ZETA ENERGY PORTER'S FIVE FORCES TEMPLATE RESEARCH

What is included in the product

Evaluates control held by suppliers and buyers, and their influence on pricing and profitability.

Instantly see how industry factors impact Zeta's profitability with a dynamic, data-driven chart.

Preview Before You Purchase

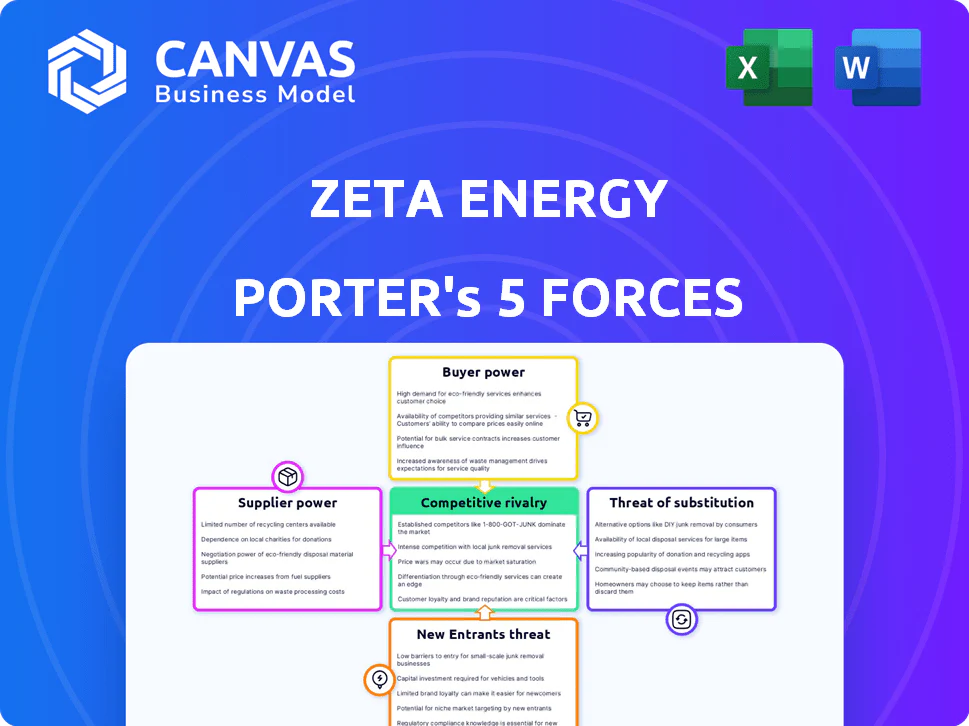

Zeta Energy Porter's Five Forces Analysis

This is the full Zeta Energy Porter's Five Forces analysis. You're previewing the complete document, ready for immediate download.

Porter's Five Forces Analysis Template

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Zeta Energy faces a dynamic landscape. Supplier power is moderately high due to specialized materials needed. Buyer power is limited, given the nascent market. The threat of new entrants is moderate, with substantial capital requirements. Substitute products pose a low threat currently. Competitive rivalry is intensifying as the market develops.

This preview is just the beginning. The full analysis provides a complete strategic snapshot with force-by-force ratings, visuals, and business implications tailored to Zeta Energy.

Suppliers Bargaining Power

Reliance on Key Materials

Zeta Energy's reliance on lithium, carbon, and sulfur, while abundant, introduces supplier power dynamics. The availability of high-purity lithium, crucial for their batteries, is influenced by a concentrated market. In 2024, lithium prices experienced volatility, impacting battery production costs. Specialized carbon materials, like vertically-aligned carbon nanotubes, further concentrate supplier power due to limited manufacturers.

Proprietary Technology Inputs

Zeta Energy's edge lies in its proprietary tech for anodes and cathodes, but it still relies on suppliers for components. This dependence could be heightened by the specialized materials needed for their lithium-sulfur batteries. For example, in 2024, the global lithium-ion battery market was valued at over $70 billion, with key material suppliers holding significant market share.

Manufacturing Equipment Suppliers

The manufacturing of Zeta Energy's advanced batteries depends on specialized equipment, potentially giving suppliers strong bargaining power. If the equipment is unique or requires specific servicing, Zeta might face higher costs. However, Zeta's plan to use existing gigafactory tech could reduce this power. For example, in 2024, the battery manufacturing equipment market was valued at approximately $8.5 billion.

Supply Chain Concentration Risk

Supply chain concentration can significantly impact Zeta Energy. Even with abundant raw materials, processing and distribution can be controlled by a few. This concentration could elevate costs and limit material access for Zeta Energy. Focusing on domestic supply chains, like in North America, can help, but regional risks may persist.

- In 2024, the global solar panel supply chain saw significant consolidation, with the top five manufacturers controlling over 80% of the market.

- The Inflation Reduction Act in the US aims to boost domestic solar manufacturing, but regional concentration remains a factor.

- Dependence on a few key suppliers could make Zeta Energy vulnerable to price hikes or disruptions.

- Diversifying suppliers or investing in vertical integration could mitigate this risk.

Potential for Supplier Forward Integration

The potential for suppliers to move forward into battery cell manufacturing presents a risk. Key battery component suppliers could become direct competitors. This is particularly relevant for providers of complex technologies. Some suppliers of materials are also developing battery technologies.

- Companies like Umicore and BASF are involved in both material supply and battery technology development.

- In 2024, the battery materials market was valued at over $30 billion.

- Forward integration could disrupt existing supply chains.

- This poses a threat to Zeta Energy's market position.

Zeta Energy: Navigating Supplier Risks in the Battery Market

Zeta Energy faces supplier power challenges due to reliance on specialized materials and equipment. In 2024, the battery materials market was valued at over $30 billion, with key suppliers holding significant influence. The potential for forward integration by suppliers, as seen with companies like Umicore and BASF, adds further risk. Diversifying suppliers and considering vertical integration could mitigate these risks.

| Supplier Power Element | Impact on Zeta Energy | 2024 Data |

|---|---|---|

| Material Concentration | Higher costs, supply disruptions | Lithium-ion battery market: $70B+ |

| Equipment Dependence | Increased manufacturing costs | Battery equipment market: $8.5B |

| Supplier Forward Integration | Increased competition | Battery materials market: $30B+ |

Customers Bargaining Power

Diverse Customer Base

Zeta Energy's diverse applications across electric vehicles, grid storage, and consumer electronics create a broad customer base. This diversity helps to mitigate the influence of any single customer group. However, the electric vehicle market, projected to reach $823.75 billion by 2030, presents a significant customer segment where large automakers could exert considerable bargaining power. In 2024, EV sales continue to rise, impacting the dynamics.

Customer Price Sensitivity

Zeta Energy's battery cost-effectiveness is a key factor. Their batteries are expected to be less than half the price per kWh compared to lithium-ion. This makes price a crucial negotiation point for customers. Customers have stronger bargaining power, especially in competitive markets like the EV sector, where price wars are common. In 2024, the average cost of lithium-ion batteries was around $139 per kWh, Zeta aims to significantly undercut that.

Availability of Alternative Battery Technologies

Customers can choose from diverse battery technologies like lithium-ion and solid-state. This access to alternatives boosts their bargaining power. The global lithium-ion battery market was valued at $66.4 billion in 2023. Solid-state batteries are expected to grow significantly. This competition gives customers leverage.

Customer Switching Costs

Customer switching costs significantly impact the bargaining power of customers in the battery market. High switching costs, such as those related to specialized equipment or extensive product redesigns, weaken customer power. If switching is easy, customer power rises.

Zeta Energy aims for its technology to integrate seamlessly into existing gigafactories. This approach may lower switching costs for manufacturers. This could increase customer power.

- The average cost to build a new gigafactory is $2 billion in 2024.

- The global battery market is projected to reach $150 billion by the end of 2024.

- China controls about 76% of the global lithium-ion battery manufacturing capacity in 2024.

In 2024, the ease of integration for Zeta's battery technology could be a key factor in its market positioning.

This could potentially influence Zeta's pricing strategies and competitive dynamics.

Large Volume Orders

Zeta Energy faces strong customer bargaining power, especially from those ordering in bulk, such as electric vehicle and grid storage manufacturers. These large customers can significantly influence pricing and terms, given the volume of their orders and its impact on Zeta's revenue. The Stellantis agreement exemplifies a key high-volume relationship, where Zeta's success hinges on satisfying a major client. This concentration of demand amplifies customer leverage, potentially squeezing profit margins.

- Stellantis deal is critical for Zeta's revenue.

- Large orders impact pricing negotiations.

- Customer concentration increases risk.

- Profit margins can be pressured.

Zeta's Pricing Battle: EV Giants Hold the Cards

Zeta Energy faces significant customer bargaining power, particularly from large EV and grid storage manufacturers, impacting pricing and profit margins. The EV market, valued at $823.75 billion by 2030, allows major players like Stellantis to influence terms. Zeta's cost-effective batteries, aiming below $139/kWh (2024 lithium-ion average), are key to negotiations.

| Aspect | Impact | Data (2024) |

|---|---|---|

| Customer Concentration | High leverage | Stellantis deal is critical for revenue |

| Price Sensitivity | Strong bargaining | Li-ion avg. $139/kWh, Zeta aims lower |

| Market Competition | Increased power | Global battery market ~$150B |

Rivalry Among Competitors

Presence of Established Lithium-Ion Manufacturers

The battery market, especially for EVs and grid storage, is fiercely competitive, dominated by established lithium-ion battery manufacturers. These giants, such as CATL and LG Energy Solution, possess substantial production capabilities and well-oiled supply chains. Strong brand recognition further intensifies rivalry, creating a challenging environment for Zeta Energy. In 2024, CATL held around 37% of the global EV battery market share, highlighting the dominance of existing players.

Emergence of Other Advanced Battery Technologies

The competitive landscape includes emerging battery technologies. Solid-state and sodium-ion batteries are becoming commercially viable. These advancements challenge Zeta Energy's lithium-sulfur batteries. Companies like Solid Power and Natron Energy are key players. The global battery market is projected to reach $196.7 billion by 2028, with a CAGR of 12.7% from 2023 to 2028.

Focus on Performance and Cost

Competition in the battery market centers on performance and cost. Zeta Energy emphasizes its advantages in energy density and charging speed. Competitors constantly advance their tech, creating a dynamic market. For example, in 2024, battery costs fell, increasing competition. Companies compete for tech leadership and cost efficiency.

Global Nature of the Battery Market

The battery market's global nature significantly impacts Zeta Energy. Competition is fierce, with key players and manufacturing hubs primarily in the Asia-Pacific region. Zeta Energy contends with both domestic and international rivals, some backed by substantial government support. This global landscape intensifies the pressure to innovate and compete effectively. The battery market was valued at $145.1 billion in 2023.

- Asia-Pacific controls over 70% of global battery manufacturing.

- China's battery manufacturers hold a dominant market share.

- Government subsidies significantly influence competitive dynamics.

Industry Consolidation and Partnerships

The battery industry is experiencing increased industry consolidation and partnerships. These strategic moves, including joint ventures, are aimed at expanding market share and securing crucial supply chains. This trend is evident in the electric vehicle (EV) battery sector, where competition is fierce. Such collaborations create larger, more competitive entities, reshaping the market landscape.

- In 2024, several major battery manufacturers announced partnerships to enhance production capacity and technology sharing.

- The global lithium-ion battery market is expected to reach $94.4 billion by the end of 2024.

- Mergers and acquisitions in the battery technology space have increased by 15% in the last year.

- These partnerships often involve significant financial investments, with some deals valued in the billions of dollars.

Battery Market: Fierce Competition Ahead

The battery market features intense rivalry, with established giants like CATL and LG Energy Solution dominating production and supply chains; CATL had about 37% of the global EV battery market share in 2024. Emerging technologies and cost competition further intensify the dynamics. The global lithium-ion battery market is projected to reach $94.4 billion by the end of 2024.

| Aspect | Details | Impact on Zeta Energy |

|---|---|---|

| Market Share | CATL (37% in 2024), LG Energy Solution | High competition from established players |

| Technology | Solid-state, sodium-ion batteries | Challenges Zeta's lithium-sulfur tech |

| Market Growth | Global battery market projected to $196.7B by 2028 | Opportunities with intense competition |

| Cost | Battery costs decreasing | Increased pressure to reduce costs |

Original: $10.00

-65%$10.00

$3.50ZETA ENERGY PORTER'S FIVE FORCES TEMPLATE RESEARCH

What is included in the product

Evaluates control held by suppliers and buyers, and their influence on pricing and profitability.

Instantly see how industry factors impact Zeta's profitability with a dynamic, data-driven chart.

Preview Before You Purchase

Zeta Energy Porter's Five Forces Analysis

This is the full Zeta Energy Porter's Five Forces analysis. You're previewing the complete document, ready for immediate download.

Porter's Five Forces Analysis Template

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Zeta Energy faces a dynamic landscape. Supplier power is moderately high due to specialized materials needed. Buyer power is limited, given the nascent market. The threat of new entrants is moderate, with substantial capital requirements. Substitute products pose a low threat currently. Competitive rivalry is intensifying as the market develops.

This preview is just the beginning. The full analysis provides a complete strategic snapshot with force-by-force ratings, visuals, and business implications tailored to Zeta Energy.

Suppliers Bargaining Power

Reliance on Key Materials

Zeta Energy's reliance on lithium, carbon, and sulfur, while abundant, introduces supplier power dynamics. The availability of high-purity lithium, crucial for their batteries, is influenced by a concentrated market. In 2024, lithium prices experienced volatility, impacting battery production costs. Specialized carbon materials, like vertically-aligned carbon nanotubes, further concentrate supplier power due to limited manufacturers.

Proprietary Technology Inputs

Zeta Energy's edge lies in its proprietary tech for anodes and cathodes, but it still relies on suppliers for components. This dependence could be heightened by the specialized materials needed for their lithium-sulfur batteries. For example, in 2024, the global lithium-ion battery market was valued at over $70 billion, with key material suppliers holding significant market share.

Manufacturing Equipment Suppliers

The manufacturing of Zeta Energy's advanced batteries depends on specialized equipment, potentially giving suppliers strong bargaining power. If the equipment is unique or requires specific servicing, Zeta might face higher costs. However, Zeta's plan to use existing gigafactory tech could reduce this power. For example, in 2024, the battery manufacturing equipment market was valued at approximately $8.5 billion.

Supply Chain Concentration Risk

Supply chain concentration can significantly impact Zeta Energy. Even with abundant raw materials, processing and distribution can be controlled by a few. This concentration could elevate costs and limit material access for Zeta Energy. Focusing on domestic supply chains, like in North America, can help, but regional risks may persist.

- In 2024, the global solar panel supply chain saw significant consolidation, with the top five manufacturers controlling over 80% of the market.

- The Inflation Reduction Act in the US aims to boost domestic solar manufacturing, but regional concentration remains a factor.

- Dependence on a few key suppliers could make Zeta Energy vulnerable to price hikes or disruptions.

- Diversifying suppliers or investing in vertical integration could mitigate this risk.

Potential for Supplier Forward Integration

The potential for suppliers to move forward into battery cell manufacturing presents a risk. Key battery component suppliers could become direct competitors. This is particularly relevant for providers of complex technologies. Some suppliers of materials are also developing battery technologies.

- Companies like Umicore and BASF are involved in both material supply and battery technology development.

- In 2024, the battery materials market was valued at over $30 billion.

- Forward integration could disrupt existing supply chains.

- This poses a threat to Zeta Energy's market position.

Zeta Energy: Navigating Supplier Risks in the Battery Market

Zeta Energy faces supplier power challenges due to reliance on specialized materials and equipment. In 2024, the battery materials market was valued at over $30 billion, with key suppliers holding significant influence. The potential for forward integration by suppliers, as seen with companies like Umicore and BASF, adds further risk. Diversifying suppliers and considering vertical integration could mitigate these risks.

| Supplier Power Element | Impact on Zeta Energy | 2024 Data |

|---|---|---|

| Material Concentration | Higher costs, supply disruptions | Lithium-ion battery market: $70B+ |

| Equipment Dependence | Increased manufacturing costs | Battery equipment market: $8.5B |

| Supplier Forward Integration | Increased competition | Battery materials market: $30B+ |

Customers Bargaining Power

Diverse Customer Base

Zeta Energy's diverse applications across electric vehicles, grid storage, and consumer electronics create a broad customer base. This diversity helps to mitigate the influence of any single customer group. However, the electric vehicle market, projected to reach $823.75 billion by 2030, presents a significant customer segment where large automakers could exert considerable bargaining power. In 2024, EV sales continue to rise, impacting the dynamics.

Customer Price Sensitivity

Zeta Energy's battery cost-effectiveness is a key factor. Their batteries are expected to be less than half the price per kWh compared to lithium-ion. This makes price a crucial negotiation point for customers. Customers have stronger bargaining power, especially in competitive markets like the EV sector, where price wars are common. In 2024, the average cost of lithium-ion batteries was around $139 per kWh, Zeta aims to significantly undercut that.

Availability of Alternative Battery Technologies

Customers can choose from diverse battery technologies like lithium-ion and solid-state. This access to alternatives boosts their bargaining power. The global lithium-ion battery market was valued at $66.4 billion in 2023. Solid-state batteries are expected to grow significantly. This competition gives customers leverage.

Customer Switching Costs

Customer switching costs significantly impact the bargaining power of customers in the battery market. High switching costs, such as those related to specialized equipment or extensive product redesigns, weaken customer power. If switching is easy, customer power rises.

Zeta Energy aims for its technology to integrate seamlessly into existing gigafactories. This approach may lower switching costs for manufacturers. This could increase customer power.

- The average cost to build a new gigafactory is $2 billion in 2024.

- The global battery market is projected to reach $150 billion by the end of 2024.

- China controls about 76% of the global lithium-ion battery manufacturing capacity in 2024.

In 2024, the ease of integration for Zeta's battery technology could be a key factor in its market positioning.

This could potentially influence Zeta's pricing strategies and competitive dynamics.

Large Volume Orders

Zeta Energy faces strong customer bargaining power, especially from those ordering in bulk, such as electric vehicle and grid storage manufacturers. These large customers can significantly influence pricing and terms, given the volume of their orders and its impact on Zeta's revenue. The Stellantis agreement exemplifies a key high-volume relationship, where Zeta's success hinges on satisfying a major client. This concentration of demand amplifies customer leverage, potentially squeezing profit margins.

- Stellantis deal is critical for Zeta's revenue.

- Large orders impact pricing negotiations.

- Customer concentration increases risk.

- Profit margins can be pressured.

Zeta's Pricing Battle: EV Giants Hold the Cards

Zeta Energy faces significant customer bargaining power, particularly from large EV and grid storage manufacturers, impacting pricing and profit margins. The EV market, valued at $823.75 billion by 2030, allows major players like Stellantis to influence terms. Zeta's cost-effective batteries, aiming below $139/kWh (2024 lithium-ion average), are key to negotiations.

| Aspect | Impact | Data (2024) |

|---|---|---|

| Customer Concentration | High leverage | Stellantis deal is critical for revenue |

| Price Sensitivity | Strong bargaining | Li-ion avg. $139/kWh, Zeta aims lower |

| Market Competition | Increased power | Global battery market ~$150B |

Rivalry Among Competitors

Presence of Established Lithium-Ion Manufacturers

The battery market, especially for EVs and grid storage, is fiercely competitive, dominated by established lithium-ion battery manufacturers. These giants, such as CATL and LG Energy Solution, possess substantial production capabilities and well-oiled supply chains. Strong brand recognition further intensifies rivalry, creating a challenging environment for Zeta Energy. In 2024, CATL held around 37% of the global EV battery market share, highlighting the dominance of existing players.

Emergence of Other Advanced Battery Technologies

The competitive landscape includes emerging battery technologies. Solid-state and sodium-ion batteries are becoming commercially viable. These advancements challenge Zeta Energy's lithium-sulfur batteries. Companies like Solid Power and Natron Energy are key players. The global battery market is projected to reach $196.7 billion by 2028, with a CAGR of 12.7% from 2023 to 2028.

Focus on Performance and Cost

Competition in the battery market centers on performance and cost. Zeta Energy emphasizes its advantages in energy density and charging speed. Competitors constantly advance their tech, creating a dynamic market. For example, in 2024, battery costs fell, increasing competition. Companies compete for tech leadership and cost efficiency.

Global Nature of the Battery Market

The battery market's global nature significantly impacts Zeta Energy. Competition is fierce, with key players and manufacturing hubs primarily in the Asia-Pacific region. Zeta Energy contends with both domestic and international rivals, some backed by substantial government support. This global landscape intensifies the pressure to innovate and compete effectively. The battery market was valued at $145.1 billion in 2023.

- Asia-Pacific controls over 70% of global battery manufacturing.

- China's battery manufacturers hold a dominant market share.

- Government subsidies significantly influence competitive dynamics.

Industry Consolidation and Partnerships

The battery industry is experiencing increased industry consolidation and partnerships. These strategic moves, including joint ventures, are aimed at expanding market share and securing crucial supply chains. This trend is evident in the electric vehicle (EV) battery sector, where competition is fierce. Such collaborations create larger, more competitive entities, reshaping the market landscape.

- In 2024, several major battery manufacturers announced partnerships to enhance production capacity and technology sharing.

- The global lithium-ion battery market is expected to reach $94.4 billion by the end of 2024.

- Mergers and acquisitions in the battery technology space have increased by 15% in the last year.

- These partnerships often involve significant financial investments, with some deals valued in the billions of dollars.

Battery Market: Fierce Competition Ahead

The battery market features intense rivalry, with established giants like CATL and LG Energy Solution dominating production and supply chains; CATL had about 37% of the global EV battery market share in 2024. Emerging technologies and cost competition further intensify the dynamics. The global lithium-ion battery market is projected to reach $94.4 billion by the end of 2024.

| Aspect | Details | Impact on Zeta Energy |

|---|---|---|

| Market Share | CATL (37% in 2024), LG Energy Solution | High competition from established players |

| Technology | Solid-state, sodium-ion batteries | Challenges Zeta's lithium-sulfur tech |

| Market Growth | Global battery market projected to $196.7B by 2028 | Opportunities with intense competition |

| Cost | Battery costs decreasing | Increased pressure to reduce costs |

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

What is included in the product

Evaluates control held by suppliers and buyers, and their influence on pricing and profitability.

Instantly see how industry factors impact Zeta's profitability with a dynamic, data-driven chart.

Preview Before You Purchase

Zeta Energy Porter's Five Forces Analysis

This is the full Zeta Energy Porter's Five Forces analysis. You're previewing the complete document, ready for immediate download.

Porter's Five Forces Analysis Template

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Zeta Energy faces a dynamic landscape. Supplier power is moderately high due to specialized materials needed. Buyer power is limited, given the nascent market. The threat of new entrants is moderate, with substantial capital requirements. Substitute products pose a low threat currently. Competitive rivalry is intensifying as the market develops.

This preview is just the beginning. The full analysis provides a complete strategic snapshot with force-by-force ratings, visuals, and business implications tailored to Zeta Energy.

Suppliers Bargaining Power

Reliance on Key Materials

Zeta Energy's reliance on lithium, carbon, and sulfur, while abundant, introduces supplier power dynamics. The availability of high-purity lithium, crucial for their batteries, is influenced by a concentrated market. In 2024, lithium prices experienced volatility, impacting battery production costs. Specialized carbon materials, like vertically-aligned carbon nanotubes, further concentrate supplier power due to limited manufacturers.

Proprietary Technology Inputs

Zeta Energy's edge lies in its proprietary tech for anodes and cathodes, but it still relies on suppliers for components. This dependence could be heightened by the specialized materials needed for their lithium-sulfur batteries. For example, in 2024, the global lithium-ion battery market was valued at over $70 billion, with key material suppliers holding significant market share.

Manufacturing Equipment Suppliers

The manufacturing of Zeta Energy's advanced batteries depends on specialized equipment, potentially giving suppliers strong bargaining power. If the equipment is unique or requires specific servicing, Zeta might face higher costs. However, Zeta's plan to use existing gigafactory tech could reduce this power. For example, in 2024, the battery manufacturing equipment market was valued at approximately $8.5 billion.

Supply Chain Concentration Risk

Supply chain concentration can significantly impact Zeta Energy. Even with abundant raw materials, processing and distribution can be controlled by a few. This concentration could elevate costs and limit material access for Zeta Energy. Focusing on domestic supply chains, like in North America, can help, but regional risks may persist.

- In 2024, the global solar panel supply chain saw significant consolidation, with the top five manufacturers controlling over 80% of the market.

- The Inflation Reduction Act in the US aims to boost domestic solar manufacturing, but regional concentration remains a factor.

- Dependence on a few key suppliers could make Zeta Energy vulnerable to price hikes or disruptions.

- Diversifying suppliers or investing in vertical integration could mitigate this risk.

Potential for Supplier Forward Integration

The potential for suppliers to move forward into battery cell manufacturing presents a risk. Key battery component suppliers could become direct competitors. This is particularly relevant for providers of complex technologies. Some suppliers of materials are also developing battery technologies.

- Companies like Umicore and BASF are involved in both material supply and battery technology development.

- In 2024, the battery materials market was valued at over $30 billion.

- Forward integration could disrupt existing supply chains.

- This poses a threat to Zeta Energy's market position.

Zeta Energy: Navigating Supplier Risks in the Battery Market

Zeta Energy faces supplier power challenges due to reliance on specialized materials and equipment. In 2024, the battery materials market was valued at over $30 billion, with key suppliers holding significant influence. The potential for forward integration by suppliers, as seen with companies like Umicore and BASF, adds further risk. Diversifying suppliers and considering vertical integration could mitigate these risks.

| Supplier Power Element | Impact on Zeta Energy | 2024 Data |

|---|---|---|

| Material Concentration | Higher costs, supply disruptions | Lithium-ion battery market: $70B+ |

| Equipment Dependence | Increased manufacturing costs | Battery equipment market: $8.5B |

| Supplier Forward Integration | Increased competition | Battery materials market: $30B+ |

Customers Bargaining Power

Diverse Customer Base

Zeta Energy's diverse applications across electric vehicles, grid storage, and consumer electronics create a broad customer base. This diversity helps to mitigate the influence of any single customer group. However, the electric vehicle market, projected to reach $823.75 billion by 2030, presents a significant customer segment where large automakers could exert considerable bargaining power. In 2024, EV sales continue to rise, impacting the dynamics.

Customer Price Sensitivity

Zeta Energy's battery cost-effectiveness is a key factor. Their batteries are expected to be less than half the price per kWh compared to lithium-ion. This makes price a crucial negotiation point for customers. Customers have stronger bargaining power, especially in competitive markets like the EV sector, where price wars are common. In 2024, the average cost of lithium-ion batteries was around $139 per kWh, Zeta aims to significantly undercut that.

Availability of Alternative Battery Technologies

Customers can choose from diverse battery technologies like lithium-ion and solid-state. This access to alternatives boosts their bargaining power. The global lithium-ion battery market was valued at $66.4 billion in 2023. Solid-state batteries are expected to grow significantly. This competition gives customers leverage.

Customer Switching Costs

Customer switching costs significantly impact the bargaining power of customers in the battery market. High switching costs, such as those related to specialized equipment or extensive product redesigns, weaken customer power. If switching is easy, customer power rises.

Zeta Energy aims for its technology to integrate seamlessly into existing gigafactories. This approach may lower switching costs for manufacturers. This could increase customer power.

- The average cost to build a new gigafactory is $2 billion in 2024.

- The global battery market is projected to reach $150 billion by the end of 2024.

- China controls about 76% of the global lithium-ion battery manufacturing capacity in 2024.

In 2024, the ease of integration for Zeta's battery technology could be a key factor in its market positioning.

This could potentially influence Zeta's pricing strategies and competitive dynamics.

Large Volume Orders

Zeta Energy faces strong customer bargaining power, especially from those ordering in bulk, such as electric vehicle and grid storage manufacturers. These large customers can significantly influence pricing and terms, given the volume of their orders and its impact on Zeta's revenue. The Stellantis agreement exemplifies a key high-volume relationship, where Zeta's success hinges on satisfying a major client. This concentration of demand amplifies customer leverage, potentially squeezing profit margins.

- Stellantis deal is critical for Zeta's revenue.

- Large orders impact pricing negotiations.

- Customer concentration increases risk.

- Profit margins can be pressured.

Zeta's Pricing Battle: EV Giants Hold the Cards

Zeta Energy faces significant customer bargaining power, particularly from large EV and grid storage manufacturers, impacting pricing and profit margins. The EV market, valued at $823.75 billion by 2030, allows major players like Stellantis to influence terms. Zeta's cost-effective batteries, aiming below $139/kWh (2024 lithium-ion average), are key to negotiations.

| Aspect | Impact | Data (2024) |

|---|---|---|

| Customer Concentration | High leverage | Stellantis deal is critical for revenue |

| Price Sensitivity | Strong bargaining | Li-ion avg. $139/kWh, Zeta aims lower |

| Market Competition | Increased power | Global battery market ~$150B |

Rivalry Among Competitors

Presence of Established Lithium-Ion Manufacturers

The battery market, especially for EVs and grid storage, is fiercely competitive, dominated by established lithium-ion battery manufacturers. These giants, such as CATL and LG Energy Solution, possess substantial production capabilities and well-oiled supply chains. Strong brand recognition further intensifies rivalry, creating a challenging environment for Zeta Energy. In 2024, CATL held around 37% of the global EV battery market share, highlighting the dominance of existing players.

Emergence of Other Advanced Battery Technologies

The competitive landscape includes emerging battery technologies. Solid-state and sodium-ion batteries are becoming commercially viable. These advancements challenge Zeta Energy's lithium-sulfur batteries. Companies like Solid Power and Natron Energy are key players. The global battery market is projected to reach $196.7 billion by 2028, with a CAGR of 12.7% from 2023 to 2028.

Focus on Performance and Cost

Competition in the battery market centers on performance and cost. Zeta Energy emphasizes its advantages in energy density and charging speed. Competitors constantly advance their tech, creating a dynamic market. For example, in 2024, battery costs fell, increasing competition. Companies compete for tech leadership and cost efficiency.

Global Nature of the Battery Market

The battery market's global nature significantly impacts Zeta Energy. Competition is fierce, with key players and manufacturing hubs primarily in the Asia-Pacific region. Zeta Energy contends with both domestic and international rivals, some backed by substantial government support. This global landscape intensifies the pressure to innovate and compete effectively. The battery market was valued at $145.1 billion in 2023.

- Asia-Pacific controls over 70% of global battery manufacturing.

- China's battery manufacturers hold a dominant market share.

- Government subsidies significantly influence competitive dynamics.

Industry Consolidation and Partnerships

The battery industry is experiencing increased industry consolidation and partnerships. These strategic moves, including joint ventures, are aimed at expanding market share and securing crucial supply chains. This trend is evident in the electric vehicle (EV) battery sector, where competition is fierce. Such collaborations create larger, more competitive entities, reshaping the market landscape.

- In 2024, several major battery manufacturers announced partnerships to enhance production capacity and technology sharing.

- The global lithium-ion battery market is expected to reach $94.4 billion by the end of 2024.

- Mergers and acquisitions in the battery technology space have increased by 15% in the last year.

- These partnerships often involve significant financial investments, with some deals valued in the billions of dollars.

Battery Market: Fierce Competition Ahead

The battery market features intense rivalry, with established giants like CATL and LG Energy Solution dominating production and supply chains; CATL had about 37% of the global EV battery market share in 2024. Emerging technologies and cost competition further intensify the dynamics. The global lithium-ion battery market is projected to reach $94.4 billion by the end of 2024.

| Aspect | Details | Impact on Zeta Energy |

|---|---|---|

| Market Share | CATL (37% in 2024), LG Energy Solution | High competition from established players |

| Technology | Solid-state, sodium-ion batteries | Challenges Zeta's lithium-sulfur tech |

| Market Growth | Global battery market projected to $196.7B by 2028 | Opportunities with intense competition |

| Cost | Battery costs decreasing | Increased pressure to reduce costs |