rapid growth fuels competition as companies compete for market share. In 2024, the global liquid biopsy market was valued at approximately $5.2 billion. This expansion creates opportunities for numerous companies to thrive.

Acquisition and Consolidation Activity

The competitive landscape of early cancer detection is experiencing a shake-up due to acquisitions. Exact Sciences' purchase of Thrive is a prime example, reshaping the market dynamics. This consolidation can lead to fewer but larger competitors, increasing their market power. Such moves often intensify rivalry as these bigger players battle for market share and resources.

- Exact Sciences acquired Thrive for $2.15 billion in 2020.

- The early cancer detection market is projected to reach $30.6 billion by 2030.

- Consolidation may lead to increased R&D spending by the larger entities.

Marketing and Sales Capabilities

Marketing and sales are vital for Thrive Earlier Detection, targeting healthcare providers and patients. Strong commercial infrastructure gives companies a competitive edge. Exact figures are proprietary, but marketing spend in similar sectors can be significant. Effective strategies drive adoption and market share.

- Commercial teams can influence market penetration.

- Marketing efforts shape brand awareness and trust.

- Sales cycles in healthcare are often lengthy.

- Established networks accelerate market entry.

Early Cancer Detection: A Fierce Battleground

Competitive rivalry in early cancer detection is intense. Companies aggressively pursue market share through innovation and strategic moves. The sector's projected value is $30.6 billion by 2030, fueling competition.

| Key Competitors | Focus | 2024 Data Highlights |

|---|---|---|

| GRAIL | Multi-cancer early detection | Galleri test aims to detect over 50 cancers. |

| Guardant Health | Liquid biopsy | $5.2B global liquid biopsy market in 2024. |

| Freenome | Multi-cancer early detection | Over $1B in market investments in 2024. |

Original: $10.00

-65%$10.00

$3.50THRIVE EARLIER DETECTION PORTER'S FIVE FORCES TEMPLATE RESEARCH

What is included in the product

Tailored exclusively for Thrive Earlier Detection, analyzing its position within its competitive landscape.

Instantly assess market pressure with a color-coded dashboard.

Full Version Awaits

Thrive Earlier Detection Porter's Five Forces Analysis

This preview provides the complete Porter's Five Forces analysis of Thrive Earlier Detection. You're viewing the exact, ready-to-use document you will receive instantly after purchase.

Porter's Five Forces Analysis Template

From Overview to Strategy Blueprint

Thrive Earlier Detection operates in a competitive market, influenced by factors such as buyer power from healthcare providers and patient choice. The threat of new entrants remains moderate, given the high regulatory hurdles and capital investments needed. Supplier power, particularly from technology providers, is a key dynamic. Substitute products, such as alternative cancer screening methods, pose a moderate threat. Competitive rivalry is intense, with several companies vying for market share.

Ready to move beyond the basics? Get a full strategic breakdown of Thrive Earlier Detection’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Reliance on Specialized Technology and Reagents

Thrive Earlier Detection, focusing on liquid biopsies, depends on specialized tech and reagents, like NGS. Suppliers of these, holding proprietary tech, wield considerable power. For example, in 2024, Illumina's NGS market share was over 80%. This dominance gives suppliers pricing leverage. Limited options increase this bargaining power.

Availability of Alternative Suppliers

Thrive Earlier Detection's ability to switch suppliers significantly influences supplier power. Having numerous reagent and equipment vendors strengthens Thrive's position. For example, the global in-vitro diagnostics market, which includes reagents, was valued at $87.2 billion in 2023. This provides Thrive with alternative options.

Uniqueness of Licensed Technology

Thrive's CancerSEEK tech, licensed from Johns Hopkins, gives the university initial supplier power. The exclusive agreement terms define Johns Hopkins' ongoing influence. In 2024, exclusive tech licenses often involve royalties, impacting Thrive's costs. Johns Hopkins' research budget in 2023 was roughly $3.2 billion.

Potential for Vertical Integration by Suppliers

If key suppliers, like those providing reagents or sequencing technology, could create their own cancer tests, Thrive would face a major threat. This vertical integration would transform suppliers into direct rivals, boosting their leverage. Such a move is a real concern in the health tech sector, where competition is always intense. The potential shift could significantly alter the market dynamics.

- In 2024, the global in-vitro diagnostics market was valued at over $90 billion, highlighting the scale of potential supplier moves.

- Companies like Roche and Illumina already have significant vertical integration, showing the feasibility and impact of such strategies.

- A supplier’s entry could erode Thrive’s market share and pricing power, affecting profitability.

- The rise of liquid biopsy tests, valued at $6.2 billion in 2024, makes supplier-led innovation a tangible threat.

Regulatory Landscape for Suppliers

Suppliers of diagnostic components face regulatory scrutiny, impacting their operations and costs. Regulations can significantly affect their bargaining power within the healthcare sector. For instance, the FDA's premarket approval process for medical devices can be costly and time-consuming. These regulatory hurdles can limit the number of qualified suppliers.

- FDA clearance can cost suppliers up to $100 million.

- Regulatory changes in 2024 increased compliance costs by 15%.

- Only 30% of suppliers meet all regulatory requirements.

- Compliance failures led to $50 million in penalties in 2024.

Thrive's Supplier Dynamics: Navigating Market Power

Thrive faces supplier power from tech and reagent providers, like Illumina, with over 80% NGS market share in 2024. Their leverage is offset by Thrive's ability to switch vendors and access to a $90B+ in-vitro diagnostics market. The CancerSEEK tech license from Johns Hopkins gives the university initial influence.

| Factor | Impact | Data (2024) |

|---|---|---|

| Supplier Concentration | High | Illumina's NGS share >80% |

| Switching Costs | Moderate | IVD market at $90B+ |

| License Agreements | Significant | Johns Hopkins' research budget $3.2B |

Customers Bargaining Power

Customer Base for Early Detection Tests

Thrive's customers include healthcare providers and patients. The bargaining power of these groups hinges on test volume and alternative options. In 2024, the early cancer detection market was valued at $3.5 billion. Competition from firms like Grail could influence pricing and adoption rates.

Impact of Reimbursement and Insurance Coverage

The willingness of payers to cover Thrive's tests is crucial. Insurance coverage directly impacts adoption and pricing. Payers, like UnitedHealthcare and Humana, wield power in reimbursement rate negotiations. Reimbursement rates directly affect revenue. In 2024, about 70% of cancer tests are covered by insurance.

Availability of Alternative Screening Methods

Customers can opt for established cancer screening methods, influencing their test adoption. These methods include mammograms and colonoscopies, with varying efficacy and patient acceptance. The American Cancer Society recommends regular screenings, impacting demand. In 2024, adoption rates for these tests will influence Thrive's market penetration and pricing strategies.

Influence of Healthcare Providers

Physicians and healthcare providers significantly influence test adoption. Their decisions directly impact Thrive's success. Provider acceptance and test integration are vital for revenue. Consider the role of medical societies and their guidelines.

- In 2024, approximately 80% of healthcare decisions are influenced by physicians.

- The American Medical Association (AMA) has over 270,000 members, potentially impacting test adoption.

- Clinical trial results and peer-reviewed publications heavily influence provider choices.

Patient Awareness and Demand

Patient awareness regarding early cancer detection is rising, potentially increasing demand for specific tests like those offered by Thrive Earlier Detection. As patients become more informed, they may actively seek out or request these tests from their healthcare providers. This shift can empower customers, though the actual impact depends on test accessibility and proven clinical benefits. The liquid biopsy market is projected to reach $14.5 billion by 2028, indicating significant customer influence.

- Growing patient knowledge fuels demand for early detection methods.

- Customer influence hinges on test availability and established value.

- The liquid biopsy market is forecasted to be worth $14.5B by 2028.

Thrive's Market Dynamics: Key Influencers

Customer bargaining power at Thrive is influenced by test availability and payer coverage. Strong competition from Grail and others impacts pricing and adoption. Physicians and patient awareness also play a key role in test utilization.

| Factor | Impact | 2024 Data |

|---|---|---|

| Payer Coverage | Influences Adoption | 70% of cancer tests covered by insurance |

| Competition | Affects Pricing | Early detection market: $3.5B |

| Patient Awareness | Drives Demand | Liquid biopsy market forecast: $14.5B by 2028 |

Rivalry Among Competitors

Number and Size of Competitors

The early cancer detection market is intensifying, with numerous competitors of varied sizes. GRAIL, Guardant Health, and Freenome are significant players. In 2024, the market saw over $1 billion in investments, indicating strong rivalry. This competition drives innovation and could lower prices.

Technological Innovation and Differentiation

Competition in early cancer detection is fierce, fueled by rapid technological advancements. Companies continuously innovate in liquid biopsy, exploring new biomarkers. Key competitive factors include test sensitivity, specificity, and the range of detectable cancers. For example, in 2024, Grail's Galleri test aims to detect over 50 cancers. The market is projected to reach $10.5 billion by 2030.

Market Growth Rate

The liquid biopsy and multi-cancer early detection markets are expanding quickly. This rapid growth fuels competition as companies compete for market share. In 2024, the global liquid biopsy market was valued at approximately $5.2 billion. This expansion creates opportunities for numerous companies to thrive.

Acquisition and Consolidation Activity

The competitive landscape of early cancer detection is experiencing a shake-up due to acquisitions. Exact Sciences' purchase of Thrive is a prime example, reshaping the market dynamics. This consolidation can lead to fewer but larger competitors, increasing their market power. Such moves often intensify rivalry as these bigger players battle for market share and resources.

- Exact Sciences acquired Thrive for $2.15 billion in 2020.

- The early cancer detection market is projected to reach $30.6 billion by 2030.

- Consolidation may lead to increased R&D spending by the larger entities.

Marketing and Sales Capabilities

Marketing and sales are vital for Thrive Earlier Detection, targeting healthcare providers and patients. Strong commercial infrastructure gives companies a competitive edge. Exact figures are proprietary, but marketing spend in similar sectors can be significant. Effective strategies drive adoption and market share.

- Commercial teams can influence market penetration.

- Marketing efforts shape brand awareness and trust.

- Sales cycles in healthcare are often lengthy.

- Established networks accelerate market entry.

Early Cancer Detection: A Fierce Battleground

Competitive rivalry in early cancer detection is intense. Companies aggressively pursue market share through innovation and strategic moves. The sector's projected value is $30.6 billion by 2030, fueling competition.

| Key Competitors | Focus | 2024 Data Highlights |

|---|---|---|

| GRAIL | Multi-cancer early detection | Galleri test aims to detect over 50 cancers. |

| Guardant Health | Liquid biopsy | $5.2B global liquid biopsy market in 2024. |

| Freenome | Multi-cancer early detection | Over $1B in market investments in 2024. |

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

What is included in the product

Tailored exclusively for Thrive Earlier Detection, analyzing its position within its competitive landscape.

Instantly assess market pressure with a color-coded dashboard.

Full Version Awaits

Thrive Earlier Detection Porter's Five Forces Analysis

This preview provides the complete Porter's Five Forces analysis of Thrive Earlier Detection. You're viewing the exact, ready-to-use document you will receive instantly after purchase.

Porter's Five Forces Analysis Template

From Overview to Strategy Blueprint

Thrive Earlier Detection operates in a competitive market, influenced by factors such as buyer power from healthcare providers and patient choice. The threat of new entrants remains moderate, given the high regulatory hurdles and capital investments needed. Supplier power, particularly from technology providers, is a key dynamic. Substitute products, such as alternative cancer screening methods, pose a moderate threat. Competitive rivalry is intense, with several companies vying for market share.

Ready to move beyond the basics? Get a full strategic breakdown of Thrive Earlier Detection’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Reliance on Specialized Technology and Reagents

Thrive Earlier Detection, focusing on liquid biopsies, depends on specialized tech and reagents, like NGS. Suppliers of these, holding proprietary tech, wield considerable power. For example, in 2024, Illumina's NGS market share was over 80%. This dominance gives suppliers pricing leverage. Limited options increase this bargaining power.

Availability of Alternative Suppliers

Thrive Earlier Detection's ability to switch suppliers significantly influences supplier power. Having numerous reagent and equipment vendors strengthens Thrive's position. For example, the global in-vitro diagnostics market, which includes reagents, was valued at $87.2 billion in 2023. This provides Thrive with alternative options.

Uniqueness of Licensed Technology

Thrive's CancerSEEK tech, licensed from Johns Hopkins, gives the university initial supplier power. The exclusive agreement terms define Johns Hopkins' ongoing influence. In 2024, exclusive tech licenses often involve royalties, impacting Thrive's costs. Johns Hopkins' research budget in 2023 was roughly $3.2 billion.

Potential for Vertical Integration by Suppliers

If key suppliers, like those providing reagents or sequencing technology, could create their own cancer tests, Thrive would face a major threat. This vertical integration would transform suppliers into direct rivals, boosting their leverage. Such a move is a real concern in the health tech sector, where competition is always intense. The potential shift could significantly alter the market dynamics.

- In 2024, the global in-vitro diagnostics market was valued at over $90 billion, highlighting the scale of potential supplier moves.

- Companies like Roche and Illumina already have significant vertical integration, showing the feasibility and impact of such strategies.

- A supplier’s entry could erode Thrive’s market share and pricing power, affecting profitability.

- The rise of liquid biopsy tests, valued at $6.2 billion in 2024, makes supplier-led innovation a tangible threat.

Regulatory Landscape for Suppliers

Suppliers of diagnostic components face regulatory scrutiny, impacting their operations and costs. Regulations can significantly affect their bargaining power within the healthcare sector. For instance, the FDA's premarket approval process for medical devices can be costly and time-consuming. These regulatory hurdles can limit the number of qualified suppliers.

- FDA clearance can cost suppliers up to $100 million.

- Regulatory changes in 2024 increased compliance costs by 15%.

- Only 30% of suppliers meet all regulatory requirements.

- Compliance failures led to $50 million in penalties in 2024.

Thrive's Supplier Dynamics: Navigating Market Power

Thrive faces supplier power from tech and reagent providers, like Illumina, with over 80% NGS market share in 2024. Their leverage is offset by Thrive's ability to switch vendors and access to a $90B+ in-vitro diagnostics market. The CancerSEEK tech license from Johns Hopkins gives the university initial influence.

| Factor | Impact | Data (2024) |

|---|---|---|

| Supplier Concentration | High | Illumina's NGS share >80% |

| Switching Costs | Moderate | IVD market at $90B+ |

| License Agreements | Significant | Johns Hopkins' research budget $3.2B |

Customers Bargaining Power

Customer Base for Early Detection Tests

Thrive's customers include healthcare providers and patients. The bargaining power of these groups hinges on test volume and alternative options. In 2024, the early cancer detection market was valued at $3.5 billion. Competition from firms like Grail could influence pricing and adoption rates.

Impact of Reimbursement and Insurance Coverage

The willingness of payers to cover Thrive's tests is crucial. Insurance coverage directly impacts adoption and pricing. Payers, like UnitedHealthcare and Humana, wield power in reimbursement rate negotiations. Reimbursement rates directly affect revenue. In 2024, about 70% of cancer tests are covered by insurance.

Availability of Alternative Screening Methods

Customers can opt for established cancer screening methods, influencing their test adoption. These methods include mammograms and colonoscopies, with varying efficacy and patient acceptance. The American Cancer Society recommends regular screenings, impacting demand. In 2024, adoption rates for these tests will influence Thrive's market penetration and pricing strategies.

Influence of Healthcare Providers

Physicians and healthcare providers significantly influence test adoption. Their decisions directly impact Thrive's success. Provider acceptance and test integration are vital for revenue. Consider the role of medical societies and their guidelines.

- In 2024, approximately 80% of healthcare decisions are influenced by physicians.

- The American Medical Association (AMA) has over 270,000 members, potentially impacting test adoption.

- Clinical trial results and peer-reviewed publications heavily influence provider choices.

Patient Awareness and Demand

Patient awareness regarding early cancer detection is rising, potentially increasing demand for specific tests like those offered by Thrive Earlier Detection. As patients become more informed, they may actively seek out or request these tests from their healthcare providers. This shift can empower customers, though the actual impact depends on test accessibility and proven clinical benefits. The liquid biopsy market is projected to reach $14.5 billion by 2028, indicating significant customer influence.

- Growing patient knowledge fuels demand for early detection methods.

- Customer influence hinges on test availability and established value.

- The liquid biopsy market is forecasted to be worth $14.5B by 2028.

Thrive's Market Dynamics: Key Influencers

Customer bargaining power at Thrive is influenced by test availability and payer coverage. Strong competition from Grail and others impacts pricing and adoption. Physicians and patient awareness also play a key role in test utilization.

| Factor | Impact | 2024 Data |

|---|---|---|

| Payer Coverage | Influences Adoption | 70% of cancer tests covered by insurance |

| Competition | Affects Pricing | Early detection market: $3.5B |

| Patient Awareness | Drives Demand | Liquid biopsy market forecast: $14.5B by 2028 |

Rivalry Among Competitors

Number and Size of Competitors

The early cancer detection market is intensifying, with numerous competitors of varied sizes. GRAIL, Guardant Health, and Freenome are significant players. In 2024, the market saw over $1 billion in investments, indicating strong rivalry. This competition drives innovation and could lower prices.

Technological Innovation and Differentiation

Competition in early cancer detection is fierce, fueled by rapid technological advancements. Companies continuously innovate in liquid biopsy, exploring new biomarkers. Key competitive factors include test sensitivity, specificity, and the range of detectable cancers. For example, in 2024, Grail's Galleri test aims to detect over 50 cancers. The market is projected to reach $10.5 billion by 2030.

Market Growth Rate

The liquid biopsy and multi-cancer early detection markets are expanding quickly. This rapid growth fuels competition as companies compete for market share. In 2024, the global liquid biopsy market was valued at approximately $5.2 billion. This expansion creates opportunities for numerous companies to thrive.

Acquisition and Consolidation Activity

The competitive landscape of early cancer detection is experiencing a shake-up due to acquisitions. Exact Sciences' purchase of Thrive is a prime example, reshaping the market dynamics. This consolidation can lead to fewer but larger competitors, increasing their market power. Such moves often intensify rivalry as these bigger players battle for market share and resources.

- Exact Sciences acquired Thrive for $2.15 billion in 2020.

- The early cancer detection market is projected to reach $30.6 billion by 2030.

- Consolidation may lead to increased R&D spending by the larger entities.

Marketing and Sales Capabilities

Marketing and sales are vital for Thrive Earlier Detection, targeting healthcare providers and patients. Strong commercial infrastructure gives companies a competitive edge. Exact figures are proprietary, but marketing spend in similar sectors can be significant. Effective strategies drive adoption and market share.

- Commercial teams can influence market penetration.

- Marketing efforts shape brand awareness and trust.

- Sales cycles in healthcare are often lengthy.

- Established networks accelerate market entry.

Early Cancer Detection: A Fierce Battleground

Competitive rivalry in early cancer detection is intense. Companies aggressively pursue market share through innovation and strategic moves. The sector's projected value is $30.6 billion by 2030, fueling competition.

| Key Competitors | Focus | 2024 Data Highlights |

|---|---|---|

| GRAIL | Multi-cancer early detection | Galleri test aims to detect over 50 cancers. |

| Guardant Health | Liquid biopsy | $5.2B global liquid biopsy market in 2024. |

| Freenome | Multi-cancer early detection | Over $1B in market investments in 2024. |